WPI Spotlight

The WPI Spotlight showcases the best analysis recently written by our analysts.We've chosen to share these articles so you can see how we approach market and policy analysis and see the value for yourself.

Enjoy reading this collection of "best of" articles and feel free to contact us with any questions.

In my near 40 years in the business, no truer words have been spoken that what I've read in Ag Perspectives. WPI Client and Risk Manager

Subscribe now for full access to our "best in class" analysis.

For corporate subscription pricing, please contact us.

This article originally appeared in the 10 October 2023 issue of Ag Perspectives

By Matt Herrington

As WPI readers already know, Saturday morning brought news that Hamas and Hezbollah fighters from Gaza launched an unprecedented attack on Israel and captured several towns in the south of the country. Israel has declared war in response and launched a military campaign to retake its towns and retaliate against the terrorist organizations. As one would expect, this sent crude oil futures sharply higher and broader commodity market joined in the rally, at least initially.

Grain markets shouldn’t be affected by the conflict, other than that rising oil prices and inflation tend to support commodity values, but headline-reading algos are more sensitive to attacks and wars after the Russia-Ukraine war. Traders seemed to realize this fact as, after early rallies, corn futures and the soy complex settled lower while waiting for this week’s WASDE. Wheat futures managed to settle higher due to unconfirmed rumors of export sales from the U.S. Funds were slight net buyers in the wheat market, though commercial activity is rumored to have been more signifcant, and were net sellers again in corn and the soy complex. This week’s trade looks to be driven by the war in Israel/Gaza and pre-WASDE report positioning.

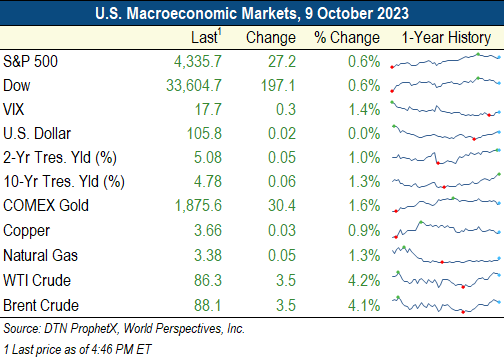

Discussion of macroeconomic markets must start with the weekend attacks on Israel by Hamas and Hezbollah that rattled global politics and oil markets. While Israel and Palestine are not major oil producers, oil markets are always jumpy when the word “war” hits newswires, especially if it involves the Middle East. Moreover, the bigger threat is that major oil producers in the region may now have a harder time balancing hardline and moderate factions within their own countries. The Wall Street Journal’s report that Iran helped plan and finance the Hamas attacks (which Iran has officially denied) added greater uncertainty to the Middle East oil and political situation. The weekend’s events don’t change immediate, fundamental supply/demand for oil, but rather introduce a significant escalation in regional tensions and broader risks to the world supply outlook. Crude oil futures finished 4+ percent higher for the day with spot WTI futures above $85 again and now targeting the $90 mark.

Stock market trading looked very typical for days when war “shocks” are introduced: safe-haven assets like gold and the U.S. dollar rallied while U.S. stocks wobbled initially. Defense and aerospace stocks surged and posted their best one-day gains since March 2020 on the day and led broader rallies that came after Israel announced it re-took several towns from Hamas control. Trading in U.S. Treasury bonds was closed Monday due to the Federal holiday but futures on the bonds pointed to rising prices (and therefore lower yields) as investors move money into safe-haven assets.

Notable Market News

Indonesia’s 2023 biodiesel consumption may only hit 11.5 million kiloliters (MKL), short of the 13.15 MKL target set by the government. The government previously mandated a 35 percent palm oil-based biodiesel blending requirement and expects to maintain that requirement in 2024.

On Friday, Russian Agriculture Minister Dmitry Patrushev said the country will start delivering grain to African countries within 4-6 weeks.

A Bloomberg survey of analysts pegged the Brazilin 2023/24 soybean crop at 163.9 MMT, which would be 9 MMT above the 2022/23 crop and a record high. The survey also estimated the corn crop at 130 MMT, well above CONAB’s preliminary estimate of 119.8 MMT.

The Rosario Grain Exchange pegged the Argentine 2023/24 wheat crop at 15 MMT but noted downside risk remains due to limited rains. WPI’s in-country analysts say a 15-MMT crop is becoming an “optimistic” outcome given the current scenario.

Argentine farmers have sold the smallest amount of wheat in the past 7 years as uncertainty regarding the harvest (which occurs in November and December) grows. Drought in parts of the country has forced the early abandonment of some fields while the quality of others will likely only be fit for feed use. Farmers are also reluctant to lock in a price ahead of the October general elections, which will likely see a new government take office on 10 December. Regardless of what party takes power, further currency devaluations are expected, which would lower the effective price farmers receive for their grain.

Russia bombed the Ukrainian ports of Odesa and Mykolaiv again overnight in effort to stymie Ukrainian exports and enhance their competitive position on the world market.

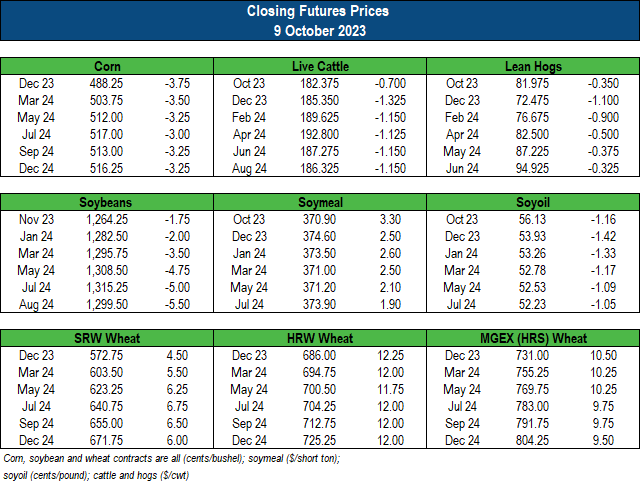

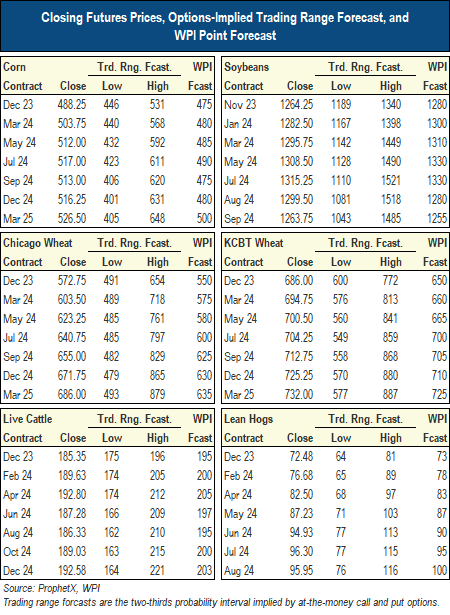

Corn

Futures

The weekend attacks on Israel by Hamas sent crude oil and most commodity markets higher on Monday morning, and corn was no exception. December futures rallied initially but again uncovered resistance near the $5.00 mark that turned back the rally. The market then drifted lower into the close with favorable weather for the U.S. harvest and a bit of risk-off trade before the WASDE pushing values into the red. December futures settled 3 ¾ cents lower in light-volume trade for the day and uncovered support at the converging 10- and 50-day MAs. Technically, corn is still in a short-term higher trend but December futures’ inability to break the $5.00 mark is a growing liability for bulls. WPI looks for steady/sideways trade this week heading into the October WASDE.

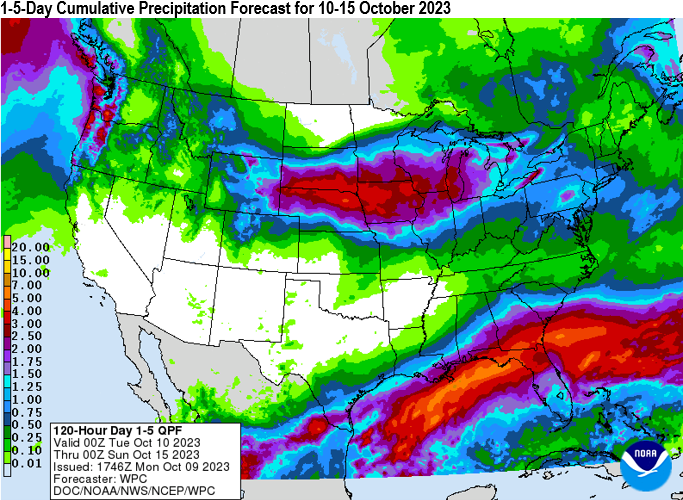

Fundamentally, harvest progress over the weekend should have been strong and the USDA’s Crop Progress report will be out Tuesday afternoon, due to Monday’s Federal holiday. Parts of the Western Corn Belt and Northern Plains saw freezing temperatures over the weekend that will have impacted late-maturing crops, but widespread frost/freeze damage is not expected. Temperatures and freeze risks will remain this week but the bigger concern is rains that will likely disrupt harvest across much of the Midwest starting at mid-week. Threats to corn yields and harvested acres are minimal so far, however, as the 6-10-day outlook turns dry again.

Soy Complex

Futures

Soybeans initially traded higher but settled slightly below unchanged after a day of two-sided trade. The bullish influence came from rising oil prices after the weekend attacks in Israel while bearish pressure came from weak soyoil values and a 4.3 percent plunge in China’s Dalian soybean futures. November CBOT futures settled 1 ¾ cents lower in moderate volume and clung to their recently-established sideways trading range ($12.56 ¾ to 12.87 ¼). Like corn, the weekend weather was favorable for harvest and strong progress is expected in tomorrow’s Crop Progress data. The 1-5-day outlook is wetter than ideal for the Midwest this week, but models currently suggest a drier trend thereafter that should facilitate better harvest progress. Weekend reports of frost/freeze damage were minimal and the 2023 crop seems to have escaped relatively unscathed much of the weather risks Mother Nature has thrown so far.

Soymeal futures bounced higher to start the week with October futures up $3.30 after no new deliveries were reported from Friday’s close. The December contract rose $2.50 in moderately heavy volume with support emerging just above $370 and resistance forming about $2 below the resistance trendline. Soymeal is in a long-term downtrend that started in late August but is currently consolidating just above major support at $361.80.

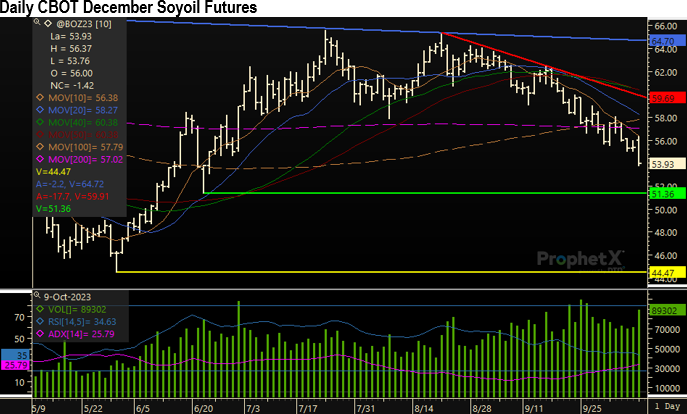

Continued weakness in RINs prices pressured the soyoil market, despite strong gains in crude oil futures. Palm oil futures were also lower for the day and helped create some pressure in soyoil after India announced its palm oil biofuel blending program will fall short of government mandates. December CBOT soyoil posted a massively bearish outside day on the charts and settled 1.42 cents/lb lower in heavy volume trade and scored a new selloff low for the day. The contract settled below psychological support at 54.00. The contract is accelerating in its current downtrend and continues to target support at 51.36.

Wheat

Futures

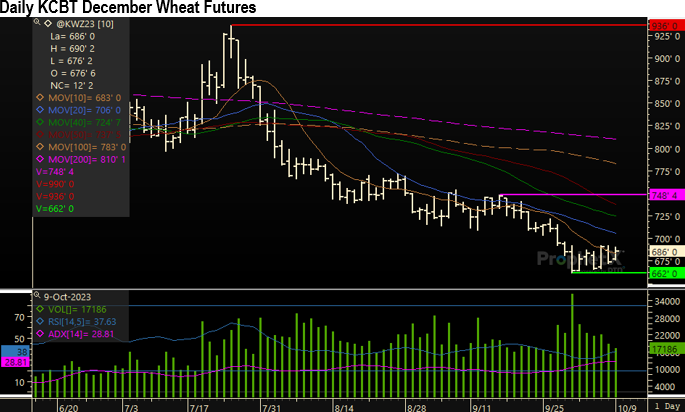

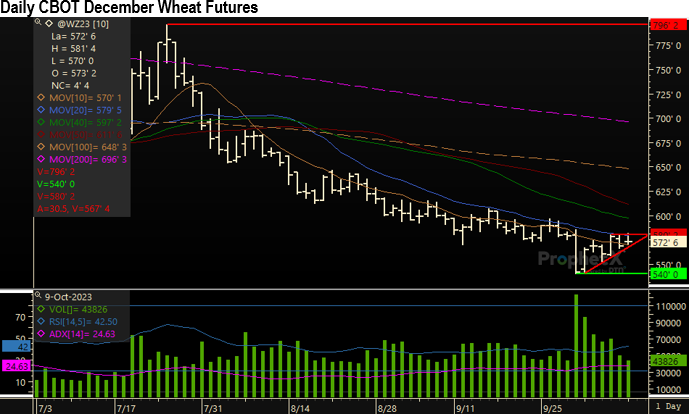

Wheat futures moved higher to start the week on rumors of possible U.S. export sales to unknown destinations. The rumors are yet unconfirmed but follow China’s recent purchase of U.S. SRW wheat. There was some bull December/March spreading in the KCBT market, which would suggest growing nearby commercial demand, if not export sales. December KCBT futures settled 12 ¼ cents higher while the March contract rose 12 cents by the close. Both contracts saw light-volume trade and stuck to inside days on their respective charts as the KCBT market remains in a sideways consolidation mode.

December CBOT wheat settled higher to start the week as well, but trading volume was light and markets could only muster inside days on their charts. The contract found resistance near $5.80 for the third straight day, with bulls unable to gain traction above that point. On the charts, December CBOT is forming a bullish ascending triangle (the red lines near today’s close) and the market is close to breaking out from this forming. Technically, WPI favors an upside breakout and the 40-day MA ($5.97) would be the initial upside target. A break below the triangle, however, would constitute a failed signal and likely force a test of contract low support at $5.40.

Cattle

Futures

Live cattle futures turned lower Monday after last week’s cash trade came in slightly lower than the prior week and as rising oil values and conflict in the Middle East sparked macroeconomic and recession concerns. December live cattle settled $1.325/cwt lower and posted an inside day on the charts in low-volume trade. The February contract posted a similar day with a $1.15/cwt lower close in a day that amounted to little from a technical trading perspective. The live cattle markets just finished the fifth straight consolidation day and have not rallied back from their recent selloff as bulls hoped. Moreover, resistance is forming at the 40- and 50-day MAs in both the December and February contracts, adding to headwinds for bulls. WPI remains bullish the cattle market from a fundamental standpoint but we are increasingly concerned/bearish about the technicals. The 100-day MA and mid-August lows are the next support levels for the December and February contracts.

Cash cattle markets saw thin trade to start the week and USDA reported just 430 head sold in negotiated trade. Prices were above last week’s weighted average as live FOB cattle sold for $183.43/cwt (up $0.70/cwt), but the volume of trade is too light to be a reliable indicator of this week’s trend. Beef markets were higher to start the week with the Choice cutout up $1.41/cwt and the Select cutout up $1.72/cwt.

There are no deliveries yet against the CME’s October live cattle futures contract, which has historically seen large numbers of deliveries.

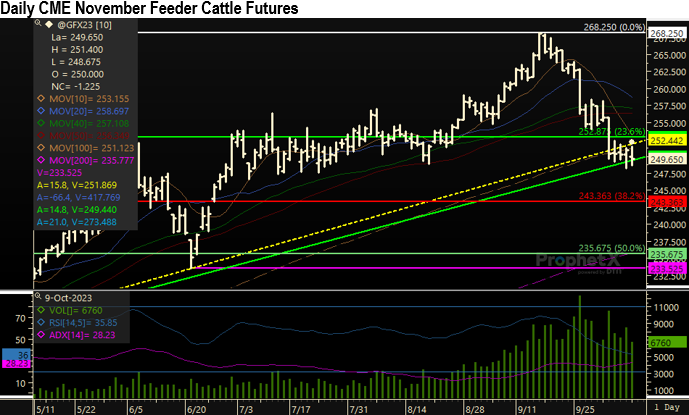

Feeder cattle futures continue to decline with speculators adopting risk-off trading and positioning amid weaker live cattle markets and macroeconomic concerns. November feeder cattle settled $1.225/cwt lower but managed to claw their way back from lows that were $2.20 under Friday’s settlement. The contract again settled above trendline support but drifted below that point as well in a signal that technical support at that point may not be as strong as expected. A settlement below the trendline ($249.44) will likely spark another significant rush for the exit that could take values into the $240 range. Not that there is an unfilled chart gap at $242 from the 27 June opening and that a selloff to $243.36 would complete a 38.2 percent Fibonacci retracement. '

Lean Hogs

Futures

Lean hog futures traded both sides of unchanged to start the week with strength in the cash hog market both Friday and Monday afternoon seeming to offer little support. December futures settled $1.10/cwt lower but the contract only marked time on the charts with an inside day in moderate volume trade. The December contract saw the bulk of the day’s selling pressure and was the recipient of bear spreading as deferred futures saw smaller losses. February futures settled $0.90/cwt lower in a similar day on the charts, essentially taking a respite from the past three days’ rally. Lean hog futures are technically still swinging higher but resistance is quickly approaching overhead with the 100-day MA threatening to stall the December futures rally at $74.33 and old trading range resistance above that at $76.72. In February futures, the downtrend line is threatening the rally at $79.41.

Cash hog prices dipped $0.36/cwt on Monday morning’s National Daily Direct report after Friday afternoon’s strong gains. The morning’s trade was light at 1,766 head while the afternoon saw greater activity with 6,959 head sold. The afternoon prices were up $0.89/cwt from the prior day at $74.81/cwt. The pork cutout rose $1.84/cwt Monday afternoon with a $13 gain in pork bellies and a $2.88/cwt-gain in loins.

Closing Futures Prices

This article originally appeared in the 17 October 2023 issue of Ag Perspectives

By Dave Juday

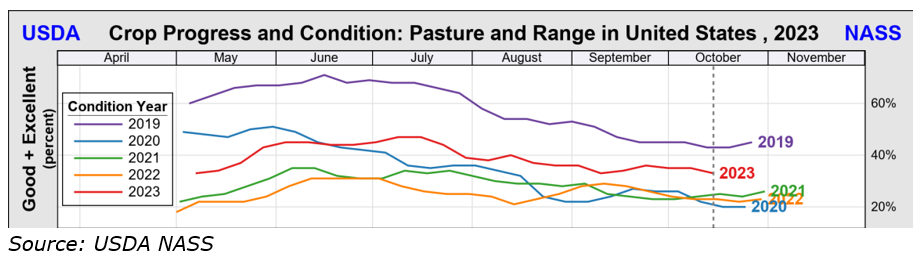

Pasture conditions are deteriorating as 2023 comes to a close and the grazing season closes out. This has potential implications for the rebuilding of the cattle herd. As of 15 October, conditions have improved over the last three years, but are not back to pre-drought levels. Going into the winter without sufficient forage is clearly an obstacle to herd expansion – and the reason why beef cow slaughter peaked in Q4 in all but six of the last 50 years. How much it peaks is something to watch this year.

One positive is that hay supplies are up. Production in 2023 is up 10 percent for alfalfa and 8.1 percent for other hay. But the bigger question with beef cattle herd rebuilding leads to question about the structure of the cow calf sector going forward. That segment of the value chain has changed least over the years compared to all the others. One issue to consider is how the trend in beef on dairy breeding will fit in the future of

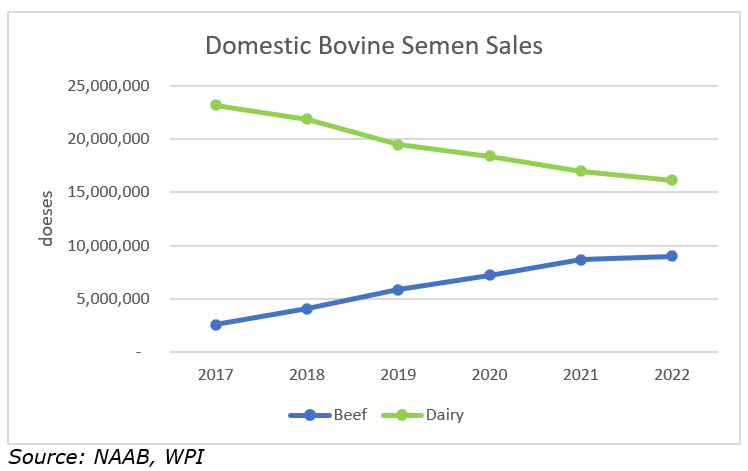

This trend is evident in the sales data for beef semen as reported by the National Association of Animal Breeders (NAAB). Over the past six years, dairy semen has dropped by about 7 million doses, while beef semen sales have increased by about 6.5 million doses. These trends are irrespective of relative changes in the beef and dairy herds. Further, as reported by NAAB, 49 percent of dairy semen doses are now sexed semen, which facilitates beef on dairy breeding.

All dairy cattle move toward beef production ultimately so there won’t be an increase in supply, but the change that beef on dairy brings is from selling dairy steers at a discount to selling feeder cattle at a premium over straight dairy steers. Those cross bred calves are also more efficient in rate of gain. Backgrounding cross bred calves takes fewer days and improves rate of gain efficiency in the feedlot.

Genetics companies continue to invest in optimum beef on dairy genetics which will only make these calves increasingly more valuable, and result in more going into branded beef programs and less into processing beef. Some feeders are offering dairies contracts for cross bred calves if they are bred following certain protocols and by using the genetics the feedlot prescribes. This trend of beef on dairy has been unfolding for some time, but the rebuilding of the beef herd may be a catalyst toward faster adoption.

This article originally appeared in the 3 May 2021 issue of Ag Perspectives

By Gary Blumenthal

We regret to inform long-time Ag Perspectives readers of the passing of Robert Kohlmeyer. Bob had a long and prolific career, first with Cargill and then with WPI.

He spent the first 34 years of his professional career doing everything from managing Cargill’s elevator operations to leading the company’s futures trading desk. He was a key trader for the company during the so-called Great Grain Robbery with the Soviet Union in 1973, and later the grain embargo against the same USSR in 1980. He would later testify several times before the U.S. Congress on the machinations of the grain trade and government policies. In a classic phrasing by Bob before a House committee in 1978 he said,

The role of the private exporter in this process is to move commodities from surplus-producing areas to deficit consuming areas in the most efficient and timely manner possible.

Bob brought his amazing insights and expertise from Cargill to World Perspectives in 1990 where he continued to educate both clients and government officials for another 30 years. Younger analysts would leave a company meeting and talk about the pearls of wisdom that would drop from Bob’s lips. He would cite old market sayings like “the market is bigger than me and thee”; and “he is your friend, but he is mine for an eighth”. While he cited the advantages of directly engaging other human beings in the Chicago trading pits, he fully embraced the digitalization of the industry and talked about the advantages of modern telecommunications.

Bob was a history major at Princeton and saw the cyclicality of the agricultural commodity markets. Thus, in his later years he wrote a series of articles called Common Thread in which he detailed the commonality of the present with past market events. His last article for WPI was late last year before illness stole his energy. His wife Julie says that it was his hope that he could resume writing for Ag Perspectives that kept him going through his illness. Whether you knew Bob Kohlmeyer or not, the legacy of his work has left a lasting impact on our industry. We will miss him dearly.

This tribute was originally published 24 March 2020.

It is with a heavy heart that we share with you that World Perspectives founder Carole Brookins died last night after succumbing to the COVID-19 virus. She was 75 years old. She fell ill after returning to Palm Beach from Paris two weeks ago. She had a storied life, breaking barriers and making things happen.

To no one’s surprise, Carole graduated cum laude from college and began her career as a municipal bond underwriter in Chicago. She then became a market reporter at the Chicago Board of Trade where she came to the attention of the second largest stock brokerage firm, E.F. Hutton. In the 1970’s she rose to become their Vice President of the Commodity Department. A little-known fact - Carole created, developed and presented the firm’s two-record album on investing called, “Learn a New Language: Money.”

Carole left Wall Street to create World Perspectives in 1980, saying she was motivated by the grain embargo against the Soviet Union since it revealed the information gap between policymakers and the trade. Because of her intellect and spunk, she was in high demand throughout her life giving public speeches and providing valuable insight. And, she attracted Washington’s most powerful as headliners at the annual conferences she would orchestrate.

One woman who met Carole back at that time responded to her passing yesterday by saying, “Carole was a powerful role model for me and many other young staffers on the Hill, in trade, business and agriculture.”

Presidents appointed her to various advisory committees and, perhaps hearkening back to her municipal bond days, she led a multinational effort in Asia in the 1990’s to build out secondary cities and create rural linkages. She was on corporate boards both before and after her appointment and U.S. Senate confirmation as U.S. Executive Director at the International Bank for Reconstruction and Development (the World Bank).

She did not slow down after her stint as a top government executive. She continued giving speeches and working through various partnerships to make economic linkages where she knew they should be but did not exist.

Carole derived her mojo from engaging with her hundreds of friends and acquaintances located around the world. It is unknown how many different countries she visited during her lifetime, but she likely missed very few. In her final years, she split time between her two favorites, the U.S. and France. Reflecting her love of both countries, two years ago Carole invested her time, her energy and her personal wealth to create the First Alliance Foundation, which memorializes the historical Franco-American relationship.

Carole was smart, she was industrious, she was always a whirlwind of ideas. She was a dear friend and close advisor. This virus took down someone very special and the world will be worse off for it. We at World Perspectives will miss her very much.

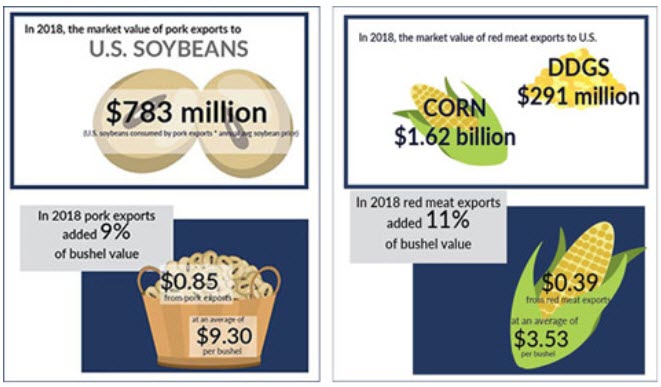

Beef and pork exports added 85 cents per bushel to the price of soybeans and 39 cents per bushel to the price of corn in 2018, according to the latest report by World Perspectives Inc. (WPI). Over the past three years, WPI has analyzed the impact of U.S. red meat exports on the value of domestic feedgrains and oilseeds.

Among new information included in the latest report are statistics that point to the value of red meat exports to U.S. soybean producers. According to WPI, the market value of pork exports to the soybean industry in 2018 was $783 million. WPI’s updated study shows that without red meat exports, U.S. soybean farmers would have lost $3.9 billion last year and U.S. corn growers would have lost $5.7 billion.

The updated report includes a projection of domestic feed use impacts based on both the long-term 10-year baseline projections for meat exports and a special analysis of the critical importance of the proposed U.S.-Japan trade agreement. USMEF has also prepared state-specific statistics on the value of red meat exports to the top 15 soybean states and top 10 corn states.

“The World Perspectives study has been a very useful tool in quantifying the importance of red meat exports to our corn and soybean member organizations,” said USMEF President and CEO Dan Halstrom. “Results of the study and the subsequent updates demonstrate that maintaining global market access for U.S. beef and pork is critical to continued growth and to the continued value that meat exports bring to corn and soybeans.”

The updated study also looks forward, projecting that U.S. pork exports are expected to generate $8.68 billion in market value to soybeans from 2019 to 2028. Red meat exports are expected to generate $19.1 billion in market value to corn and $3.1 billion in market value to distiller’s dried grains with solubles (DDGS) in that same period.

“When the original study came out a few years ago, it gave us a good look at the value of U.S. beef, pork and lamb exports to corn and soybean farmers,” said Dean Meyer, a corn, soybean and livestock producer from Rock Rapids, Iowa. Meyer, a member of the USMEF Executive Committee, noted that the WPI study continues to support the fact that exporting red meat drives demand for livestock, in turn driving demand for livestock feed.

“The updated study offers a fresh look at corn and goes a little deeper into soybean meal and what red meat exports mean for soybean growers. As grain farmers, we are aware that meat exports add value by increasing the volume of soybean meal and corn used to feed cattle and hogs, but the numbers in this study provide a clear picture of just how important those exports really are,” said Meyer.

USMEF and the National Corn Growers Association initially commissioned WPI to quantify the impact of U.S. beef and pork exports on corn use and value in 2016, using 2015 data. Record-setting growth in red meat exports since 2016 – along with an uncertain global trade climate that has developed since the original study – led USMEF to request updates. Using final 2018 data and new 2019 to 2028 USDA baseline projections, WPI updated its analysis of red meat exports’ impact on corn in 2018 and expanded the analysis of the value of pork exports to soybeans.

Highlights from the updated WPI study include:

- Since 2015, meat exports represent the fastest growing category of corn and soybean meal use.

- In 2018, exports accounted for:

- 14.6 percent of total U.S. beef production;

- 25.7 percent of U.S. total pork production;

- 459.7 million bushels of corn utilization – with a market value of $1.62 billion at the year-average market price;

- 2 million tons of soybean meal disappearance — the equivalent of 84.2 million bushels of soybeans with a market value of $783 million.

- In 2018 beef and pork exports added an estimated $0.39 to the average 2018 corn price of $3.53/bushel, and pork exports added $0.85 per bushel to the average 2018 soybean price of $9.30/bushel.

- Since 2015, one in every four bushels of added feed demand for corn was due to beef and pork exports, and one in every 10 tons of added feed demand for soybean meal use was due to pork exports.

- Over the next 10 years, meat exports are forecast to generate a projected $30.8 billion in cumulative annual market value to corn and soybeans based on USDA’s long-term forecast for crop prices.