GOOD MORNING,

Prices were on the defensive with the market unable to ignore 3% better ratings on Monday for corn and beans. The majority of corn is now pollinating under mostly favorable circumstances. Beans will be made in August. The answer to larger crops is demand, and traders will be on the hunt for Chinese wheat, bean, or corn business. China continues to purchase large breaks, and we will see if the pattern continues. China may need to increase corn into their country as domestic stocks tighten. Soyoil is higher following firmer crude oil palm, returning a bid to oilshare.

IN news stories, officials at Argentina's grain and crush export chamber of commerce said there have been 14 confirmed Covid-19 cases at two different port operations.

WEATHER

Rains will concentrate on lower Midwest and parts of the Hard Red Winter wheat country. From this point forward there should be some net drying activity. Parts of Iowa still have parts of dryness that will remain a concern. Overall weather remains neutral to bearish

ANNOUNCEMENTS

Rabobank is forecasting Brazil 20/21 bean acres in Brazil at 38.0 mln hectares, up nearly 3%, and forecasting 20/21 production at a record volume of 127.3 mmt. If production is realized it would be 5.3% larger than the previous record season.

Brazil's ANEC estimated its July 2020 bean exports at 8.4 mmt, down 400,000 mt from the prev. outlook. The group lowered their July 2020 corn exports to 5.4 mmt from 5.65 mmt prev.

Egypt and China became the major importers of Ukrainian grain for the 19/20 season with a combined volume of 13.3 mmt. Egypt imported 7.1 mmt of Ukraine grain while China imported 6.2 mmt. Ukraine exported 56.5 mmt of grain for the 2019/20 season.

Russia's SovEcon reduced its forecast for Russia's 2020 wheat crop to 79.3 mmt from 79.7 mmt due to worsening conditions for spring wheat.

CALLS

Calls are as follows:

beans: 3-5 lower

meal: 2.00-2.40 lower

soyoil: 5-10 higher

corn: 1 1/2-2 lower

wheat: 3 1/2-4 1/2 higher

OUTSIDE MARKETS

Rising crude at $41.56/barrel, a firmer US dollar at 93.39, firmer gold at $1953.20/oz, and stocks up 39 pts.

TECH TALK

- December soyoil traded down to what was a previous gap level at 2960c, which was key lower support and market stabilization. Prices may want to go down and test this level once more, but if short or want to get long it is a good place to buy something. Dec. soyoil firms from this level to trade back over 30c.

- December meal prices remain a $290.00-$308.00 trade, and the trade back under key support at $297.00 opens the door for a test of $294.00.

- November beans return to test $8.83/$8.85 and some traders could be looking for an opportunity to own the market down at these levels. The ability to hold on to lows shows chart stabilization for beans.

- Dec. corn continues to sit on its lows with support from $3.27-$3.30. Resistance moves down to $3.33/$3.34 for Dec. corn, and further lows could be placed. Corn ended on a weak note, so expect to see more follow-through lower.

- Sep. wheat futures consolidate values from $5.20-$5.25, though its appearance is rather toppy should prices trade back under $5.19. Because of the vertical advance from $4.95-$5.19, there is not much to stop a trade lower should prices break below $5.19.

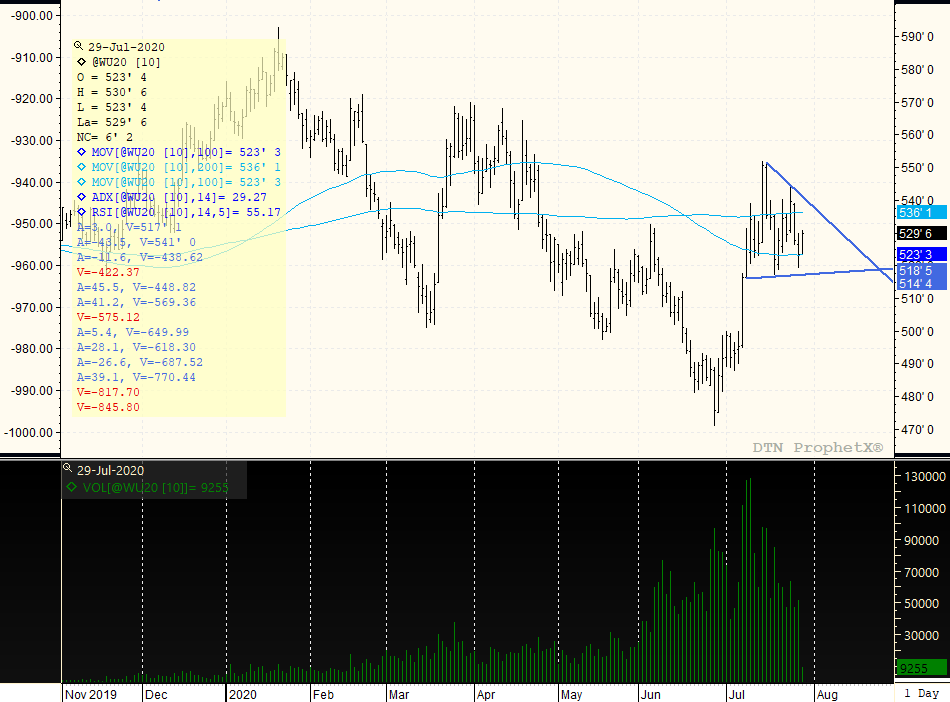

SEPTEMBER WHEAT

Prices are back and forth from $5.20-$5.51 1/2 using $5.35 as a pivot level. Prices continue to operate in the upper portion of a trading range where lows of $4.71 were placed in late June. Therefore, any break under $5.19 opens the door for trade back towards $5.00-$5.08. Trendline resistance returns again to the $5.36-$5.40 area. The 200-day moving average is $5.36, and trendline resistance, as noted by the upper blue line, crosses at $5.41. The up-trend still remains strong with an ADX of 29, but has been weakening a bit.

ON THE CALENDAR

EIA report is out today, with expectations that production could bounce back 3-4% WOW with a slight stocks build.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

The CBOT was mostly higher to end a mostly bearish week with wheat leading the way on several mildly bullish developments. Wheat futures saw price-supportive development in the IGC’s lower 2024/25 global ending stocks forecast, dryness in the U.S. Southern Plains, and smaller Russian 2024...

The CBOT was mostly higher to end a mostly bearish week with wheat leading the way on several mildly bullish developments. Wheat futures saw price-supportive development in the IGC’s lower 2024/25 global ending stocks forecast, dryness in the U.S. Southern Plains, and smaller Russian 2024...

USDA released the monthly Cattle on Feed report today. Total inventory, placements and marketings all came in lower than the pre-report estimates, though total inventory was at the same volume or higher than last year for the seventh consecutive month. Placements came in well below the average...

USDA released the monthly Cattle on Feed report today. Total inventory, placements and marketings all came in lower than the pre-report estimates, though total inventory was at the same volume or higher than last year for the seventh consecutive month. Placements came in well below the average...