GOOD MORNING,

Prices continue to hammer out trading ranges heading into the end of the month, starting lower in the night session but reversing course to trade higher. The "easy" money now seems to have come to an end as volatility increases. The seasonal Jan/Feb. timeframe has arrived with a vengeance, as new shorts enter and old bulls fight it out. Weather has normalized a bit in SA, and Chinese buying, demand, and harvest are in front of us.

The markets are looking to head into wide sideways ranges now, with the only question being, is the downside over? This correction from the top has been deeper than the ones preceding it, but until funds dump 2/3 of their position and rallies are met with selling interest, the bull markets will likely continue. Net fund positions are now estimated at long 4K contracts of wheat, 341K corn, 131K beans, 85K meal, and 96K soyoil. Today, the soyoil bull looks to have the clear advantage as prices are on a rebound and approaching previous contract highs.

In terms of demand, weekly grain inspections were supportive for all the markets yesterday. It included 18 cargoes of beans destined for China, with a cargo of corn and 3 cargoes of sorghum as well. Corn shipments were noticeably higher than beans, however, and seasonally shipments begin to favor more corn and less beans as SA supplies come on board. For the moment, corn seems to be holding up better than beans, at least technically speaking. Marketing year to date:

--Corn shipments stand at 738 mln bu, or 29% of the USDA's projected 2.55 bln bu.

--Wheat export shipments total 592 mln bu representing about 60% of the USDA projected 984 mln bu, up from 57% a week ago.

--Bean shipments are 1.664 bln bu representing 74.6% of the USDA's projected 2.230 bln bu program, up from 70% week ago.

On a different note, China continues to sell wheat out of their reserves, and at some point they may need to replace that supply. The question is who will be the supplier? National restrictions on wheat continue to be supportive, and the Russian government has formally approved a proposal to impose a higher export tax on wheat from March 1. It will involve a €50/ton ($61) wheat export tax starting from March 1 to June 30, vs. the 25 euro/ton tax set for Feb. 15 to March 1.

WEATHER

--In South America, rains now continue to delay the harvest in Brazil, which was reflected in the cash movements at Paranagua and Santos where March and April shipments are now at parity on a flat price basis. Rains continue to help crop development in Argentina.

--In the US, a strong storm bringing snow cover crosses the upper Midwest from Iowa through Chicago. St. Louis received a record amount of rain for one day on Monday, though it was badly needed.

ANNOUNCEMENTS

Brazil estimated the average daily bean export volume through the third week of Jan at 116,000 mt vs. 63,500 mt /day year ago. The average daily corn export volume for the third week of Jan was an estimated 126.870 mt vs. 95,780 mt year ago.

Ukraine's Economic Ministry and unions representing grain traders and farmers have agreed to 20/21 MY corn export limit at 24 mmt, which is the same as the projection by USDA.

Corn imports in the EU for the week ending Jan 24 reached 150,346 mt, the lowest level since the start of the marketing year, as reported by the European Commission.

Ukraine's soft milling wheat export prices decreased by $3-$4/ton following softer global prices.

Delivery of grains and oilseeds to Argentine export hub Rosario is slowly returning to normal this week after protests by truckers last week that blocked roads leading from the farm belt to the port.

CALLS

Calls are as follows:

beans: 17-19 higher

meal: 4.00-4.50 higher

soyoil: 70-80 higher

corn: 9-10 higher

wheat: 4-6 higher

canola: 10.00-11.00 higher

OUTSIDE MARKETS

Firmer energy costs, with crude trading tup to $53.24/barrel, and the US dollar down to 90.38. Stocks are mixed with the Dow up 60 pts and the NASDAQ down 9 pts.

TECH TALK

Since we are officially in trading ranges, prices are now building on yesterday's recovery trade off the low. Look for any pullbacks to hold as trading range lows look to be in place, and prices are quickly taking back a large part of recent trading range losses, which is part of bull market behavior.

- March corn trends higher with trendline resistance now located at $5.25. Look to probably go there as prices now turn higher from lower. Would now continue to own pullbacks, as weaker markets do not recover from falls such as occurred last week. Key support has now been established at $5.00 as a value level with this week's strength.

- March wheat probed under $6.30 without downside follow-through, and recovery higher from lower promotes a move back towards $6.70/$6.75.

- March beans trends upward and would look for prices to likely approach the $14.00 mark again with a stop at $13.85/$13.88. The ADX remains strong, and the market drop in price reduced overbought situations to a manageable RSI at 57%, which makes it easier to own the market without an immediate threat of a correction. Look to re-establish a new range from $13.50-$14.00 in all likelihood.

- March soyoil charts are very constructive now, with lower lines of strong support at 4175c never even approached, while 42c became a point from which to go long. The move higher now favors a test of 4420c, and possibly a move back towards the recent highs at 4469c.

- March meal reaches a sell-off low of $417.00 but trades back towards $435.00-$438.00 resistance. This chart has put in the least amount of price recovery, as it looks to consolidate from $420.00-$435.00. However, the price action remains positive, so would look at the high likelihood that prices eventually trend back over $438.00 and back towards the middle of the trading range which is $455.00.

Pullbacks today that may hold for higher trade if wanting to long or cover a short:

March beans: $13.45

March meal: $430.00

March soyoil: 4340c

March corn: $5.17

March wheat: $6.45

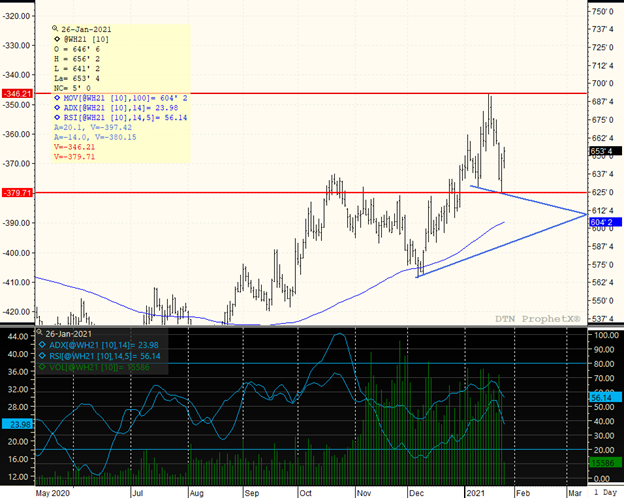

MARCH WHEAT

The major direction is sideways, with contract highs of $6.93 holding for a trip down to $6.30, the lowest end of the trading range for now. The market triggered sell-stops under $6.30 which took prices down to $6.24, but the weakness did not last and prices bounced into the middle of the trading range again. Would play the $6.30-$6.80 trading range, as prices continue to find little follow-through selling on wash-outs such as we saw last week. Could straddle/strangle this trading range with the ADX still showing a very weak trend with a reading of only 24. Funds are just about even wheat, with a minor long, but that could easily change on any break to the downside of $6.25. For now, would not want to sell this market until a confirmed close can occur under $6.30 with follow-through the next day. Given the chart set-up, there is more upside retracement potential than downside.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Corn, soybeans and soyoil all closed lower after trading up the previous three sessions. July soymeal made it a fourth trading session higher, and wheat remains on a tear with a fifth trading session closing higher. The mood around wheat sees supply concerns developing in North America and in t...

Corn, soybeans and soyoil all closed lower after trading up the previous three sessions. July soymeal made it a fourth trading session higher, and wheat remains on a tear with a fifth trading session closing higher. The mood around wheat sees supply concerns developing in North America and in t...

Cow-calf producer margins are discussed less frequently in these pages than their downstream counterparts of feedlot and beef packer margins, but this doesn’t mean they are less important to understanding the beef industry’s current state and outlook. Additionally, discussion of thi...

Cow-calf producer margins are discussed less frequently in these pages than their downstream counterparts of feedlot and beef packer margins, but this doesn’t mean they are less important to understanding the beef industry’s current state and outlook. Additionally, discussion of thi...

Reigniting a Transatlantic Deal Former Italian prime minister Enrico Letta is something of a policy rock star after authoring a report on the future strategy for the EU. Most of the 146-page report focuses on strengthening the EU’s internal Single Market but, buried at the end of th...

Reigniting a Transatlantic Deal Former Italian prime minister Enrico Letta is something of a policy rock star after authoring a report on the future strategy for the EU. Most of the 146-page report focuses on strengthening the EU’s internal Single Market but, buried at the end of th...