GOOD MORNING,

The adage is that low prices cure low prices. But now it's also enough to say that a few tweets and headlines along with some positive technical signals will aid in price recovery as well. Trump's tweets had been hinting at some kind of resolution, but this time the markets heeded what was said with China echoing that they would also play the negotiation game. Bears were caught at fresh lows in grains, which fueled yesterday's turn-around. Media outlets continue to say that US negotiators have reached terms of the phase one deal and await the President's sign-off. China continues to a verbal agreement to purchase $50 bln of farm products in 2020, which would exceed the record amount of $26 bln in 2012. The US now awaits for Beijing to sign off on the deal.

Good export sales provided the fundamental catalyst to drive bears out of their comfort zone. Soyoil futures continue to trade upward, isolated from all the other markets as the bullish trade continues. Growing biofuel demand with reduced production in palm oil continues to drive oilshare higher, as African Swine fever reduces the need to crush (reduced herds) which has depleted oil stocks. The uncertainty about Argentine's tax policy under the new administration is encouraging buyers to extend forward coverage as well.

WEATHER

US weather remains cool and dry. The focus remains on Argentina's weather, with dry and hot weather depleting soil moisture, increasing stress on developing bean and corn crops, and slowing planting. This weekend does have a chance for better rainfall events.

Funds are net short corn, beans, and meal, long a modest amount of wheat and heavy longs in soyoil. Issues for these markets are:

Beans: Were probably undervalued on a technical overshoot to the downside for funds. Still, China has to buy and Argentina remain dry to justify much higher values. If a deal is signed off on, bean values could continue to trend higher.

Wheat: World ending stocks are ample but US stocks were lower. Can now add that the USMCA deal could trigger more wheat buying (not to mention China on a trade deal). Argentine wheat crops are lower and they supply Brazil. Last year, Brazil imported 7 mmt of wheat and of that, 6 mmt was supplied by Argentina. Australia is out of the export picture as well.

Corn: Saw one of the largest weeks of export sales, with Mexico taking a chunk. Whether a drought is the catalyst in Mexico or USMCA, makes no difference. Higher exports will stabilize this market on its lows, but it still remains one of the slowest export paces since 2012.

Soyoil: Tight world supplies continue on the back of lower palm oil production. Slower crush for meal draws down soyoil stocks. Look for pullbacks to continue, and technically this market has the best upside and follow-through, though currently is heading towards overbought levels.

ANNOUNCEMENTS

Brazil's oilseed group ABOIVE estimated that Brazil will export an additional 3 mmt of beans next year, forecast it to reach 75 mmt in 2020.

Russia is searching for a new way to restrict grain exports.

The Rosario Grain Exchange said they are requesting the crush company Vicentin to provide the amount of debt with suppliers for unpaid grain, and to make a concrete offer to its creditors.

BA Exchange pegs bean plantings now at 61.3% of the 17.7 mln acres projected, which was up 12% on the week but is less than the 68.8% year ago. Lack of rainfall has delayed some plantings.

DELIVERIES

Meal: 196

Soyoil: 104

Corn: 44

CALLS

Calls are as follows:

beans: 10-14 higher

meal: 2.80-3.50 higher

soyoil: 30-35 higher

corn: 4 1/2-6 higher

wheat: 1-3 higher

OUTSIDE MARKETS

Outside markets feature firmer values as stocks and commodities rally. Crude trades up to $59.60/barrel while the US dollar falls to 96.71, the lowest level since last July. The British Pound is rallying against the dollar with the Tory victory in the U.K. election. Stocks are up 65 pts.

TECH TALK

- Many friendly chart patterns have been triggered this week, from bull flags (soyoil) to an outside day closing higher (wheat). This morning, small gaps are now present for March beans ($9.16-$9.18 12) and March corn (3.80 1/4 to $3.80 1/2) as prices pull away to the upside. Since they are small in nature, they are not break-away or measurement gaps, but will serve as key support on a setback and if left unfilled, becomes more bullish.

- March beans trade to new highs, which establishes $9.00 as a floor, with highs yet to be determined. What is true is that the up-move is now strengthening the ADX, suggesting pullbacks will become buying opportunities, and prices are over key moving averages from $9.18-$9.22.

- March meal prices also get a boost after testing key support close to $295.00, but languish at the bottom of a trading range.

- March soyoil is the bull, trading to new highs at 3305c after a 2 day vertical advance followed by a bull flag, with a target overhead high of 3330c.

- March corn battles back from a new trading range low close to $3.70 with a small gap-higher trade in the night session and prices bumping up against major trading range highs of $3.85.

- March wheat prices posted an outside day higher on Thursday with extension gains as well, with prices testing the key resistance level of $5.35.

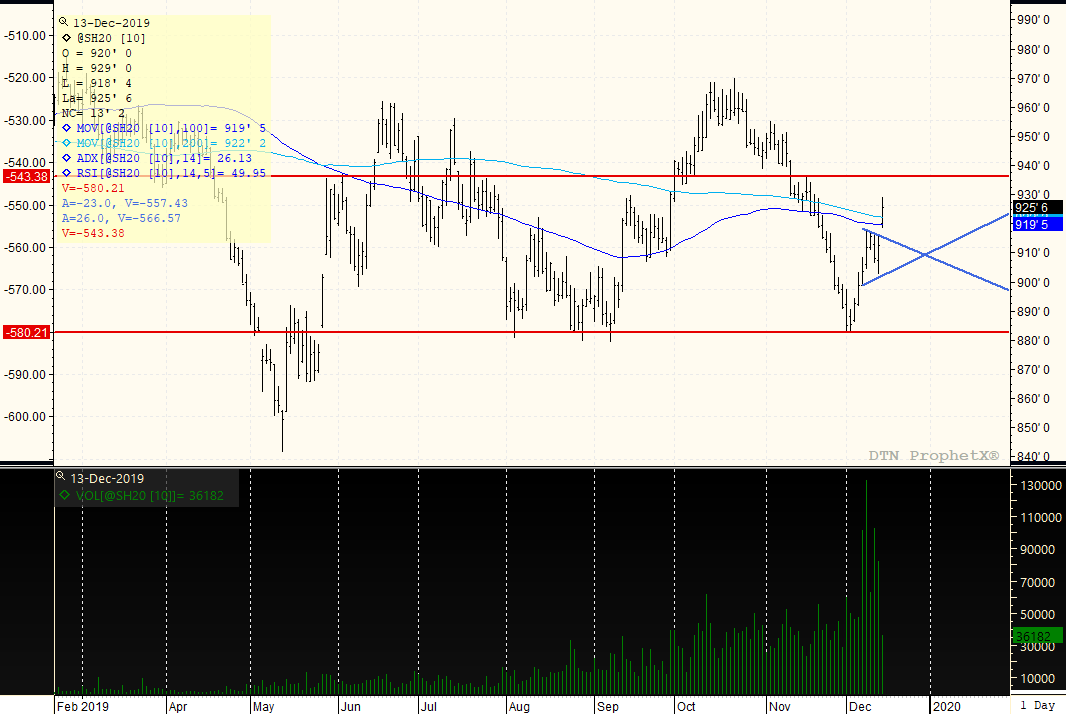

MARCH BEANS

Prices elevate to higher levels with a night session gap from $9.16 to $9.18 1/2. Prices take out moving averages located at $9.19 (100 day) and 200 day ($9.22) which extends the trading range to the upside. Trade will begin by staying over the 200 day moving average of $9.22 which strongly suggests that the market challenges $9.29 for test of $9.35/$9.40, and a $9.00-$9.35/$9.40 trading range. If prices remain above the 200-day moving average without gap closure, will promote more short-covering.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Corn, soybeans and soyoil all closed lower after trading up the previous three sessions. July soymeal made it a fourth trading session higher, and wheat remains on a tear with a fifth trading session closing higher. The mood around wheat sees supply concerns developing in North America and in t...

Corn, soybeans and soyoil all closed lower after trading up the previous three sessions. July soymeal made it a fourth trading session higher, and wheat remains on a tear with a fifth trading session closing higher. The mood around wheat sees supply concerns developing in North America and in t...

Cow-calf producer margins are discussed less frequently in these pages than their downstream counterparts of feedlot and beef packer margins, but this doesn’t mean they are less important to understanding the beef industry’s current state and outlook. Additionally, discussion of thi...

Cow-calf producer margins are discussed less frequently in these pages than their downstream counterparts of feedlot and beef packer margins, but this doesn’t mean they are less important to understanding the beef industry’s current state and outlook. Additionally, discussion of thi...

Reigniting a Transatlantic Deal Former Italian prime minister Enrico Letta is something of a policy rock star after authoring a report on the future strategy for the EU. Most of the 146-page report focuses on strengthening the EU’s internal Single Market but, buried at the end of th...

Reigniting a Transatlantic Deal Former Italian prime minister Enrico Letta is something of a policy rock star after authoring a report on the future strategy for the EU. Most of the 146-page report focuses on strengthening the EU’s internal Single Market but, buried at the end of th...