GOOD MORNING,

The surprising strength of the rallies this week caught bears off guard, creating a short-covering rally which found little selling pressure. Corn was the strongest market but makes sense since it was the most beaten-up heading into the Sep. report. Basis remains strong. The hurricane, which triggered fund selling and liquidation, perhaps got the market to a point where it:

1) had to come up for air and

2) created an undervalued condition for corn, in particular, given the amount of fund selling into the Sep. 10 data.

Near the close, wheat and soyoil encountered losses that took the other markets off their highs.

As technicals took over Wednesday, the market was able to shrug off bean cancellations and a bearish NOPA report for soyoil stocks. The NOPA report was net positive for beans. Any weakness yesterday in the bean market was taken as a buying opportunity. In the actions-speak-louder-than-words category, the ability to come back from negative trade speaks to technical strength, and interest in buying the market. Today we continue to see upside follow-through.

Other positives now being factored into the market is more chatter about yields coming in as less than expected, with some disease issues via the dry end to the season. Ideas are circulating that perhaps the USDA will have to dial down yields next month. As for business, the delays in the Gulf have forced China to purchase more expensive Brazilian beans, but their supplies may be getting low and they still need to cover their needs into the fall and winter.

As harvest proceeds, there is also more talk that corn yields are less than expected, with the talk of a dry end to the season perhaps resulting in a drop in the final yield. Illinois fields have triggered the most conversation about disease and weak stalks.

WEATHER

--Warm and mostly dry over the next 10 days across the US with limited rains in areas. Rains are ongoing in the south.

--There are still La Nina concerns and discussions concerning growing conditions in South America. Russia could use more rain.

REPORTS

Export Sales:

beans: 21/22 net 1.26 mmt and 22/23 net 2,000 (vs. an expected .600-1.5 mmt)

meal: 20/21 net 95,400 mt and 21/22 net 42,400 mt (vs. an expected 75-400 kmt)

soyoil: 20/21 minus 1,700 and 21/22 net 6,100 (vs. an expected minus 20k to plus 20k)

corn: 21/22 net 246,600 mt and 22/23 net 2,300 mt (vs. vs. an expected .500-1.0 mmt)

wheat: 21/22 net 617,100 mt (vs. an expected 300-700 kmt)

Export sales were good for wheat and beans but low end for all else.

Wheat: Good sales due to strong demand for feed and high quality wheat, with tighter supplies moving forward.

Corn: Sales were poor, probably due to the Gulf. US is competitive, but so are Ukraine and SA.

Beans: Good sales with daily announcements from China, but the Gulf situation impacted export capability. Brazil took the lion's share of biz.

Soyoil: Sales remain low end. Rising world premiums makes soyoil expensive.

Meal: Sales were just moderate but better demand should be felt moving forward. The US is competitive.

ANNOUNCEMENTS

Russia's Ag ministry data shows as of Sep 15, all grains harvested at 99.4 mmt, which includes 70.8 mmt of wheat and 17.5 mmt of barley.

Argentina's BA Exchange estimated production for 21/22 corn at 55.0 mmt vs. USDA at 53 mmt, and beans at 44 mmt vs USDA at 52 mmt.

Chinese buyers have agreed to relax a key quality specification for upcoming shipments of French wheat in response to rain damage in France's harvest. Chinese importers will now accept readings of 75 kgs, (165 lb), per hectoliter, compared with 77 kg minimum initially required for import deals.

CALLS

Calls are as follows:

beans: 2-4 higher

meal: 2.20-2.30 higher

soyoil: 50-60 lower

corn: 1/2-1 higher

wheat: 3-5 lower

OUTSIDE MARKETS

Firmer with crude oil trading up to $72.66/barrel. The US dollar trades higher to 92.79 with stocks down 35 pts.

TECH TALK

- November beans see positive price action, as the pullbacks have been very shallow evidencing there is buying interest in this market. Values are over $13.00, and the market now most likely moves into resistance from $13.05 / $13.10. The turn higher from lower is also over sideways congestion which was from $12.80 -$12.95, and now becomes a base of support. Trade over $13.06 finds very little resistance to stop a further advance towards $13.35, previous trading range tops, but we have to get there.

- December meal direction is sideways, and the market is trading from $335.00 up to $350.00. For the day expect that $340.00 is now a support level from which the market can rally from. The chart features a likely congestion trade from $340.00 to $350.00.

- December soyoil trading range works higher as well, and the chart direction higher suggests that this market is looking to test the 100-day moving average at 5980c, having defined 55c as an interim low. Pullbacks in this market are buying opportunities.

- December corn prices turned higher from lower, taking out most resistance levels which were located at $5.25 to $5.28, sparking a rally towards $5.40. Interim resistance is $5.45, and with pullbacks shallow and the market well bid think we go there. Top of the trading range and very good resistance is $5.55.

- December wheat is also back over $7.10 after trading down to $6.77. Trading range is now from $6.80-$7.22/$7.55, but may move higher than this if buying takes us back over the key resistance zone which led to the break. For the day, wheat is struggling against $7.17-$7.20 resistance.

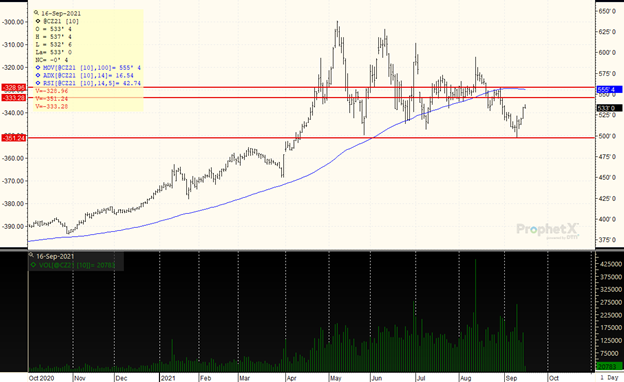

DECEMBER CORN

The reversal from the blow-off low last Friday was confirmed yesterday as the outside day closing higher now sees a rally above the highs of $5.30. The ADX is gaining a bit of strength, and open interest rose yesterday for the first time as prices traded upward signaling new longs are probably in the market. The target high is now $5.45, which was the peak leading to the low under $5.00. The market is not yet overbought, and Wednesday's price action goes a long way to confirming a bottom. Look for good support to move higher to $5.15, and $5.45 appears do-able. The market would move higher again if it traded over $5.45, with the 100-day moving average and peak high coinciding at $5.55, which is likely the top of this market for now should we go that high. We could be in the process of moving into a $5.20-$5.55 trading range.

TAGS – Feed Grains, North America

Large supplies and a strong dollar took their toll this week on corn and soybeans, but they still managed to outperform. Weather worries pushed wheat higher for a seventh straight session, and pork finally took a fall. There was high volume trading in corn today but without any strong fee...

Large supplies and a strong dollar took their toll this week on corn and soybeans, but they still managed to outperform. Weather worries pushed wheat higher for a seventh straight session, and pork finally took a fall. There was high volume trading in corn today but without any strong fee...

The Market Brazil has been winning the soybean export war, and imported biodiesel feedstock threatens domestic crush margins, but Chicago trading this week appeared to shake off such concerns. July soybeans traded lower for the past three trading sessions but larger gains achieved at the beginn...

The Market Brazil has been winning the soybean export war, and imported biodiesel feedstock threatens domestic crush margins, but Chicago trading this week appeared to shake off such concerns. July soybeans traded lower for the past three trading sessions but larger gains achieved at the beginn...

The Q1 2024 GDP was 1.6 percent, well below the pre-report consensus expectation of 2.4 percent, and down from 3.1 percent in Q1 2023 and 3.4 percent in Q4 2023. That rate was the slowest in almost two years, dating back to Q2 2022. Recall that in the 2 February Ag Perspectives report on...

The Q1 2024 GDP was 1.6 percent, well below the pre-report consensus expectation of 2.4 percent, and down from 3.1 percent in Q1 2023 and 3.4 percent in Q4 2023. That rate was the slowest in almost two years, dating back to Q2 2022. Recall that in the 2 February Ag Perspectives report on...