NOTE: There will be no Technical Perspectives reports on 2 July.

GOOD MORNING,

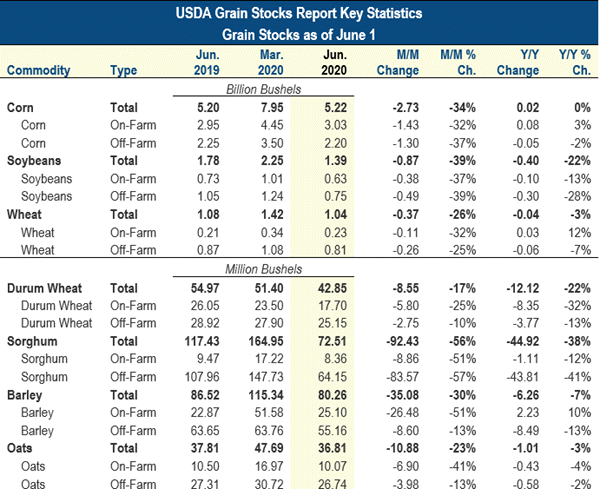

Funds entered the June Quarterly Stocks/Acreage report with a record short corn position, short elsewhere, and long beans. The report was bullish acreage and bearish to neutral stocks. However, the overriding factor is that the market has to digest the data delivered and it is focusing on acreage for the moment. Trading ranges are being adjusted slightly higher for corn, beans, and meal. Funds purchased 30K corn contracts yesterday, (20K the day before), which probably leaves them still short 270K. Cash markets were slightly lower as farmers took advantage of the price improvement to get something hedged.

Report Recap:

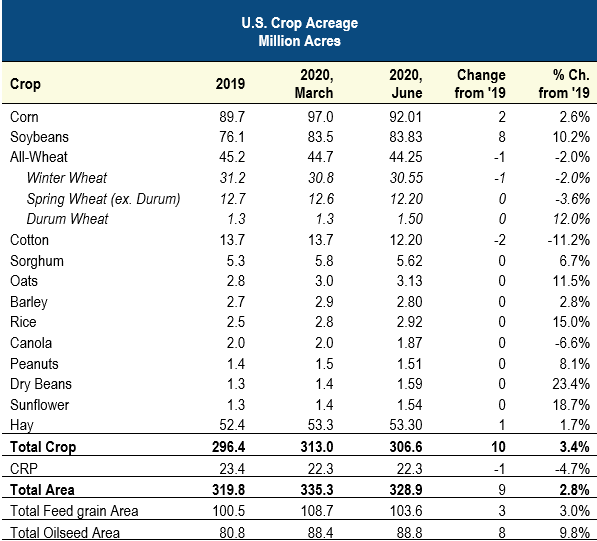

2020 planted acreage for the eight major crops was 246.7 mln acres, down 6.7 mln acres from March intentions and nearly equal to 2019's 247.0 mln.

WEATHER

July weather turns more interesting with hotter and drier weather to begin the day. Net drying in July will show depleted topsoil moisture but as long as subsoil moisture is reserved, crops will continue to be OK. This has been a wet week so far around the Midwest, with badly needed rains in North Dakota, Minn., and southern Ill. The 6/10-day outlook offers up little chance of rainfall though temperatures are average.

ANNOUNCEMENTS

Brazil's ANEC estimated June exports at 11.9 mmt, lower than 12.6 mmt. ANEC projects July exports at 7.25 mmt, stating that bean supplies have started to fall following record shipments.

Brazil's ANEC estimated June corn exports at 775,000 mt, lower than last week's projection of 1.0 mmt. They are projecting July corn exports at 3.9 mmt.

DELIVERIES

meal: 243, JP Morgan put out 241

soyoil: 287

Chicago wheat: 61

KC wheat: 16

CALLS

Calls are as follows:

beans: 5-8 higher

meal: 3.00-3.50 higher

soyoil: 4-9 higher

corn: 5-7 higher

wheat: 4-6 higher

OUTSIDE MARKETS

A firmer crude oil price, trading up to $40.58/barrel, and a firmer US dollar at 97.22. The Dow is off 280 pts.

TECH TALK

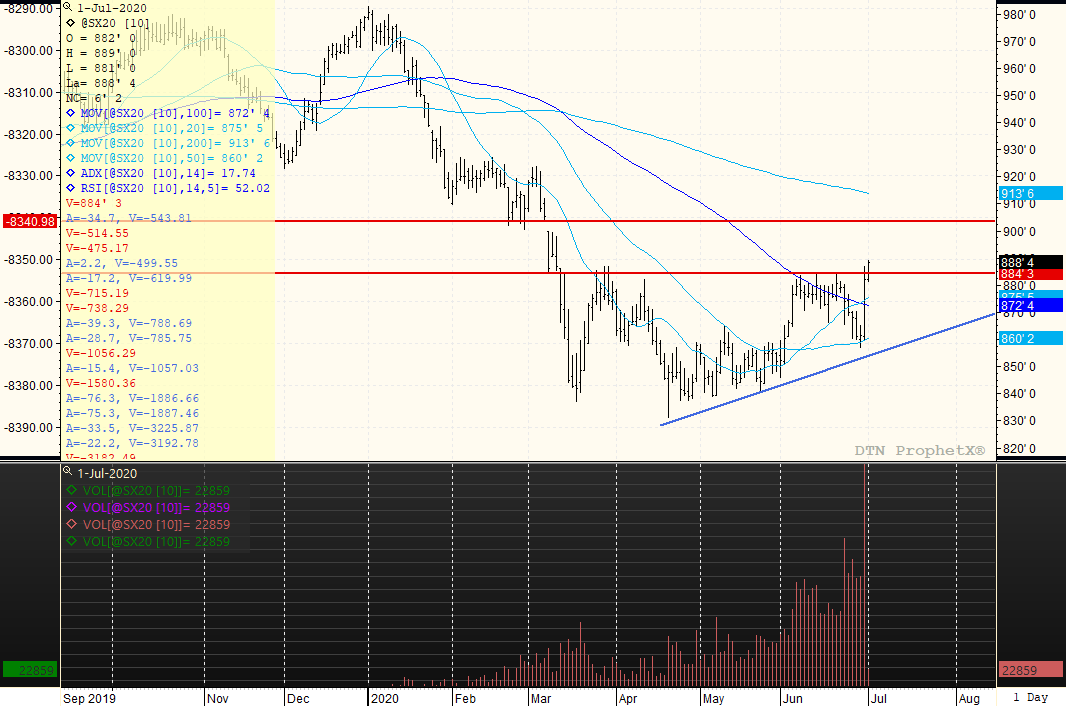

- November beans make a vertical straight up advance line post report that is bullish, with a pullback towards $8.70 buyable. New highs move lower support up to $8.70 and suggests that an old gap may be filled at $9.03.

- Dec meal prints a new contract low at $287.50, but the reaction after the report takes prices beyond key resistance at $295.00 toward the $300.00 level. The 100-day moving average is located at $301.00, and would look to go there.

- December soyoil futures trades back over 29c but has very good resistance at 2920-2930c. Prices are posting an inside day of trade, but would look for the 2860c level to likely hold and for prices to eventually test 2950c once more.

- Sep. corn prices pull back from newly placed highs yesterday and test the previous trading range highs of $3.39 with a $3.40 morning low. Good support now moves up to $3.35/$3.39 as new morning trading range highs hit above the 100-day moving average of $3.47. The target high now moves back to $3.55/$3.60 with the current market advance.

- Sep. wheat struggles to gain traction over $5.00 but the stabilization moves key support back to $4.80 for what could be a $4.80 to $5.15 trading range. Would look for wheat to not keep up the rally pace that the other markets have now entered into.

NOVEMBER BEANS

The previous trading range is from $8.55-$8.85, but prices topped the $8.85 level. The upside break-out suggests that prices will find buying interest on pullbacks, which increases the possibility that prices could close the open gap located at $9.03 given time. The trend still remains extremely weak with an ADX of only 17, meaning that rallies may be a slow climb. However, the vertical advance yesterday from the lows of $8.60 moved prices over all moving averages which turned $8.70/$8.72 into a buy-able level in a market that has yet to establish a new high for its trading range. The previous tops at $8.80 also offer up first support in a market that could target $8.92, and then $9.02/$9.03.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Corn, soybeans and soyoil all closed lower after trading up the previous three sessions. July soymeal made it a fourth trading session higher, and wheat remains on a tear with a fifth trading session closing higher. The mood around wheat sees supply concerns developing in North America and in t...

Corn, soybeans and soyoil all closed lower after trading up the previous three sessions. July soymeal made it a fourth trading session higher, and wheat remains on a tear with a fifth trading session closing higher. The mood around wheat sees supply concerns developing in North America and in t...

Cow-calf producer margins are discussed less frequently in these pages than their downstream counterparts of feedlot and beef packer margins, but this doesn’t mean they are less important to understanding the beef industry’s current state and outlook. Additionally, discussion of thi...

Cow-calf producer margins are discussed less frequently in these pages than their downstream counterparts of feedlot and beef packer margins, but this doesn’t mean they are less important to understanding the beef industry’s current state and outlook. Additionally, discussion of thi...