GOOD MORNING,

Prices are mixed this morning, with soyoil lower on the back of a palm oil sell-off, while all other markets are higher. Conflicting stories continue to circulate for China and beans, but according to Shanghai's JCI, China will have to purchase US beans to cover any shortages they have with hog breeding expected to recover, and therefore meal demand higher. US beans remain cheaper than Brazil into what could be the end of the year.

Bean prices are firmer this morning into new highs, despite the WSJ story yesterday in which it stated that China had cancelled some US farm shipments including 23 cargoes of beans due to rising tensions between Washington and Beijing. The article stated that importers China Oil, Foodstuffs Corp., and China Grain Reserves Corp. had cancelled their shipments by passing on purchases of 23 cargoes of US beans last week. Conflicting stories are what trading ranges are made of, and beans have traversed the same range for months, but attempting to make an upside exit this AM.

Grains continue to mark time, though shorts are starting to get impatient with the inability of corn to break. Corn options trade has been more friendly lately, as shorts seem to want to hedge their 290K futures/options position by purchasing calls. Wheat prices could be headed for higher territory as charts still look to be potentially forming a market bottom. Dryness in the Great Plains will be watched closely to see if conditions begin to worsen.

WEATHER

Mostly ideal for the moment, with current Midwest weather still looking benign. The 6/10- and 8/14-day maps now show below average temperature odds, with periods of dryness for the extended outlook. Scattered showers move through the eastern cornbelt, with mostly dry weather Thurs. into Friday. Temperatures are well above normal west and near to above normal east. In the Delta, drier weather will help with planting activities. Scattered showers will appear for the rest of the week, which will benefit areas hit. Tropical Storm Cristobal will bring heavy rains to wherever it lands, which now looks to be around Louisiana.

REPORTS

Export sales:

Beans: 19/20 net 495,200 mt and 20/21 net 607,400 mt (vs. an expected 600 - 1.5 mt)

Meal: 19/20 net 558,900 mt and 20/21 net 25,000 mt (vs. an expected 200-650 mt)

Soyoil: 19/20 net 9,400 mt (vs. an expected 8-45 mt)

Corn: 19/20 net 637,500 mt and 20/21 net 27,500 mt (vs. an expected 450 -1.2 mmt)

Wheat: 19/20 net 179,500 mt and 20/21 net 437,300 mt (vs. an expected 150-850 mt)

Wheat: New sales were moderate to solid, with rising world premiums that will help push US into competitiveness.

Corn: Moderate old sales but poor new. Cheapest offers are out of SA, particularly Argentina. Quality remains an issue for old crop out of the west.

Meal: Big sales with Philippines the major buyers. Argentina's logistical issues help the US become more competitive.

Soyoil: Sales poor

Beans: Sales poor for old, above for new. China is the largest buyer.

Broiler Hatchery Data: Egg sets were close to unchanged YOY, while broilers placed were down 3%.

ANNOUNCEMENTS

World food prices fell for a 4th month in a row in May, according to the UN food agency, hitting a 17-month low. UN FAO world food price index averages 162.5 pts in May vs. 165.6 in April.

Brazil's ANEC forecasts June bean exports at 10.8 mln mt, down 22.3% from May's 13.9 mln mt. Bean exports for first half 2020 was 60.5 mln mt. Meal exports were forecast at 1.68 mln mt, down 1.2% from May at 1.70 mln mt.

Chinese media bureau reported live hog prices for late May were up 4.6% vs. the 10-day prev. period.

ProGro increased their 20/21 Ukraine wheat export forecast to 18.0 mln mt, up 1.0 mln mt vs. mo ago.

CALLS

Calls are as follows:

beans: 2 ½-3 higher

meal: .70-1.00 higher

soyoil: 25-30 lower

corn: 1 -1 1/2 higher

wheat: 6-8 higher

OUTSIDE MARKETS

Weaker energies with crude down to $36.38/barrel. The Dow is up 11 pts. with the US dollar continuing its fall to 97.11.

TECH TALK

- July soyoil trade hits a peak at 2820c but doesn't stay there long with a 50 pt break leading prices back down towards the 2750c level once again. The main direction for soyoil is higher, and pullbacks may find buying interest for another rally towards 2865c first, and gap-closure at 2890c.

- July meal could extend gains and advance towards major resistance at $288.00. Would look for a $281.00-$295.00 trading range.

- July beans continue to find a bid over the $8.50 level and trades towards $8.62 key resistance. The market remains well bid and could play this one from the long side with a sell-stop under $8.50.

- July corn walks the chart back to test $3.20, which now becomes key support for a market that could move higher. The July low of $3.21 was met but not broken, and prices are now well bid with a large short on record.

- July wheat tests its lower end trading range located at $5.05 with a nice bounce. Have to keep an eye on this chart, as any move over trendline resistance at $5.25 suggests that a possible inverted head and shoulders bottom has formed which targets $5.40-$5.50. The chart has been doing more work on the right shoulder, but any confirmation would have to come from a close over $5.25.

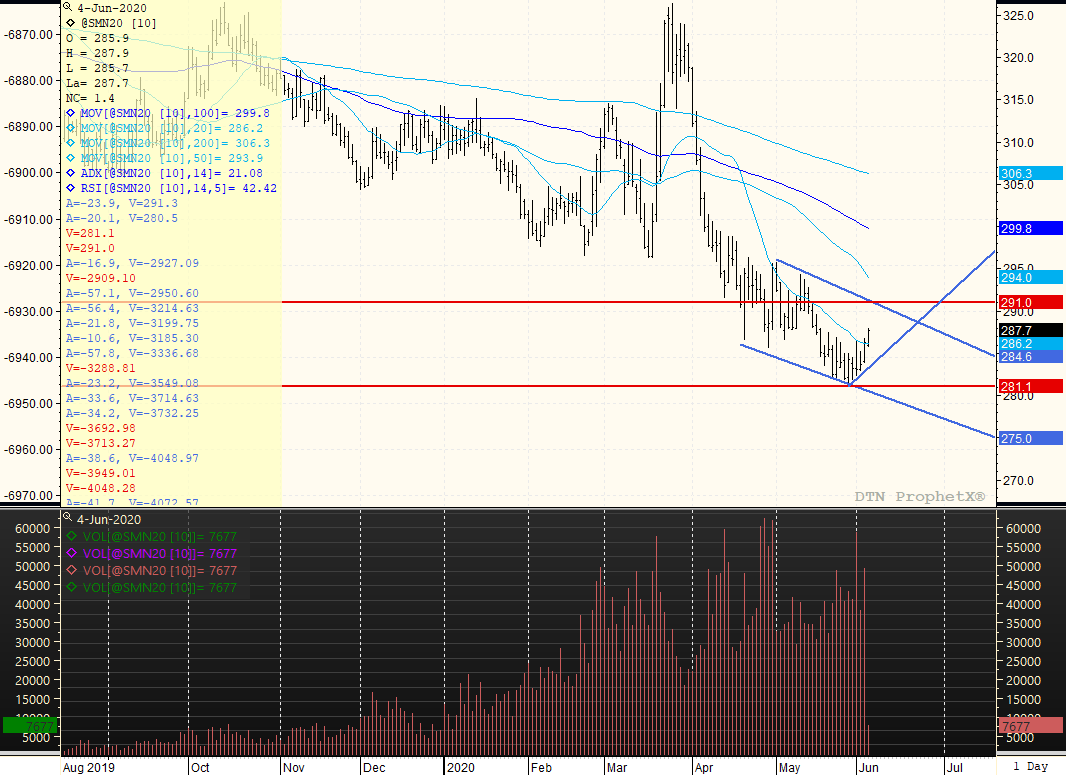

JULY MEAL

Overall trading range is from $281.50 to $295.00, with the swing point at $288.00. Because of the slight "v" shaped bottom, support is now more visually defined with trendline at $283.50. The market is gaining some upside momentum with the ADX strengthening to 21 from the teens, meaning pullbacks may be used to cover a short position. If needing to price, would continue to now do so on breaks, as frankly think prices will head towards $288.00 or better for a retracement upwards towards $295.00/$299.00.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Corn, soybeans and soyoil all closed lower after trading up the previous three sessions. July soymeal made it a fourth trading session higher, and wheat remains on a tear with a fifth trading session closing higher. The mood around wheat sees supply concerns developing in North America and in t...

Corn, soybeans and soyoil all closed lower after trading up the previous three sessions. July soymeal made it a fourth trading session higher, and wheat remains on a tear with a fifth trading session closing higher. The mood around wheat sees supply concerns developing in North America and in t...

Cow-calf producer margins are discussed less frequently in these pages than their downstream counterparts of feedlot and beef packer margins, but this doesn’t mean they are less important to understanding the beef industry’s current state and outlook. Additionally, discussion of thi...

Cow-calf producer margins are discussed less frequently in these pages than their downstream counterparts of feedlot and beef packer margins, but this doesn’t mean they are less important to understanding the beef industry’s current state and outlook. Additionally, discussion of thi...

Reigniting a Transatlantic Deal Former Italian prime minister Enrico Letta is something of a policy rock star after authoring a report on the future strategy for the EU. Most of the 146-page report focuses on strengthening the EU’s internal Single Market but, buried at the end of th...

Reigniting a Transatlantic Deal Former Italian prime minister Enrico Letta is something of a policy rock star after authoring a report on the future strategy for the EU. Most of the 146-page report focuses on strengthening the EU’s internal Single Market but, buried at the end of th...