GOOD MORNING,

Prices started the night lower, but head into the close higher into today's important WASDE report, one that could determine trend over the next several weeks. Jan and Feb timeframes are typically negative for US markets as early harvest begins in Brazil, but this year La Nina pushes that timeframe back. Rains in South America pressured the market a bit, but this is all about positioning into the report. Funds stand heading into the report long an estimated 400K contracts of corn, 11K wheat, 175K beans, 100K soyoil, and 75K meal. Typically, when funds are all on one side of the market it spells trouble. The report and weather moving forward will determine whether the bull boat continues to float or sinks. Full steam ahead into the report at 11:00 Central time, where we see new data on US ending stocks, quarterly stocks, world stocks, and US winter wheat seedings.

Average estimates of ending stocks:

beans: 139 mln bu vs. 175 mln bu in Dec.

corn: 1,599 mln bu vs. 1,702 mln bu in Dec.

wheat: 859 mln bu vs. 863 mln bu in Dec.

Quarterly Dec. 1 stocks estimate:

beans: 1,290 mln bu vs. 3,252 mln bu yr ago

corn: 11,951 mln bu vs. 11,327 mln bu yr ago

wheat: 1,695 mln bu vs. 1,841 mln bu yr ago

World demand continues to be a supportive feature, and the USDA will have to dial that into their report today. China's bean imports from the US for 20/21 could surpass its annual US imports for 2015/16 by the end of the month, according to OCBC, as imports remain strong and only half the season has passed. Prices may have to remain in rationing mode, particularly if weather turns back dry for SA by the last half of the month.

WEATHER

Better rains in Brazil were noted along with better than expected rainfall in Argentina. Conditions will turn drier into the last half of January, and over the next 30 days 55-60% of Argentina could see less than normal rains, according to long range forecasts. Brazil is expected to see rains in the northeast but conditions are still trending dry than normal over the next 30 days.

ANNOUNCEMENTS

Russia will consider changes to its wheat export tax by the end of this week, according to the economy minister. Russia is considering raising the tax from the planned 25 euros, ($30) per ton, to 50 Euros between Feb. 15 and June 30.

Argentina farmers said they would continue their ban on selling crops despite the gov. decision to amend the corn export suspension that triggered the sales strike. This remains supportive for the bean market, taking hedge pressure off the market.

China's Ag Ministry monthly data forecast 20/21 corn imports rising to 10.0 mmt, up 3.0 mmt from the prev. forecast, attributing the increase to demand for feed from recovering pig her and increased domestic corn prices. The data also showed feed corn consumption at 185 mmt, up 2.0 mmt from the prior outlook.

DELIVERIES

Jan beans: 70 Cunningham puts out 65, Wells Fargo stops 62

CALLS

Calls are as follows:

beans: 6-8 higher

meal: 2.40-2.60 higher

soyoil: 30-35 lower

corn: 1-1 1/2 higher

wheat: 9-11 higher

canola: .30-.50 higher

OUTSIDE MARKETS

Feature a continuing strong crude oil market at $52.07/barrel, with a weaker US dollar which trades down to 90.30. The stock market is up 70 pts.

BUSINESS

Egypt tendered for wheat after the close for Feb/March timeframe, and have received only 4 offers this AM.

TECH TALK

- March soyoil futures takes another leg lower after moving under 43c to test 42c, where major support is located. This market could be forming a top, but the uptrend still remains intact with an ADX of 48, so if short this is a very good place to cover something in, price if needing to, or try the long side of the market. The rally into contract highs of 4469c started here, and therefore it makes a completion cycle downward. Could see some meal/soyoil correction after the start of the day.

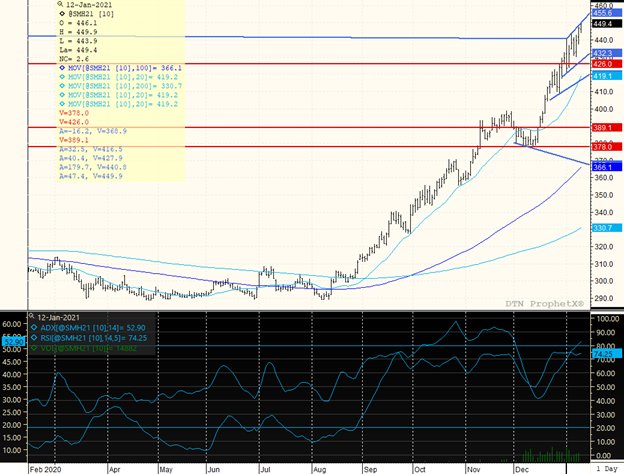

- March meal trades close to major trendline resistance, which is today at $450.00, with a new contract high of $449.90. First support moves up to $442.00, and the upside does not appear to be finished even though $450.00 is major trendline.

- March beans is in congestive mode from ctr highs of $13.88 3/4 to trading range lows of $13.55. The major trend is higher, and unless prices break the bottom of an ascending triangle, the low of which crosses today at $13.50, would stay long, price, or cover a short on a hard break. Target highs are still $14.00, and the market top has not yet been defined.

- March corn corrects down to $4.89 and looks slightly more vulnerable to a further downside correction. Having said this, the ability to stay positioned towards the recent ctr highs of $5.02 3/4 is more bullish than bearish, which increases the chance for trade back over $5.00.

- March wheat remains a sideways affair, holding the lower $6.30's to trade back towards $6.50. Could continue to straddle/strange $6.00-$6.50, with upside targets of $6.75.

MARCH MEAL

March meal continues to be a very strong market, pushing up against major trendline resistance which is at a new ctr high of $449.90. This level is right against the top trendline, with overbought conditions of 74%. The trend remains very strong with an ADX of 52. If long, would probably elect to take part of it off the table, though there are no signs of a top and prices remain well bid. The top line of blue resistance continues to slant up towards $460.00, and given the strong bid in the market that is the next target. For now, would consider the overall range from $430.00, which has moved up from $420.00, with a target high at $450.00 just about hit.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Most of the major agricultural commodity contracts opened today’s trading session in the red and stayed that way to the close. Only feeder cattle and lean hogs managed small gains on the day. New contract lows were hit for December soyoil, September SRW and September HRW. Volume was overa...

Most of the major agricultural commodity contracts opened today’s trading session in the red and stayed that way to the close. Only feeder cattle and lean hogs managed small gains on the day. New contract lows were hit for December soyoil, September SRW and September HRW. Volume was overa...

Non-Meat: In a first, a Europe-based company has sought EU approval to market lab-grown meat, in this case fake foie gras. Some member states have already banned such products. While lab-grown meat remains expensive, and plant-based meat substitutes have faced declining popularity, the increase...

Non-Meat: In a first, a Europe-based company has sought EU approval to market lab-grown meat, in this case fake foie gras. Some member states have already banned such products. While lab-grown meat remains expensive, and plant-based meat substitutes have faced declining popularity, the increase...

June 2024 total red meat and poultry stocks were up slightly from May but 5.4 percent below June 2023 levels due to sharp declines in poultry and pork stocks. Total poultry stocks were down 7.8 percent year-over-year (YoY) due to reductions in broiler slaughter for the month. Total pork stocks...

June 2024 total red meat and poultry stocks were up slightly from May but 5.4 percent below June 2023 levels due to sharp declines in poultry and pork stocks. Total poultry stocks were down 7.8 percent year-over-year (YoY) due to reductions in broiler slaughter for the month. Total pork stocks...