GOOD MORNING,

Prices are lower as more organized rainfall hits key growing areas across Minnesota, Illinois, Missouri, and Iowa. Heavy showers pushed through the St. Louis area yesterday, dropping temperatures by 20 degrees. Today, the extreme heat is back. With the late plantings, the peak pollination period for corn appears to fall from July 20th to August 10th, much later than the usual July 4th period.

Weather maps are not in full agreement as to extended forecasts, but this week will continue to feature some of the hottest temperatures of the year.

Grains are leading in terms of weakness with longs liquidating part of their overall position.

ANNOUNCEMENTS

It was reported that the USDA Risk Management Agency may already have a running total of 2-3 mln prevent plant acres of beans as of early July, and 7-8 mln acres of corn. USDA Undersecretary Bill Northey said earlier this month that total prevent plant acres could go over 10 mln.

China's National Grain Trade Center reported 522,921 tmt of corn sold from state stockpiles, which was 13.5% of the volume offered into the marketplace.

Ukraine's Ag Ministry forecast 2019/20 grain exports at 1.7 mmt, well ahead of the same period a year ago when 778,000 tmt was shipped.

India's state-run weather bureau noted monsoon rains were 20% lower than average. In particular, beans received only 68% of normal rainfall in the period.

STORIES

US Treasury Sec. Mnuchin says he and USTR have a call later with Chinese counterparts, and in person trade talks could follow depending on how the call goes. Mnuchin said that Huawei is not the sticking point in trade talks.

Export sales were released this morning and South America and Ukraine got most of the corn business. Wheat sales were mid-range, with lower prices in the Black Sea and the EU covering most of the demand. Bean sales were at low end as China's demand is down due to ASF, and there are no good faith sales to China via trade talks. Meal was at the low end as well but better than expected for new crop. Soyoil sales are poor.

Calls this morning are as follows:

beans: 4-6 lower

meal: 90-1.10 lower

soyoil: steady

corn: 8-10 lower

wheat: 5-7 lower

CIF soybeans are weaker this morning. Processor bids are steady for the nearby with Cedar Rapids up 5c.

Outside markets feature crude oil at $56.42/barrel, and the US dollar at 97.26., slightly firmer. Dow is off 33 pts in early morning trade. China, Europe, and Japan equities all lower.

TECH TALK

Prices continue in trading ranges, but corn, wheat, and beans all feature potential topping activity, as noted by the special report put out yesterday. These tops foreshadow a possible further break in the market that is triggering some long liquidation in grains this morning, as their presence is neutral to bearish.

We have held these lower trading range low levels before, but patterns were not as far along, which makes these lows more susceptible to fail. Prices still have to close under all necklines to confirm head and shoulder tops.

- Bean and wheat charts have the best topping symmetry, while corn still appears as though it has wide trading ranges. Price action has been steady/lower all week, with a return to trading range lows.

- Nov beans have key support at $8.90, but trendline support a bit higher at $8.95. A close under $8.90 targets a return to the $8.65/$8.70 area.

- Dec meal is heading back towards $310.00, with an open gap still located at $309.00. For the past months the ability to retain the gap has been positive, keeping price action above key support. Closing the gap at $309.00 with a settlement under suggests we could test $300.00-$305.00.

- Dec soyoil bounces off 28c and has now congested once again between 28c-29c. A trade under 2797c, low of the last break, would take prices down to 2750c.

- Dec corn remains sideways from $4.20 to $4.65 and has been building support from $4.25-$4.30. The chart does not offer much back support if we break $4.30, and returning towards this important level lowers resistance down to $4.45 and suggests we more than likely see if $4.30 can hold again today.

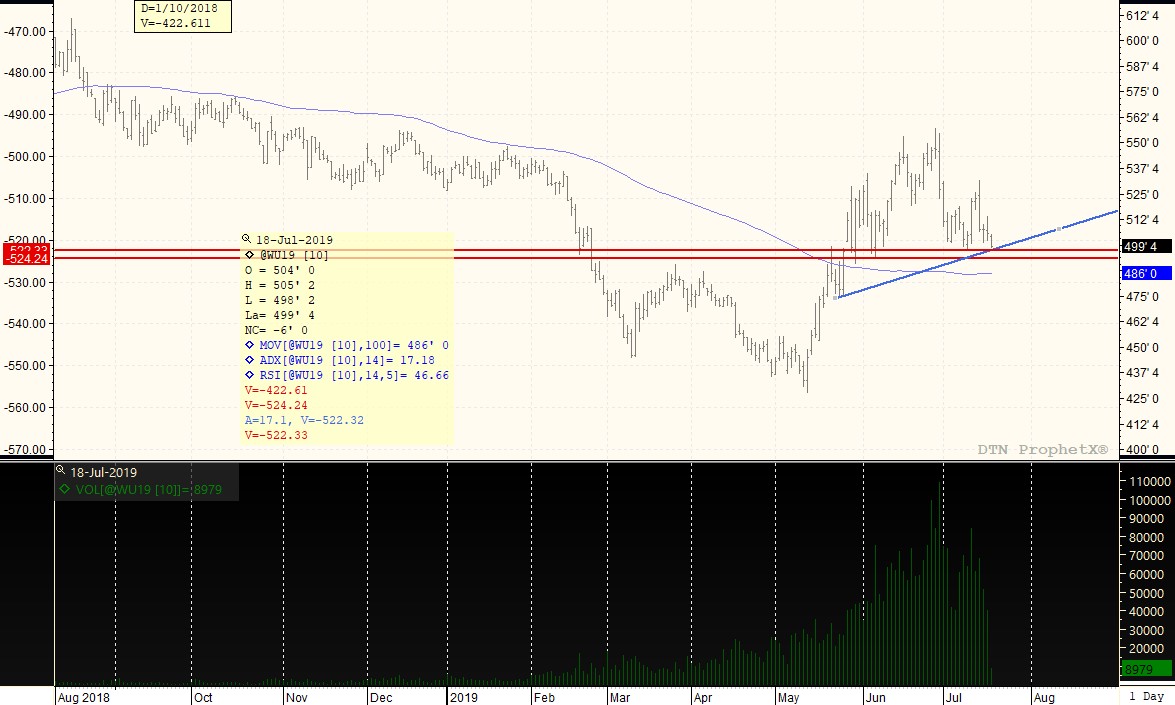

- Sep wheat is back at recent lows at $4.98, with the potential to have the largest downside if we cannot hold here.

SEPTEMBER WHEAT: Best potential reversal pattern for the morning is noted for wheat. September wheat features a very symmetrical head and shoulder potential top, which will only be confirmed with a close under $4.85. The failure to gain much traction on the wheat rally yesterday, stopping short at $5.15, with a return to the $5.00 level this morning, is creating long liquidation this morning. If prices trigger sell-stops under $4.95 with a close under it will trigger further losses as the pattern marks a major change of trend from higher to lower. So far, this chart has held its $4.95-$5.00 level of trade but returning to trading range lows time and time again eventually breaks support. Could sell this pattern only if we close under 4.85, which would more or less put a top in place. The lower blue line crosses with recent red line support at $4.98, making it a very big support area to begin the day.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Ocean Freight Comments - 19 April 2024 By Matt Herrington Spot dry-bulk freight markets remain weak amid dull April demand but rates are improving for May and June with improved interest in booking cargoes. Chinese demand for iron ore and coal has improved and bolstered capesize rates while gra...

Ocean Freight Comments - 19 April 2024 By Matt Herrington Spot dry-bulk freight markets remain weak amid dull April demand but rates are improving for May and June with improved interest in booking cargoes. Chinese demand for iron ore and coal has improved and bolstered capesize rates while gra...

The bearishness continues as South America crops loom and Northern Hemisphere weather is stable. The impending flood of Argentine soymeal and soyoil onto the market sent the May soyoil contract to a new low. There was nothing in today’s weekly USDA Export Sales report to alter the...

The bearishness continues as South America crops loom and Northern Hemisphere weather is stable. The impending flood of Argentine soymeal and soyoil onto the market sent the May soyoil contract to a new low. There was nothing in today’s weekly USDA Export Sales report to alter the...