GOOD MORNING,

Prices were stronger with beans rallying higher as more rumors of Chinese business hit the wires. The outlook for China's bean and corn imports continues to be friendly for prices, particularly since China's production outlook was lowered due to multiple typhoons impacting corn. Tender business remains very active for wheat. Funds continue to buy market pullbacks on continued signs of good demand. Higher crude, falling NOPA stocks to a nine-year low, and firm world oil values continues to support soyoil futures and oilshare.

Harvest results are gradually coming in and more results will circulate as it proceeds. With a harvest weekend on the way, it could portend more of a two-sided trade for some of the more over-bought markets after the open.

WEATHER

--Heavy rains from hurricane Sally stay over the southeast, as it weakens to a depression from a hurricane. For harvest, weather in the states over the next 10 days looks good in the Midwest.

--NE China crop areas are very wet and flooded with more rains in the forecast, which is leading to a reduction in crop estimates. SA, EU, and Black Sea remain too dry causing stress to current crops and future seedings. Night frosts expected in central, northern and eastern Ukraine could present more trouble for winter grain sowing for the 2021 harvest.

REPORTS

Export Sales

Beans: 20/21 net 2.457 (vs. an expected 1.5-2.7 mt)

Meal: 19/20 minus 105,400 mt and 20/21 net 197,300 mt (vs. an expected 200-550 mt)

Soyoil: 19/20 net 100 (vs. an expected 0-35 mt)

Corn: 19.20 net 1.609 and 20/21 (vs. an expected 800-2.0 mt)

Wheat: 20/21 net 335,700 mt and 20/22 net 300 mt (vs. an expected 350-700 mt)

Good sales for corn and beans, low-end for products and wheat.

Wheat: Moderate sales but Russia and Black Sea continue to garner the bulk of demand. More tender business this week could support values on a break. China is absent.

Corn: Good sales as expected. China is in for 360K and unknown at 360K. Good sales are expected next week.

Beans: Big numbers were expected and hit. China accounts for 1.488 MMT and unknown for 500K., with 264K switched from unknown to China.

Meal: Poor sales with world demand slowing down.

Soyoil: Low-end, with more buying going to palm as China purchases ahead of a holiday

ANNOUNCEMENTS

Brazil ag consultancies forecast 20/21 bean field expansion in the northern and northeastern regions to expand by more than 6%, which is the fastest rate in 4 years, expecting around 865,000 hectares to be added.

China set Sep 18th as a date to auction 20,000 mt of frozen pork from state stockpiles. The gov. has sold over 550,000 mt of frozen pork from state reserves so far this year.

China's National Development Reform Commission stated that the 2021 tariff rate quotas for corn, rice, and wheat would remain unchanged for 20/21. The 2021 corn quotas will stay at 7.2 mmt, with 60% taken off by state run firms. Wheat quotas will remain at 9.64 mmt, with 90% taken off by state run firms.

Strategie Grains forecasts a small European wheat surplus of 1.5 mmt. They forecast EU-28 20/21 wheat production at 1.2 mmt.

CALLS

Calls are as follows:

beans: 2-4 lower

meal: 1.30-1.60 lower

soyoil: 5-8 lower

corn: 2-2 1/2 lower

wheat: 1/2-1 lower

What to look for today? New highs were placed, but prices will open lower, a slight difference from other bull market days, and could elicit more profit-taking.

OUTSIDE MARKETS

A weaker energy picture, with crude trading down to $39.42/barrel from $40.39/barrel highs, and the US dollar higher at 93.14. Stocks are down 300 pts.

TECH TALK

- November beans posted an outside day closing higher Wed. with a bounce back from a break to $9.85 to place a new contract high at $10.18 1/4, the highest price since June 2018. The strong upward bounce sent a signal that prices were going to test previous highs, as weaker markets do not have the capabilities of bouncing. New highs beget new highs, and though the market remains overbought at 82%, (anything over 70% is overbought), could see another run at the highs.

- December soyoil pulled back to test 3390c, the top of the congestion pennant which also held, leading to a new high price of 3519c. The ADX has strengthened to 50, the strongest trend reading on the board. Look for a pullback towards 3450c to offer up first support values, and there is currently not a sell signal.

- December meal charts also remain sideways / higher, but currently sets a double top at $328.00. The uptrend remains firm, so would look for a re-test of these highs at some point. Dec meal trendline support moves up to $318.00.

- Dec corn trades past $3.70, negating but does hit a target high at $3.73. If long would be cautious at this point, as $3.61 is the next best support on a solid break.

- Dec. wheat charts continue to set up good support at $5.37/$5.38, with congestion trade around the previous support level of $5.42. Key resistance is $5.45/$5.48, and could be a seller against this level with a tight buy-stop for a larger break down towards $5.25/$5.30.

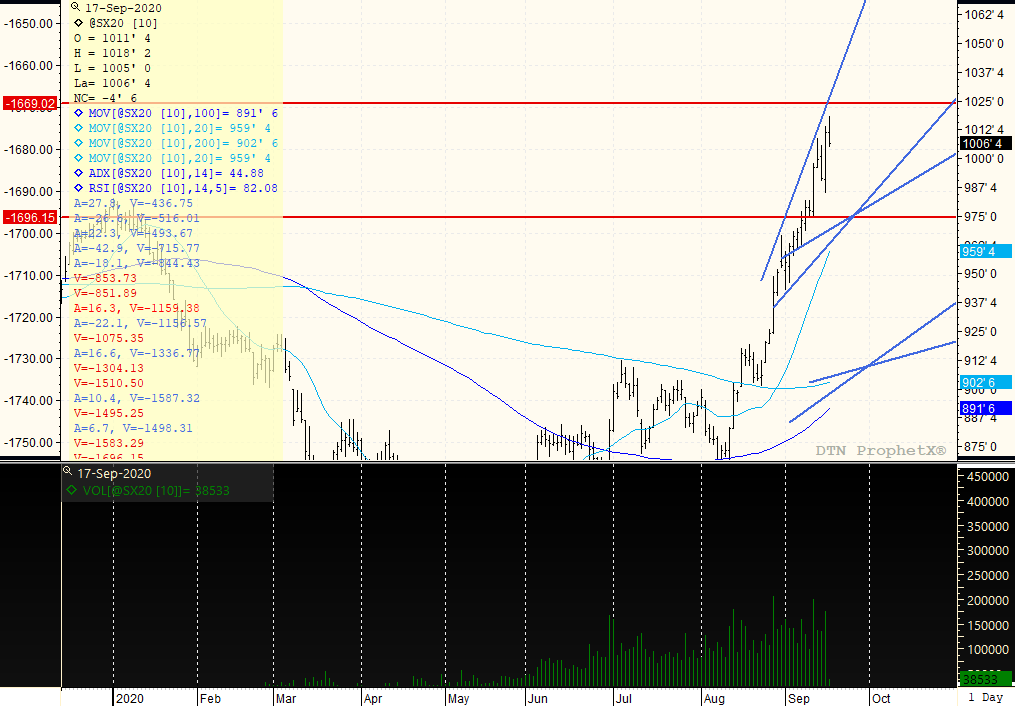

NOVEMBER BEANS

The bull market continues with new ctr highs at $10.18 1/4. Prices will open around the first congestion level from $10.05-$10.07, with a break below $10.00 now turning charts a bit sideways from higher. There is a note of caution this morning, as the new high in place will be met with a lower open. Additionally, the high of the night at $10.18 1/4 comes close to the upper blue trendline resistance. Therefore, if long would probably take a profit on something should prices make another run into the $10.18/$10.20 target area. For now, would consider the trading range notched up to $9.80 to possible highs of $10.20. Without a chart break-down, possible highs above $10.20 could also still take place with an extreme target high of $10.35.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

The bearishness continues as South America crops loom and Northern Hemisphere weather is stable. The impending flood of Argentine soymeal and soyoil onto the market sent the May soyoil contract to a new low. There was nothing in today’s weekly USDA Export Sales report to alter the...

The bearishness continues as South America crops loom and Northern Hemisphere weather is stable. The impending flood of Argentine soymeal and soyoil onto the market sent the May soyoil contract to a new low. There was nothing in today’s weekly USDA Export Sales report to alter the...

Transatlantic GI’ing Consumers Politicians on both sides of the Atlantic protest big business and their sacrilegious capitalism. Yet sometimes it is government screwing the consumer to boost private profits. Parmigiano Reggiano was a prized and premium priced cheese before obtaining the E...

Transatlantic GI’ing Consumers Politicians on both sides of the Atlantic protest big business and their sacrilegious capitalism. Yet sometimes it is government screwing the consumer to boost private profits. Parmigiano Reggiano was a prized and premium priced cheese before obtaining the E...