GOOD MORNING,

Prices are mostly lower this morning as the markets rallied high enough to draw some profit-taking from the bull as the week draws to a close. Funds who are short may adopt a wait and see attitude, particularly as far as the Chinese shopping list goes. As corn and beans neared new highs for recent ranges there were more reports of hedging interest and cash sales in beans over the last several weeks. Beans have been gaining on corn, as they are apt to do in the month of December, but today the spread has turned a bit as profit-taking in beans sends prices lower. The new bean/corn ratio hit new highs at 2.42, a situation that typically reverses as the calendar turns over from Dec 19 to Jan 20. Soyoil is holding vs. meal for another surge in oilshare.

WEATHER

Still mostly neutral, though dry spots are starting to worsen slightly in Brazil. Hot and dry weather continues in Rio Grande do Sul, depleting soil moisture. Increasing showers and storms across Brazil's northeast will ease stress on beans and improve conditions there. Moderate to heavy showers in the dry areas of Argentina's BA eased stress on corn and beans in that region. Weather remains neutral.

REPORTS

In terms of reports, there was a monthly condition report for winter wheat released Thursday, with only three states seeing improvement, those being North and South Dakota, as well as Nebraska.

The grain crushing report was as follows:

Crushings: 174.6 mln bu vs. 187.1 mln bu in Oct, and 178.10 mln bu yr ago. Oil stocks increased by 59 mln lbs to 1.879 bln, well over the expected 25 mln lb increase. Meal stocks increased from 335 tmt to 426 tmt.

Ethanol crush down-ticked and is nearing the bottom end of the range from the second half of 2019.

Export sales:

Beans: 19/20 net 330,300 tmt and 20/21 net 1,700 tmt (vs. an expected 350-1.0 low end)

Meal: 19/20 net 94,700 tmt and 20/21 net 1,500 tmt (vs. an expected 75-250 low end)

Soyoil: 19/20 net minus 1,900 tmt (vs. an expected 5-30 poor)

Corn: 19/20 net 531,400 tmt and 20/21 net 8,600 tmt (vs. an expected 30-775 neutral )

Wheat: 19/20 net 312,900 tmt and 20/21 net 20,400 tmt (vs. an expected 250-600 low end)

Sales were expected to be light and did not disappoint. Bean sales hit a marketing year low, down 66% from the prior 4-week average, and below the low end of expectations. Purchases by China totaled 160,200 mt. Meal sales have limited demand, with soyoil sales surprisingly bad. Mexico again accounted for much of the corn sales, with wheat sales low end. Wheat sales may increase moving forward due to rising world premiums and a Phase 1 deal.

ANNOUNCEMENTS

Argentina's reporting agency BAGE forecasted its wheat progress at 92% complete, with overall production forecast at 18.5 mmt.

Argentina's BA Exchange estimated beans planted at 84.3%, with corn at 83.5% complete. Recent rainfall has been beneficial for both crops.

The new Japan/US deal is now on board for the new year, and the USMCA should be ratified shortly.

Brazil corn exports in 2019 were large, shipping 4.368 mmt of corn in Dec vs. 4.288 in Nov, and 3.637 mmt year ago.

DELIVERIES

beans: 275

soyoil: 349

meal: 1503

CALLS

Calls are as follows:

beans: 6-8 lower

meal: 2.20-2.60 lower

soyoil: 10-15 lower

corn: 1 1/2-2 lower

wheat: 4 1/2-6 lower

OUTSIDE MARKETS

Outside markets show a risk-off day of profit-taking with the Dow off 226 pts. Energies, on the other hand, are stronger with crude trading up to new highs at $64.09/barrel, and the US dollar on firmer footing at 97.10.

TECH TALK

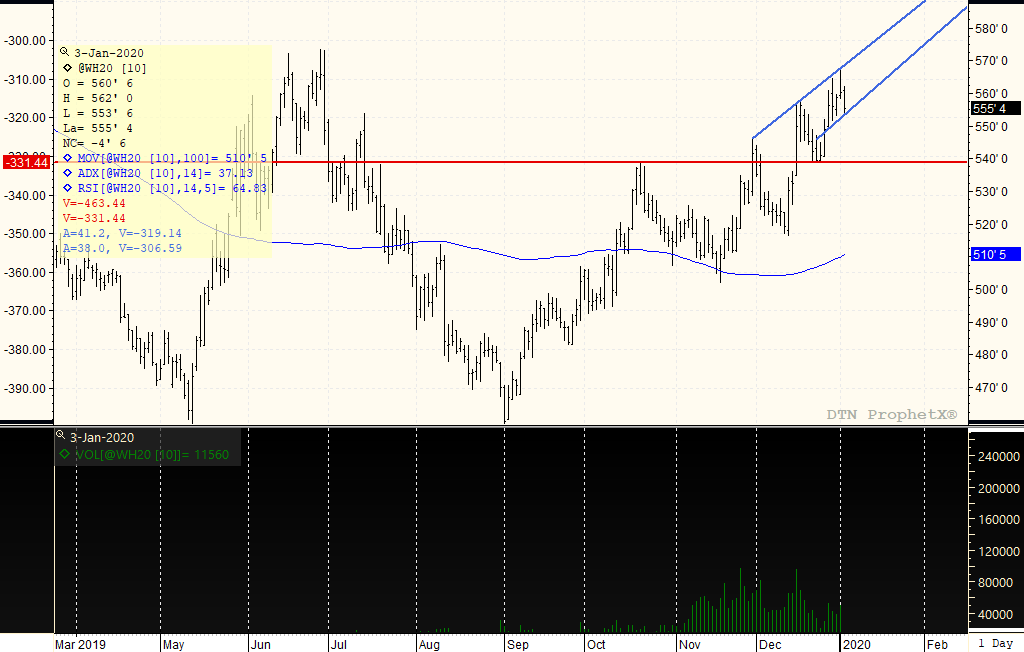

- The markets were due some back and fill but that begs the question as to whether this the start of a larger correction. For now, the pullbacks are not enough to say that is so.

- March wheat would now trigger sell-stops and break important support, should it take out $5.51.

- March corn prices trade sideways and if one market were to head higher first, it would be this one. Prices are sideways to higher for March corn, with trendline resistance still located at $3.91.

- March beans trade back towards key support at $9.45, technically a key first support level that so far appears to offer the chance of holding.

- March meal sells back into key support from $300.00-$302.00, a level that must be broken in order to leg lower.

- March soyoil back and fills towards 35c, with key support at 3440c.

If these key support levels are violated, would look for larger pullbacks:

March beans: $9.40

March meal: $300.00

March soyoil: 3440c

March wheat: $5.50

March corn: $3.85

MARCH WHEAT

Prices rallied to new highs this week at $5.67 1/2 before retreating. The lower end of the trading range, however, is located at $5.40, and for the morning it appears that the chart will start on minor trendline support. Starting on support often suggests that a larger pullback will be coming, confirmed with a break at $5.50. If long, would think about taking something off the table, as wheat prices appeared "tired" yesterday, spending the majority of the day at the lower end of its trading range. If wanting to strangle or straddle the range, $5.25-$5.65 would be reasonable, though there is still a chance for an eventual test of the recent highs as well.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

The bearishness continues as South America crops loom and Northern Hemisphere weather is stable. The impending flood of Argentine soymeal and soyoil onto the market sent the May soyoil contract to a new low. There was nothing in today’s weekly USDA Export Sales report to alter the...

The bearishness continues as South America crops loom and Northern Hemisphere weather is stable. The impending flood of Argentine soymeal and soyoil onto the market sent the May soyoil contract to a new low. There was nothing in today’s weekly USDA Export Sales report to alter the...

Transatlantic GI’ing Consumers Politicians on both sides of the Atlantic protest big business and their sacrilegious capitalism. Yet sometimes it is government screwing the consumer to boost private profits. Parmigiano Reggiano was a prized and premium priced cheese before obtaining the E...

Transatlantic GI’ing Consumers Politicians on both sides of the Atlantic protest big business and their sacrilegious capitalism. Yet sometimes it is government screwing the consumer to boost private profits. Parmigiano Reggiano was a prized and premium priced cheese before obtaining the E...