GOOD MORNING,

Report day! At 11:00 central time traders will see how the new carry-out levels and SA production estimates impact prices. Funds seemed to be onto something yesterday, with corn prices accelerating from the start of the day. As mentioned before, fund buying would probably not be countered with much selling, as farmers are now busy planting. Dec corn is making new contract highs this morning, as May trades back to the level attained on March 31 towards $5.85. Beans continue to waffle on either side of even, caught between lower soyoil today vs. firmer meal trade.

Wheat and corn rallied on rumors that China is around the market for both. China could be looking to buy US wheat, as they have been selling large amounts from their state reserves as a substitute for higher priced corn. According to China's National Grain Trade Center, between Jan and March China sold 26.06 mmt of wheat in gov. auctions, which is 12 percent more than the quantity sold in 2020. Wheat rallied as concerns remained over global weather, with dryness continuing in the US Northern Plains, and dry and cold conditions in western Europe tempering optimism over the wheat harvest. Corn rallied on continued dry conditions in Brazil.

US corn basis continues to move higher, and bean processors continue to bid for beans. Corn demand may have to be adjusted, if not in this report, certainly the May one. Export data for corn was extremely friendly, with net sales now at 66.4 mmt. Corn also derived support from US ethanol producers who are preparing for the peak summer driving season, as Americans return to the road as more vaccines are distributed. This could be a recovery year for the much depleted vacation industry. EIA ethanol stocks were at the lowest level since November, as reported yesterday.

The April WASDE is out at 11:00 central time. As a reminder, here are general advertised expectations for 20/21 carry-out:

beans: 118 mln bu (more ideas are lower)

corn: 1,379 mln bu (more ideas are lower)

wheat: 846 mln bu

STORIES

Argentina's farmers are once again hanging on to their beans as an asset against exposure to the country's depreciating peso currency, even as Brazil and US farmer selling is accelerated. This has been a common practice in Argentina for years, but comes as Argentina needs more export revenue to get out of a deep recession, and as uncertainty continues ahead of congressional elections. Farmers fear that the gov. may once again raise export taxes. The lack of selling is net positive for beans when prices rally.

There are escalating tensions on Ukraine's eastern border with Russia as the latter increases its forces near the border. So far, the friction has not affected grain exports and prices but it is being monitored closely.

WEATHER

--Weather remains extremely dry in the Northern Plains which is supporting Minn. wheat. Dryness in the Plains and the western Corn Belt remains a problem. Long term forecasts suggest that the western Corn Belt may be too dry heading into the key summer growth time, while the eastern Corn Belt remains okay. There are currently more rains over the Midwest and Delta that could delay the planting pace a bit.

The EU remains too dry as well, also supportive for wheat. Brazil remains dry, and Argentina is too wet, slowing harvest and lowering the quality of bean crops.

ANNOUNCEMENTS

Argentina's BA Exchange forecasts bean production at 43 mmt vs. 44 mmt prev. They estimated that 3.5% of the soy crop has been harvested.

China's Ag Ministry increased its 20/21 marketing year corn import forecast to 22.0 mmt, more than twice the volume they estimated last month at 10 mmt. USDA projection for 20/21 corn imports is 24.0 mmt.

Russia's SovEcon forecasts the 2021 wheat crop at 80.7 mmt.

CALLS

Calls are as follows:

beans: mixed

meal: 2.20-2.50 higher

soyoil: 25-30 lower

corn: 2 1/2-3 1/2 higher

wheat: 4-6 higher

OUTSIDE MARKETS

A slightly weaker crude oil market, trading down to $59.13/barrel, and a firmer US dollar at 92.23.

TECH TALK

- There are plenty of bullish tech signals to entice the bulls out there, from bull flags to ascending triangles. Prices for May beans continue to walk back to test $14.00, which is not unusual at this point, but does point to a large sideways stuck pattern. Would continue to own, price, or cover a short on a break towards the 50-day moving average which is located from $13.95 - $14.00. The price action is building in a bit more resistance which could create a break towards the 50-day moving average of $13.95. If short and we go there, would probably get something covered.

- May meal prices are basing again at slightly higher levels, from $405.00-$408.00. Look for this market to likely head back over the key resistance level of $411.00 for trade back towards $420.00.

- May soyoil is 52c-54c, pivoting around 53c. Would still prefer to own good breaks in this market, which includes any pullback to key support at 5175c-52c.

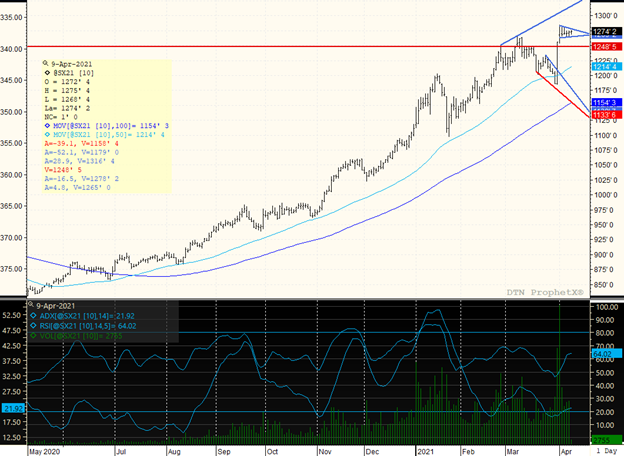

- Dec corn gap remains open, albeit it is small, and we are starting a new leg higher over trendline resistance. New contract highs have been posted in Dec. corn due to the open gap and the primary direction is up. May corn trades back towards the prev. contract high at $5.85 and shows more technical strength by going there. Trendline resistance is still close by at $5.88/$5.90 but looks like we go there into the report.

- May wheat takes out major trendline resistance and the 100-day moving average which takes prices sideways from lower. Next stop is $6.40/$6.45 as the chart features a "v" bottom, with a move higher over the 100-day moving average of $6.32, which is likely where we begin the trading session.

NOVEMBER BEANS

The market continues to trade in a congestive price pattern, still possibly forming a bull - flag. The vertical two-day price rise remains constructive, and typically the price congestion after a vertical upside break-out can last up to 1-2 weeks. This technical bullish action keeps bears away and bulls still interested. The ADX is still weak, however, which is why the market seems to be stalling out after reaching new ctr highs at $12.85. If prices can accelerate to the upside of $12.65/$12.70, would look for the ADX to strengthen and for prices to target $13.00-$13.20. Regardless, unless November beans break and settle back under $12.45, the path of least resistance remains higher. Look for a $12.45-$12.85 or higher trading range based on current technical price action.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...