GOOD MORNING,

Report day today, to be released at 11:00 central time. Expectations include reduced corn and bean yields, reduced production, reduced corn exports, higher wheat exports.

Prices are higher this morning after reversing course from Monday's lows. Higher values are attributed to short-covering after President Trump said he would postpone Oct. 1 tariff increases for a few weeks. Officials are reporting that Chinese importers have been asking about prices for US beans and pork, but no solid sales confirmations to report yet. In the meantime, a spokesperson for the Commerce Ministry said he hopes both sides create favorable conditions for more October trade talks. The markets are all higher in general in what appears to be a broad day of macro across-the-board buying, except for crude oil.

WEATHER

Getting interesting.....perhaps not in the US, but certainly in South America. Mid-September is the time that bean planting picks up in Brazil but it has been dry, causing producers to push back their planting times in Mato Grosso and Parana, the two largest bean producing states. Australia remains in a drought cycle with wheat production officially lowered to below 20 mmt to 19.1 mmt vs. the 26 mmt average.

As to the US, the short-term forecast remains favorable but by the last part of September a freeze may cross parts of Canada. While that is not unusual, any frost it brings to maturing bean crops in the Dakotas/Minnesota will be a problem.

STORIES

Sources from the White House say the administration is recommending biofuel producers accept a deal that would raise blending mandates next year by 5 percent. It is less than they asked for and they have until Friday to make their decision.

ANNOUNCEMENTS

China's Ag Ministry estimated 2019/20 corn production at 255.51 mmt, up 0.82 percent from month ago.

China's Ag Ministry estimated 2018/19 corn consumption at 174 mmt, off 2.0 mmt from month ago on lower pig and sow herds.

China's Ag Ministry estimated 2019/20 bean imports at 84.0 mmt, down from 84.9 mmt, off 1.06 percent from month ago.

China's Ag Ministry estimated 2019/20 bean production at 17.23 mmt vs. 17.27 mmt month ago.

Argentina's Rosario Grain Exchange est. bean harvest at 50.0 mmt, with corn harvest at 50.0 mmt, vs. 51 mmt month ago.

Russia's SovEcon estimated the 2019 wheat crop at 118.2 mmt, up 1.4 mmt from month ago. The wheat crop was 74.9 mmt, up 0.5 mmt from prev.

DELIVERIES

beans: 408

soyoil: 45

meal: 54

Chicago wheat: 1

KC wheat: 3

September contracts expire at noon tomorrow.

CALLS

Calls today are as follows:

beans: 6-8 higher

meal: 1.50-1.90 higher

soyoil: 15-18 higher

corn: 1/2-1 higher

wheat: 1/2-1 higher

If one market moves lower, it is likely to be wheat.

Outside markets feature higher equities markets, up 50 pts on month based on optimistic trade rhetoric. The bullish trend continues for the US dollar, with prices now at 98.93. Crude oil breaks to $54.64/barrel.

BUSINESS

Taiwan is in for 110,000 mt of US wheat.

Export sales this morning were generally better than expected except for corn. Mexico purchased the majority of US beans. Ukraine and SA still fill the majority of world corn needs. Meal sales were neutral to low end, with competition from Argentina.

TECH TALK

- Major direction is sideways/lower, but the markets are starting a consolidation phase into the report and have all rallied close to key resistance levels, which is Dec corn at $3.63, Nov beans at $8.80, Dec soyoil at 2911c, Dec wheat at double highs at $4.83 1/2, and Dec meal at $299.00. Expect to find buy-stops over these highs. The seasonal prices for corn and wheat are higher for the last half of September. Reaction to the report will be key. Funds are net short across the board, and may take a bearish report to cover in some of those positions in front of the South American growing season.

- Nov bean charts features a sideways trade with bears unable to break the $8.50 level with downside follow-through. Two top ranges exist, with the first at $8.82, and beyond that $8.95.

- Nov beans begin higher against trendline resistance close to $8.77, and therefore trade over $8.80 suggests we could eventually test $8.95.

- Dec soyoil charts are more constructive looking with trade back over 29c, suggesting a re-test of 2920c-2930c.

- Dec meal remains amazingly resilient, falling towards new lows at $292.00, only to continue to recover nicely. If following the pattern, could price on breaks towards $291.00, should we get there, while any trade that is over the major down-trend channel would be significant and suggest prices could rally back towards $305.00/$310.00 again.

- Dec wheat prices are in a $4.50 - $4.85 trading range, and running into key resistance at $4.83/$4.86. The chart pattern is congesting after the run-up with any trade past $4.83 1/2 opening the door to moving up towards the 100-day moving average at $4.98. If short and we trade past $4.86, would be prepared for such a rally to take place.

- Dec corn prices are up against major resistance at $3.63. In the big picture, the market has not traveled very far from contract lows at $3.52 1/2. However, we could be in the early process of forming a base, with a trade over $3.63 buyable for a rally towards $3.70. Sellers may be waiting at this point in Dec corn as the major trend is lower and the downtrend is strong with an ADX reading at 32.

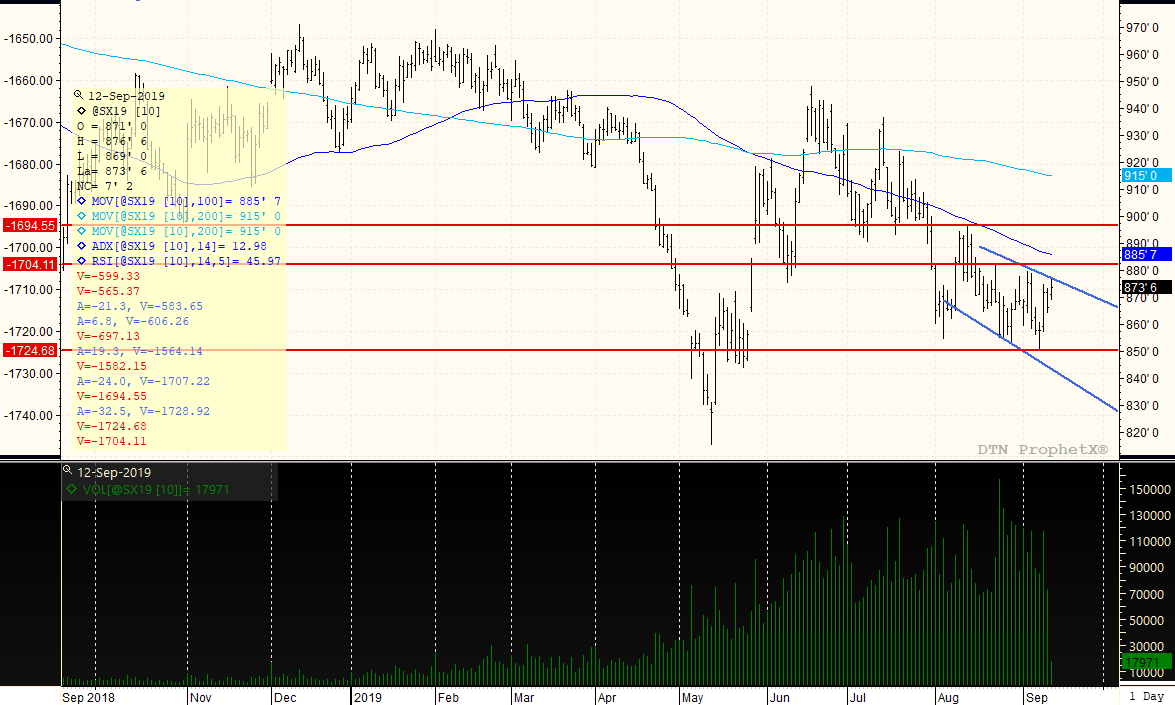

NOVEMBER BEANS

Overall trading range is from an established $8.50 up to $8.82/$8.85, and the major direction is sideways. The ADX trend is extremely low at 12 (anything under 25 is lack of trend), and therefore prices have little follow-through at the top or bottom. The bottom target under $8.50 to $8.40 was never achieved as price action posted a new low without follow-through.

On the top end, $8.77 to $8.82 is one layer of resistance, while trade over that takes us back towards the 100-day moving average of $8.85. Could continue to straddle or strangle from $8.50-$8.85 with buyers not interested until we trade above $8.82. For the day would prefer to own breaks, and if the report is bearish, will be interesting to see if funds want to cover in a partial position on a break of size.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...