GOOD MORNING,

Prices are mixed this morning, lower for everything but soyoil. Soyoil futures followed a strong performance by palm, which jumped to new contract highs, and firmer crude oil which trades closer to the $80/barrel mark. Oilshare is soaring, as Egypt comes to tender for some as well. Beans made new lows in the night session but are recovering slowly following the palm. Grains remain in congestion mode. China markets are closed for holiday.

The October USDA will be important in that yields will become more exact. In front of that report come the guesses. StoneX raised its corn yield to 176.7 bpa from 177.5 bpa prev. report, with production at 15.022 bln bu from 14.998 bln bu. They also raised the bean yield to 51.3 bpa vs. 50.8 bpa prev. with production at 4.436 bln bu vs. 4.409 bln bu prev.

Macros were negative yesterday as stocks went slipping into the red when it was announced the trading of China's Evergrande stock was suspended.

Rhetoric from the USTR will state how China is not living up to the trade agreements. Traders are waiting to see how China will respond to the USTR statement with hopes that they will resume buying in terms of the Phase one deal. Beans are being punished the most in its affiliations with all things China. Having waited eight months for US Trade Rep. Katherine Tai's promised "to-to-bottom" policy review with China, some US industries and experts were complaining of the lack of timing or specifics.

Export inspections yesterday were good for corn, and the reported chunk to Mexico yesterday from the USDA finds prices and charts holding up well. For the week ending 9/30, US exporters shipped the highest total since before Hurricane Ida disrupted Gulf operations., which included 141K mt to China. Export inspections for beans found that one month into the marketing year, shipments have reached 1.831 mmt vs. 7.088 mmt year ago.

WEATHER

--Sporadic rains across the Midwest are delaying fieldwork. The 6–10-day weather maps give way to better progress again which will heave harvest on a strong stride towards completion. There is a chance for showers in the HRW areas next week.

--Rains in Argentina and Brazil are constructive for crop development.

REPORTS

Crop Progress:

beans: 34% harvested as of Oct. 3 vs. 26% average and 16% week ago. Dropping leaves: 86% vs. 75% week ago. Good to excellent: 58%. States furthest ahead are Ill., Iowa, and the Dakotas.

corn: 29% harvested vs. 24% year ago and 22% average. Mature: 88% vs. 85% year ago and 77% average. Good to excellent: 59%

winter wheat: 47% planted vs. 50% year ago, and 46% average. Emerged: 19% vs. 22% year ago, and 20% average.

ANNOUNCEMENTS

Brazil's Safras y Mercado forecast 21/22 bean planting at 4% vs.1.5% week ago. Brazil's IMEA said Mato Grosso, (Brazil's largest bean producing state), is at 37.4 mmt, unchanged from their Sep. forecast.

Iran is forecast to triple its wheat imports for 21/22 marketing year ahead, and could import up to 8 mmt after hot and dry weather conditions in the region, while at least half of the needed volume has already been covered, according to AgriCensus.

CALLS

Calls are as follows:

beans: 1-3 lower

meal: 2.00-2.50 lower

soyoil: 60-80 pts higher

corn: 3 1/2-4 lower

wheat: 8-10 lower

OUTSIDE MARKETS

Crude oil trading to new highs over $78/barrel, after OPEC+ decided to stick to a gradual output increase plan rather than fully opening the taps. Stocks are up 150 pts with the US dollar trading to 94.04.

TECH TALK

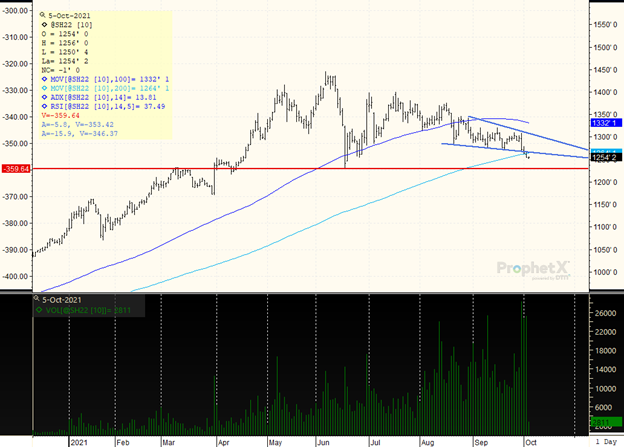

- December meal futures trades to new lows overnight, below $325.00, and on target to hit $320.00. These are the lowest levels since Oct 2020. The downtrend is strengthening with an ADX at 25, and prices are now verging on oversold at 31%. The break-down below the congestion phase from $335.00-$345.00 now becomes resistance, although it seems as though we are now a long way from it. There is no reversal signal yet, so could stay patient if needing to price.

- November bean prices also slipped to new lows at $12.31, with oversold status not quite as much as meal at 36% RSI. The new lows have yet to be met with a reversal signal, and now the target low is $12.15-$12.20. Rallies may continue to be selling opportunities as there is not a good reversal signal off the low.

- December soyoil remains the bull market, forming a line of good support from 5750c to 58, and finally on target to likely achieve its target high of 60c, the 100-day moving average. Prices over 5980c will do the trick, and think we go there despite a weak ADX at 15, one which could likely also find 60c holding as a market top.

- December corn has not left its Sep 30 trading range which was $5.27 on the downside, and $5.48 on the up. Prices are in the middle of this zone, and working within an ascending triangle, which is a friendly formation. Trading to the downside of $5.30 would drop prices out of the uptrend, however, turning into a wider trading range from $5.15-$5.45. If needing to price, the behavior of the corn market has been rather resilient, and any move over trendline resistance and the 100-day moving average of $5.49 would be extremely friendly, targeting $5.60.

- December wheat back and fills after achieving a new high for the move up yesterday at $7.63 1/2. Would look for pullbacks to see support, and there is plenty of air between recent highs and key support at $7.35. If short, would probably use the $7.35 middle of the range to make an exit, as this chart is still fairly friendly, if not a bit overdone to the upside.

MARCH BEANS

Path of least resistance is lower with an ADX at 13, which is a very weak trend, and heading into slightly oversold conditions at 37%. The market had been in sideways congestion from $12.75-$13.09, but broke to recent lows under key support at $12.70 to trade to new lows today at $12.50 1/2. The target low is now at the June low of $12.29/$12.30. By the time we get there, we could be into oversold status. Until then, prices can continue to slowly leak lower, with small rallies probably being sold by funds, or those long given weakish market structure. For the day, the $12.50 benchmark appears to be tested, and has to hold in order to begin to form a low.

TAGS – Feed Grains, North America

Most of the major agricultural commodity contracts opened today’s trading session in the red and stayed that way to the close. Only feeder cattle and lean hogs managed small gains on the day. New contract lows were hit for December soyoil, September SRW and September HRW. Volume was overa...

Most of the major agricultural commodity contracts opened today’s trading session in the red and stayed that way to the close. Only feeder cattle and lean hogs managed small gains on the day. New contract lows were hit for December soyoil, September SRW and September HRW. Volume was overa...

Non-Meat: In a first, a Europe-based company has sought EU approval to market lab-grown meat, in this case fake foie gras. Some member states have already banned such products. While lab-grown meat remains expensive, and plant-based meat substitutes have faced declining popularity, the increase...

Non-Meat: In a first, a Europe-based company has sought EU approval to market lab-grown meat, in this case fake foie gras. Some member states have already banned such products. While lab-grown meat remains expensive, and plant-based meat substitutes have faced declining popularity, the increase...

June 2024 total red meat and poultry stocks were up slightly from May but 5.4 percent below June 2023 levels due to sharp declines in poultry and pork stocks. Total poultry stocks were down 7.8 percent year-over-year (YoY) due to reductions in broiler slaughter for the month. Total pork stocks...

June 2024 total red meat and poultry stocks were up slightly from May but 5.4 percent below June 2023 levels due to sharp declines in poultry and pork stocks. Total poultry stocks were down 7.8 percent year-over-year (YoY) due to reductions in broiler slaughter for the month. Total pork stocks...