GOOD MORNING,

Prices are generally lower this morning on neutral crop progress conditions and chart back-filling from recent highs. Oilshare continues to soften as traders buy meal/sell soyoil on better meal demand. Chinese meal prices closed higher as well as they continue to follow US strength. China's recovering swine and poultry sector suggests that meal demand could continue to rise for the balance of the year. For now, Chinese ports are saturated with recent purchases while crush is running ahead of last year's numbers. Brazil's depreciating currency resulted in farmers selling a record amount of beans to China in the first months of 2020.

WEATHER

- The 6/10 day outlook calls for isolated showers over the upcoming weekend with temperatures near to above normal next week. Showers continue in the Delta, which is maintaining adequate soil moisture. Weather maps are consistent with seven-day maps suggesting a few showers at best for the eastern areas, while the northern Corn Belt sees the better potential for rain showers. GFS ensemble suggests that from Friday - weekend ridge could break down and offer up the chance of better storms.

REPORTS

Commitment-of-Trader's report:

beans: net long 67,836

meal: net short 52,497

soyoil: net long 847

corn: net short 201,648

wheat: net short 38,812

Post report, corn bears covered in 77K contracts and are probably now short around 225K. The net long in beans is the most bullish in eight months.

Crop Progress:

Corn: 71% good/excellent, down 2% from week ago. Condition ratings fell the most in the eastern belt, which has been drier for longer. Michigan and Ohio were down 10% WOW, with Illinois down 6% and Indiana down 3%.

Beans: 71% good/excellent, unchanged from wk ago. Blooming: 31% vs. 17% week ago. Setting pods: 2%

Winter Wheat: 58% harvested vs. 42% year ago and 55% average

Spring Wheat: 70% good/excellent. 63% headed vs. 47% year ago and 68% average.

The crop progress report was about as expected with corn condition declines slightly positive for the market.

ANNOUNCEMENTS

The pandemic is poised to hit meat consumption globally, with per-capita consumption set to be 3% lower for 2020, and the lowest level since 2011, according to data from the United Nations.

France's wheat crop could be the smallest in a decade due to adverse weather. France's Ag Ministry pegged harvest at 31.3 mln tons in its first estimate of the 20/21 season, down 21% from a year ago.

Ukraine and Russia may speed up exports early for 20/21 as their governments plan to limit shipments later, as reported by AgroConsult. Russian wheat exports increased to 11.5 mmt for the first five months of 2020 from 9.5 mmt a year ago, as reported by official customs data.

DELIVERIES

Chicago wheat: 31

Meal: 2

Soyoil: 21

KC wheat: 18

BUSINESS

Egypt tenders for an unspecified amount of wheat for delivery from August 8 - 18. Early indications are that Russian prices are the most competitive.

CALLS

Calls are as follows:

beans: 3-5 lower

meal: .30-.70 lower

soyoil: 25-30 lower

corn: 4 1/2-5 1/2 lower

wheat: steady

OUTSIDE MARKETS

Feature a lower stock market which is trading off 200 pts, with a firmer US dollar at 97.60. Crude trades to a low of $39/barrel.

TECH TALK

- Charts are encountering back and fill from the recent highs. November beans are doing a typical walk-back to test $9.00, but the pullback is fairly shallow and therefore buyers will be on the hunt as weakness occurs. Path of least resistance is still higher, and good support moves up to $8.90 on a larger break. If short, would look to cover and go long should prices break down towards $8.85.

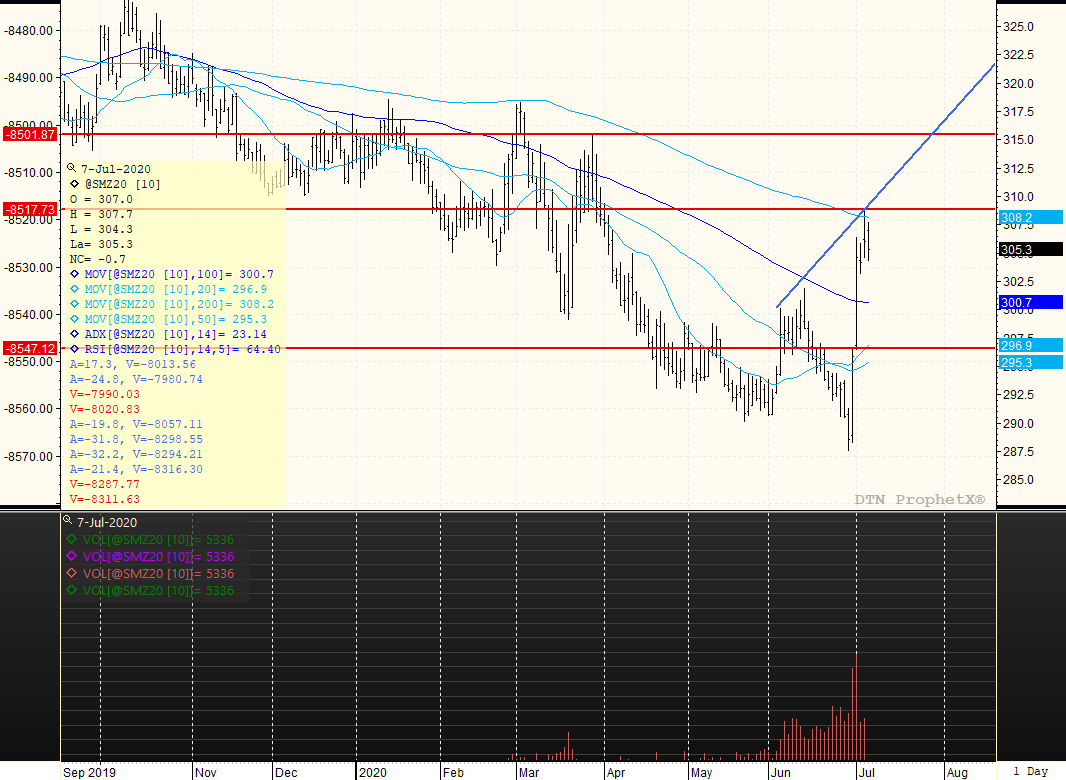

- December meal cannot get past its 200-day moving average of $308.00 with a small pullback towards $304.00. Look for better buying or short-covering to surface should prices decline to $299.00-$301.00 which was a previous top.

- December soyoil trades back under 29c but sits atop the 20, 50, and 200-day moving averages which are from 28c-2880c. Prices could still target 2950c as a period of consolidation takes place, but a break of 2880c suggests that a larger pullback may take place.

- December corn appears a bit more toppy as resistance builds anew from $3.57 to double highs at $3.63. Would look for further possible weakness down towards $3.48/$3.52, but this probably holds as charts suggest a new and higher $3.35-$3.65 trading range could come into play. The 100-day moving average in Dec. wheat was $3.52, and violating it suggests that more selling could be ahead.

- December wheat prices are stuck in the $4.95-$5.05 trading range, but prices continue to bump up against key resistance from $5.03/$5.08. Feels like wheat prices need a bit of breathing room with a rally to alleviate oversold extremes. A trade back over $5.08 allows prices to climb towards $5.15/$5.18.

DECEMBER MEAL

Overall trading range is higher from lower, with prices today caught between the 200 day moving average of $308.00 and the 100 day moving support average line of $300.70. Big picture trading range has lower support moving up from ctr lows of $287.50 to $295.00. Current trading range is now $295.00-$308.00 with the price advance. Prices could be in the first stages of placing a top, but if needing to price or cover a short would look to do so at $300.00-$301.00, as the rally may not be complete yet. Any trade over the 200-day moving average of $308.00 will trigger a move towards the peak high of $312.00-$315.00, as there is not much back resistance to stop an advance on the chart.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...