GOOD MORNING,

Prices continue to slip into trading ranges in front of the April 9 WASDE report. Sharply lower soyoil futures were the key to soy complex weakness yesterday, with one wire talking about a hedge fund selling out its soyoil length in front of Friday's report. Soyoil values are slightly firmer this morning for the May contract, with Egypt tendering. Beans are mixed, firmer in the PM session but a negative export sales number and new CONAB estimates creating more pressure heading into the close.

Grains are firmer taking over leadership on the board to the upside led by wheat. Wheat found some strength via short-covering activity, with KC in the lead. There are also a few more wheat tenders around from Algeria, Japan, and Taiwan. Corn prices continue firm with US domestic basis values stronger. The corn market remains well bid, indicating more aggressive consumer pricing before the report on Friday.

Brazil's CONAB released its estimates for current bean production, raising the crop estimates to 135.54 mmt vs. 135.13 mmt prev., and vs. 124.8 mmt for 19/20. Heavier than normal rains in some areas continue to cause problems with moisture in crops and concerns about quality. In Mato Grosso, the impact of rains on quality has resulted in some buyers getting discounts on purchases, according to the agency.

CONAB forecasts a record total corn crop of 109 mmt vs. its March forecast of 108.1 mmt, and vs.102.5 mmt in 19/20.

WEATHER

--The US 6/10-day forecast is for normal to below normal temperatures and normal rainfall. There are concerns about dryness in parts of the US western Corn Belt and Plains. More precip is noted for Illinois and Iowa, plus locally heavy amounts of rain for the Delta. The pattern has been for rains to continue in the upper Midwest, lighter rains in the central Belt allowing for crops to get in with a mix or rain and sunshine.

--In Brazil, net drying is expected in the center south and for some of the interior southern production areas over the next seven to 10-days. Argentina's conditions are still good for late maturing crops.

REPORTS

Export Sales:

beans: 20/21 net minus 92,500 mt and 21/22 net 338,600 mt (vs. an expected 100-600 kmt)

meal: 2021 net 127,700 mt and 21/22 net 4,800 mt (vs. an expected 100-300 kmt)

soyoil: 20/21 net 15,700 mt (vs. an expected 0-25 kmt)

wheat: 20/21 net 82,000 mt and 21/22 net 529,900 mt (vs an expected 150-700 kmt)

corn: 20/21 net 757,000 and 21/22 net 50,000 mt (vs. an expected .600-1.2 mmt)

Sales for 20/21 wheat and beans at marketing year lows. Gist of exports was negative.

Wheat: Sales were a marketing year low for 20/21, with increases primarily for South Korea, the Philippines, and Mexico. Reductions for China were reported of 56,700 mt. 20/22 sales were primarily for China for 260,000 mt.

Corn: Sales down 5% from the prev. week and 54% from the 4-week ave. Increases primarily for Japan and South Korea, and China for 99,000 mt, (with 70K switched from unknown).

Beans: Sales a marketing year low, down from prev, week and 4-wk ave. Increases for Egypt and Japan. A reduction of 216,100 mt for 20/21 was noted from China. 21/22 sales saw China in for 264,000 mt, but exports were a marketing year low.

Meal: Sales down 9% from prev. week and 36% from the 4-week ave. Increases noted for Mexico and Canada.

Soyoil: Sales up noticeably from prev. week and up 53% from the 4-week ave. Increases primarily for SK and the Dom. Rep.

ANNOUNCEMENTS

Russian wheat production for 21/22 was left at 78.6 mmt with improved rainfall boosting soil moisture levels to near average.

The United Nations Food Agency announced that world food prices rose for a 10th consecutive month in March, hitting its highest level since June 2014, led by jumps in veg oils, meat, and dairy.

The USDA will alter how it reports soyoil use by biofuel producers beginning with its May WASDE. The change comes amidst rising demand for veg oils from producers of renewable diesel, a clean burning fuel made from soy and other fats and oil.

CALLS

Calls are as follows:

Beans: 1-2 lower

meal: 80-1.00 lower

soyoil: mixed/higher

corn: 3-5 higher

wheat: 6-8 higher

OUTSIDE MARKETS

Crude oil prices struggling, trading down to $59.05/barrel, with the US dollar trading to 92.21. The Dow is down 15 pts.

TECH TALK

- May soyoil prices are congesting now from 52c-54c, using 53c as a pivot point. The market is moving sideways from 52c-54c, but also has very strong trendline support on a break to 5150c should we go there. Given the hard stop at 52c, think the market will continue to find strength and rally back towards 54c once again. Overall trading range appears to be from 52c-56c.

- May bean prices continue to test $14.00, staying above the 50-day moving average of $13.97. The price pattern has been to chop around from $14.00-$14.50, so nothing should change that for the moment. Should profit-taking result in a break of $13.97, a larger downside correction will begin again. But given the acreage numbers and reaction after for beans, think we stay well supported at $14.00 for further upside. Nov beans are busy basing from $12.65-$12.70, which is still relatively close to $12.85 contract highs. The market is still constructive for Nov beans, with $12.45 a buying opportunity if we go there.

- May corn puts on a very strong showing after losing most of its gains post report to fall to $5.50 from $5.85. However, prices are now well bid and moving over recent tops of $5.58. A nice line of support has formed at the lows after the report from $5.53-$5.55 and would look for prices to strengthen towards $5.70 as the session continues.

- May wheat now forms a "v" bottom which is creating both support and short-covering activity. Very strong resistance is located at $6.32 which is where the 100-day moving average as well as major trendline resistance meet. On a strong showing would look to give it a test, with any trade above suggesting that we test $6.40/$6.45 next.

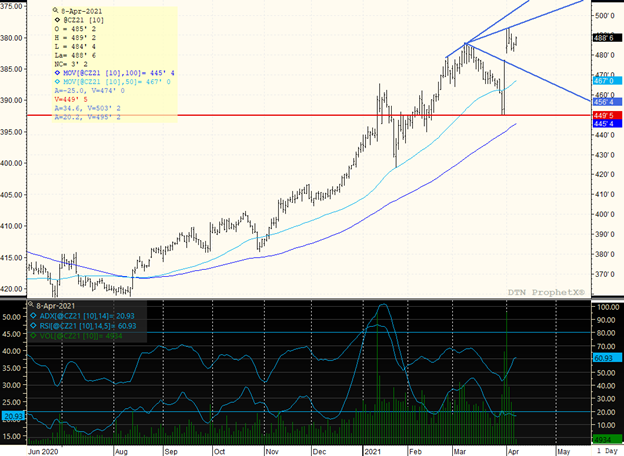

DECEMBER CORN

The mission of the market is to determine value levels of trade given the jump to new ctr highs of $4.93 1/2 from the pullback towards the open gap which is from $4.77 1/2 up to $4.80 3/4. The trend is weak overall as the market posts peak highs near $5.00 but cannot hold the rally. Best support under the market would be $4.75/$4.77, which is gap closure. When prices spike such as this one did, the gap remains open for several weeks after. Even if we fall into the gap, would use that opportunity as a chance to cover a short, own, or price as the major direction is still higher, and the presence of a new ctr high suggests that the top is not yet established. Think we are headed for a $4.75-$5.00 trading range or higher.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Large supplies and a strong dollar took their toll this week on corn and soybeans, but they still managed to outperform. Weather worries pushed wheat higher for a seventh straight session, and pork finally took a fall. There was high volume trading in corn today but without any strong fee...

Large supplies and a strong dollar took their toll this week on corn and soybeans, but they still managed to outperform. Weather worries pushed wheat higher for a seventh straight session, and pork finally took a fall. There was high volume trading in corn today but without any strong fee...

The Market Brazil has been winning the soybean export war, and imported biodiesel feedstock threatens domestic crush margins, but Chicago trading this week appeared to shake off such concerns. July soybeans traded lower for the past three trading sessions but larger gains achieved at the beginn...

The Market Brazil has been winning the soybean export war, and imported biodiesel feedstock threatens domestic crush margins, but Chicago trading this week appeared to shake off such concerns. July soybeans traded lower for the past three trading sessions but larger gains achieved at the beginn...

The Q1 2024 GDP was 1.6 percent, well below the pre-report consensus expectation of 2.4 percent, and down from 3.1 percent in Q1 2023 and 3.4 percent in Q4 2023. That rate was the slowest in almost two years, dating back to Q2 2022. Recall that in the 2 February Ag Perspectives report on...

The Q1 2024 GDP was 1.6 percent, well below the pre-report consensus expectation of 2.4 percent, and down from 3.1 percent in Q1 2023 and 3.4 percent in Q4 2023. That rate was the slowest in almost two years, dating back to Q2 2022. Recall that in the 2 February Ag Perspectives report on...