GOOD MORNING,

The major trends are shifting a bit, as traders continue to buy grains/sell soy, the opposite of the trend over the last several months. Good growing weather in South America is adding to supply pressure, even as more trade rhetoric turns negative. There are concerns over corn supplies left in the fields and lower global supplies of wheat (Australia's drought), puts wheat on a higher path.

Prices started the new month with another beating in the soy complex as new lows did not hold and led to more sell-stops. Traders were surprised at the extent of the sell-off in the soy complex in general. This morning, more hiccups arise for trade with Trump in London saying that a Chinese/US trade agreement may have to be put off until after the 2020 November election. Trump stated that he had no deadline in getting an agreement with China, and said in some ways waiting until after the election would be preferable. These comments are now baked into yesterday's sell-off in beans, which traded to the lowest levels since last Sep 9. Meal sits at new contract lows, and soyoil prices are testing the lower part of its new and higher trading range.

Corn appears ready to enter a more interesting phase of trade having held on to the lower $3.70's in March to actually stage a bit of a recovery rally. Ethanol production and export sales have picked up over the last few weeks, and the strong basis and lack of deliveries is inviting a few shorts to lighten up. Corn to ethanol is forecast at 5.375 bln bu, and a continuation of healthier ethanol production levels gives this market a bit of support. Corn demand still needs to grow to move this market to higher resistance levels, but it could be in the early stages for advancement. The size of the 2019 crop remains in doubt as winter weather arrives, while expanding livestock production points to increased feed use.

WEATHER

Quieter in the Midwest after the series of holiday storms marched through, bringing an end to harvest in parts of the northern plains. Focus is now South America, where rains continue to point to growing and thriving crops. Good weather in Brazil confirms ample 2020 supplies, and continues to cap off a market rally.

REPORTS

Crop progress:

Corn: 89% harvest was complete, which was only a 5% advance week to week, implying that over 9 mln acres were left out in the field, or about 1.4 bln bu. North Dakota was a stand-out with 2 million acres left, and with the recent weather it may stay out there into winter. North Dakota is only 36% harvested vs. 95% average.

Beans: 96% harvested, off 3% from the 5-year average. This indicates that there are 2.8 mln beans left in fields led by North Dakota (.452), Michigan (.258), Wisconsin (.249), and Indiana (.215).

Wheat: There were no wheat conditions reported this afternoon, which typically end the last week of November.

The commitment-of-trader's report was released as follows: disaggregated futures / options combined futures managed money flows as of Nov 26, 2019:

beans: net short 44,656

soyoil: net long 66,648 (reduced)

meal: net short 32,079

wheat: net long 8,359

corn: net short 116,947

The surprise in the report was that funds were not as short corn as expected. Funds have also been reducing length in soyoil.

USDA census crush for October was 187.2 mln bu, which was an all-time record, and up from 162.3 mln bu in Sep. Meal stocks were 335,183 tmt, and soyoil stocks were 1.82 bln lbs, vs. an expected 1.765 bln lbs.

USDA grain crush: corn for fuel alcohol was 436.78 mln bu.

Gist of report was supportive for beans and negative for soyoil.

ANNOUNCEMENTS

November Brazil bean exports were 5.158 mmt, which was unchanged from Oct., but 7% higher than year ago. Corn exports in Nov. were 4.288 mmt, down 29% from Oct., but 17% higher than year ago.

BUSINESS

After the close, Egypt announced a tender for 55,000 mt of wheat for shipment over the Jan 21/31 time period, of which the last purchase was comprised of Ukrainian and Russian origin. Wheat world values continue to firm, as they have over the last few weeks.

DELIVERIES

Dec soyoil: 878

meal: 319

CALLS

Calls are as follows:

beans: 1 1/2-2 higher

meal: .30-.50 higher

soyoil: 3-5 higher

corn: 1/2 lower

wheat: 3 1/2-4 higher

OUTSIDE MARKETS

The Dow is off 180 pts on Trump's comments, and ideas that a phase one deal may not be coming soon. Crude oil reacts by trading down to $55.53/barrel, with the US dollar trading to new lows at 97.74.

TECH TALK

- March corn prices are moving slightly higher and holding over $3.75-$3.80, which could become a new base of support in a slightly higher trading range. March corn gains more support at $3.80 given the chart price rise.

- March wheat could top out at $5.55 before the rally stops and is forming a classic pennant pattern of price congestion after a strong move up. Typically, prices tend to exit these pennants in the same direction we entered them, which suggests we could still leg higher one more time.

- Jan beans drop to a new trading range low at $8.67 1/2, close to the trading range low of $8.65. Oversold extremes at 20% now come into play, and at 18% relative strength index there is a strong warning that prices need to reverse and clean house.

- Jan meal places new contract lows at $292.60 without a good reversal signal as of yet. However, we do have a reliable price pattern of placing new lows and rejecting those quickly in this market. Would look for Jan meal to easily slide into a $290.00-$305.00 trading range.

- Jan soyoil continues to react to a topping pattern, finally breaking to new lows yesterday at 3011c, which is also at trendline. Any trade under 30c would near crossing lower moving averages of 2970c-2980c, and would be covering a short should we get there.

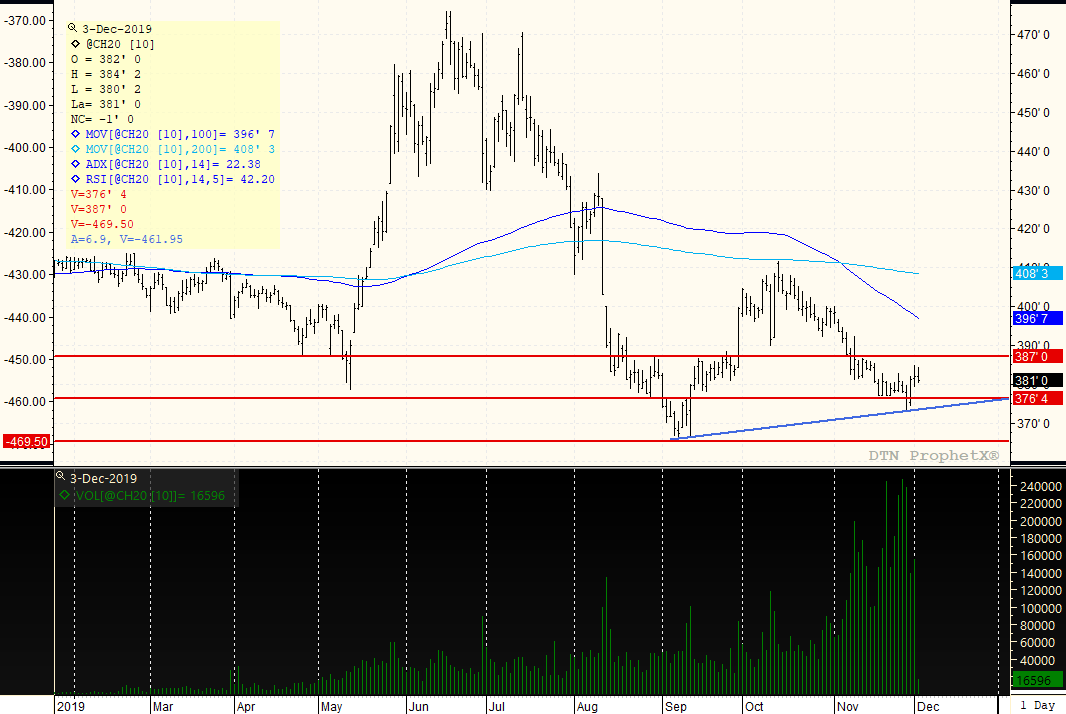

MARCH CORN

One clue of where a market is going to go is if it won't break and stay lower after a long decline, which is where the corn market currently is. Traders have been covering in their shorts on breaks, which is why prices are now holding intact over $3.80. Overall trading range could be from $3.75 - $4.05, and therefore we have been testing trading range lows over the last month. Seasonally, corn tends to rally from now into the springtime. Would look for the possibility that pullbacks continue to see more support which makes it harder to pullback towards the $3.70 level.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

The CBOT was mostly higher to end a mostly bearish week with wheat leading the way on several mildly bullish developments. Wheat futures saw price-supportive development in the IGC’s lower 2024/25 global ending stocks forecast, dryness in the U.S. Southern Plains, and smaller Russian 2024...

The CBOT was mostly higher to end a mostly bearish week with wheat leading the way on several mildly bullish developments. Wheat futures saw price-supportive development in the IGC’s lower 2024/25 global ending stocks forecast, dryness in the U.S. Southern Plains, and smaller Russian 2024...

USDA released the monthly Cattle on Feed report today. Total inventory, placements and marketings all came in lower than the pre-report estimates, though total inventory was at the same volume or higher than last year for the seventh consecutive month. Placements came in well below the average...

USDA released the monthly Cattle on Feed report today. Total inventory, placements and marketings all came in lower than the pre-report estimates, though total inventory was at the same volume or higher than last year for the seventh consecutive month. Placements came in well below the average...