GOOD MORNING,

Prices are mostly lower as the July 10 WASDE is ready to open with a new set of new numbers for market digestion. Weather remains hot and dry, though a few rounds of rainfall fell across parts of the Midwest. After Friday the forecast turns hot and dry again. For this week, sporadic rainfall is resulting in a small market setback from recent highs.

Corn prices continue to work a bit lower though there continues to be talk of China in the market. On the negative side, corn faces competition from Ukraine as well as South America. Spreads are firming with some interior locations looking for nearby supplies of corn. Bean spreads tighten as well as more chatter about business occurs.

Wheat is starting to gain on corn on technical considerations as prices rally out of recent lows. French production cuts and more wheat tenders in general created a bit of a short-covering rally by already short funds. Ukraine and Russia also reduced their wheat harvests. Look for further signs that wheat may accelerate out of harvest lows.

WEATHER

- The 6/10-day maps lean warm and dry, except for the Northern Plains, but the 8/14 day outlook offers a better return to a normal weather pattern. There have been isolated scattered showers across much of the Corn Belt, with temperatures near to above normal heading into the weekend. Showers continue in the Delta which is maintaining adequate moisture levels for now. Bottom line is that adequate soil moisture is still noted for much of the Midwest which should foster growth, though areas in the east are direr and in need of more moisture.

ANNOUNCEMENTS

Brazil's CONAB raised its estimate of bean production for the 19/20 growing season to a record 120.9 mmt, vs. 120.4 mmt in June, and vs. 115.03 mmt for 18/19.

Brazil's CONAB forecast it would produce 100.6 mmt of corn vs. 100.4 mmt in 18/19, but down from the June forecast of 101.0 mmt. The safrinha crop was cut to 73.9 mmt from 74.2 mmt.

Brazil's ANEC increased July bean exports to 8.0 mmt vs. 7.25 mmt wk ago, with year-to-date total exports at 69.57 mmt. July corn exports are forecast at 5.16 mmt vs. 3.9 mmt week ago, with year-to - date total exports at 7.7 mmt.

France's AgriMer's first forecast for 20/21 soft wheat shipments outside the EU are forecast to fall to 7.75 mmt, down 43% from 19/20 which is the lowest volume in 4 years.

Russia's IKAR downgraded its estimate for the Russian 2020 grain crop by 2 mmt to 126 mmt due to low yields in part of the country's southern and central regions. Its forecast for Russia's 2020 wheat crop was cut by 1.5 mln tonnes to 78 mln tonnes.

DELIVERIES

Chicago wheat: 82

CALLS

Calls are as follows:

beans: 2-4 lower

meal: 1.20 - 1.80 lower

soyoil: 5-9 lower

corn: 1 1/2-2 lower

wheat: 2 -2 1/2 higher

OUTSIDE MARKETS

Outside markets include firmer stocks, up 48 pts, along with higher crude at $40.76/barrel. The US dollar falls to 96.80.

TECH TALK

- Dec. soyoil futures direction is higher, closing a March Covid gap at 2964c. Target high is 30c but the close was rather anemic. Eventually price direction appears ready to target 30c-3025c. All moving averages under the Dec. soyoil market remained intact to support this market as the day moved along yesterday.

- Dec. meal prices back and fill after hitting the 200-day moving average at $308.00. Dec. meal pulls back to what could be the lower adjusted end of the trading range at $300.00-$301.00. If pricing or covering a short, the low end close suggests that the $295.00 level could be hit before prices stabilize again.

- November beans walk prices back to test key support under the $9.00 level of trade, which is typical once beans have breached a major benchmark. The capabilities still are intact for beans to target $9.13 again for a possible higher target of $9.20. Nov. bean trading range could be a newly adjusted $8.80-$9.20 level, but the close back below $9.00 suggests that further weakness could be in store. A drop to $8.85 is probably a good short-covering or buying opportunity.

- December corn prices pullback to test the previous resistance levels of $3.45-$3.48 in place for so long, now turned support. On a first return lower support typically holds, and would look for this to be the case. If needing to price, the $3.35/$3.40 level offers a better opportunity should we go there.

- Sep. wheat futures are consolidating under $5.00 again, and any trade over $5.00 will trigger fund short-covering. If that is the case, there is not much back resistance to stop an advance towards the 50 day moving average of $5.09. The chart pattern forming is more friendly than bearish, as explained below.

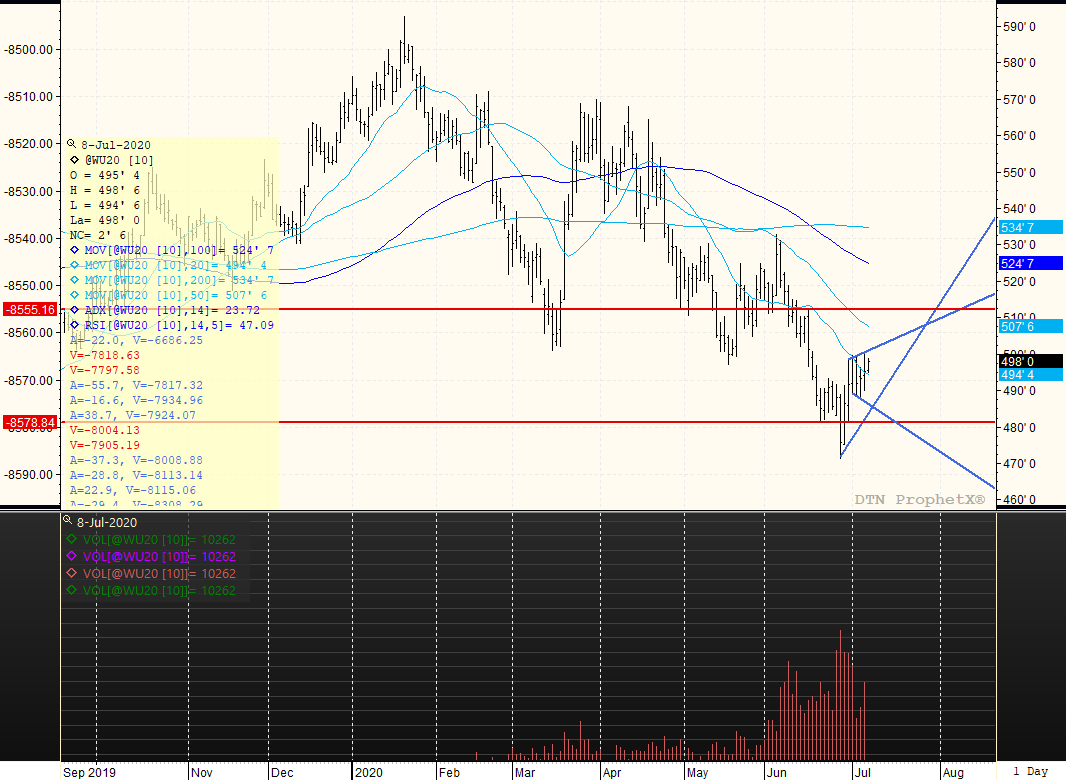

SEPTEMBER WHEAT

The cycle direction lower resulted in a blow-off low of $4.71, with multiple lows providing better support at $4.81. The chart pattern is becoming more constructive as prices appear to work into an ascending triangle, which is friendly for price direction, (as opposed to a descending triangle which is bearish). If the market were to break, trendline support now moves up to $4.85, and any move above $5.00 suggests that prices will find a trip to the upper red line which crosses at $5.12, top of the possible $4.80-$5.12 trading range. The triangle suggests strongly that further strength could arrive for a $4.80-$5.12/$5.15 trading range. Could also straddle/strangle this same range.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...