GOOD MORNING,

The night session featured a higher wheat market vs. lower markets elsewhere, supported by Matif corn and wheat that gapped into new highs overnight. Russia's restrictions and export taxes, ($1.65 export tax on wheat exports after March 1), could mean that as much as 5-7 mmt of Russian export demand may have to go elsewhere. Corn prices were lower but found good commercial pricings at lower price levels. Beans led the way lower on the back of better than expected weekend rainfall in Argentina.

Brazil crop production has gotten enough to stabilize crops for the moment. Beans encounter a sharper fall than corn, as the planting season begins along with the fight for acreage. This is the time of year when corn typically can hold up better, as harvest begins to ramp up in Brazil. For now, the bean harvest is off to a slow start. As to US production, the bean/corn ratio is now at 2:60:1, which continues to favor corn over beans.

While weather is a bit better in SA, good world demand continues. China's customs data showed that grain imports soared to record highs in 2020, after tight domestic corn supplies pushed prices to multi-year peaks, driving demand for cheaper imports. China purchased a record 11.3 mmt of imported corn last year, including 2.25 mmt in Dec. alone. After Russia announced wheat export restrictions, Ukraine's grain traders said they would probably not restrict 20/21 corn exports, a move requested by animal feed and meat producers to try to stop higher feed prices. Ukraine is a key competitor for supplying corn. The ag ministry said they would decide on Jan 25 whether to limit corn exports to 22 mmt.

In politics, Brazilian truckers are threatening a strike Feb 1. due to higher fuel costs and lower freight rates.

WEATHER

Brazil is trending wetter with improvements in crop conditions, though the slow start to harvest already implies that production will be smaller. Argentina is seeing timely rains bring more relief to crops this weekend, with more moisture reserves this time around in front of a drier last half January.

REPORTS

Commitment-of-Traders report disaggregated futures / options combined as of Jan 12:

Beans: net long 166,486

Meal: net long 84,408

Soyoil: net long 93,536

Corn: net long 374,714

Wheat: net long 16,987

The COT was neutral to constructive, showing smaller than expected long positions across the board. Funds sold products and beans.

ANNOUNCEMENTS

Brazil's AgRural put bean harvest at a slower -than-expected start with just 0.4% vs. 1.8% year ago. Good rains and lower temperatures in many areas in Jan. so far are helping the crop develop. Regions that were dry such as Rio Grande do Sul, Maranhao, and Tocantins are expected to see better rains last half Jan. AgRural forecast bean production for 20/21 at 131.7 mmt.

Brazil's IMEA estimated Mato Grosso's 21/22 bean forward sales at 15.9% of the crop, up from 12.9% at the end of Dec., but well ahead of the 0.95% long term average at this point. 20/21 forward bean sales was 68.5% of the crop, which is 2% over the Dec. crop figure, but ahead of the 50.9% long term average at this point.

Brazil's IMEA estimated 20/21 Mato Grosso corn sales at 66.8% of the crop vs. 62.7% at the end of Dec., but ahead of the 45.4% long term average.

Russia's IKAR forecast Russia's 20/21 wheat exports at 37.5 mmt, down 1.0 mmt from the prior outlook.

China's National Grain Trade Center Monday reported 3.939 mmt of wheat sold at auction, which was 99.7% of the volume offered into the marketplace.

CALLS

Calls are as follows:

beans: 18-20 lower

meal: 5.80-6.00 lower

soyoil: 50-60 lower

corn: 1/2-1 lower

wheat: 6-9 higher

OUTSIDE MARKETS

Outside markets feature a weaker crude oil market which trades down to $51.87/barrel, and a weaker US dollar at 90.64. Stocks are up 199 pts.

TECH TALK

- March wheat prices place an inside day of trade from new contract highs of $6.93, and the main direction is now higher. Trendline resistance slants back towards $6.98/$7.05 should we go there. Major support now moves up to $6.50 from $6.30, and the top has yet to be hit.

- March corn prices back and fill towards major support at $5.22/$5.25, but all in all would price scale down into the gap at $5.15/$5.17. While prices do pull back, the chart does not show a corn top in place.

- March beans are trying to establish a trading range from contract highs at $14.36 by traveling back to $13.85. The market could still trade down to $13.70, and as long as prices do not close under here would have to view it as a buying opportunity. Funds appear to be liquidating on small rallies, however, which could keep bean prices pressured for the day in order to show us a trading range bottom.

- March soyoil falls to new lows at 41c, with 4080c as major lower trendline support. The rallies in soyoil now serve as a place in which funds can lighten up on length. Could cover a partial short in soyoil at 41c and keep the rest, as any trade under 4080c will find prices trending down to 40c without much of a problem.

- March meal enters into a fairly shallow correction, breaking to new lows at $451.60 with a good bounce higher. If needing to price something, the $445.00-$450.00 is a good place to do so, and suspect that even $450.00 may not be tested given the chart structure. Look for a $450.00-$470.00 trading range to likely form.

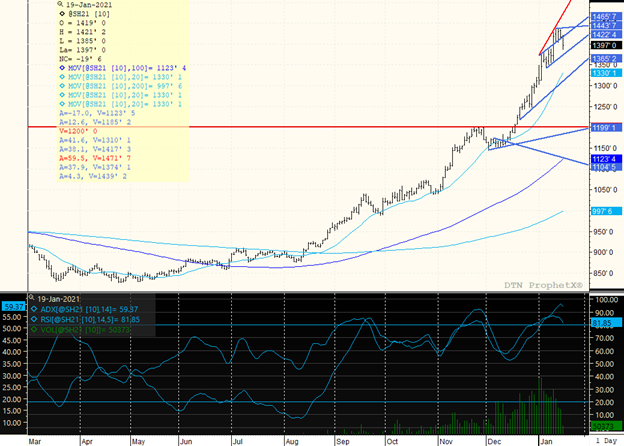

MARCH BEANS

The major direction is higher, but tops were beginning to form from $14.30-$14.35 which triggers a larger downward correction today. Lowest trendline support is located at $13.70, and would only be short if the market were to settle underneath. While the market is correcting, it has yet to enter into bear market territory. Look for a sideways trend to develop from $13.70-$14.35, and the ADX is still strong at 59, meaning one should price or cover a short on a further break. Could also look for a place to go long, though the fact that funds are not adding to their position is a bit troubling for the bull.

ON THE CALENDAR

Jan options expiration on Friday and cattle-on-feed.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...