GOOD MORNING,

Equities celebrated the signing of the Phase One deal, but beans were not impressed. A bearish NOPA soyoil stocks number sent soyoil prices tumbling, more or less confirming that the top posted a week ago was indeed a possible market high. This AM, prices will begin the day lower across the board as more soyoil bulls liquidate and wheat bulls take profits.

Here are some of the salient points of the agreement:

China will purchase no less than $12.5 bln above the 2017 baseline of $24 bln in year one - net total of $36.5 bln

China will buy no less than $19.5 bln above the 2017 baseline of $24 bln in yr 2 - net total $43.5 bln

The troubling statement throwing cold water on the market was China's Vice Premier Liu's statement that market principles would guide commodity purchases.

Though equities were able to muster a good performance from the signing, beans started to show cracks even before the signing, and further disappointment as the details were released as big purchases do not seem imminent. Specific amounts of each commodity were not broken out in detail.

Seasonally, beans have a hard time staying higher this time of the year as more SA crop production begins to hit the market. Technically, the violation of key support at $9.33 March beans became a sell signal. Funds also sold corn yesterday, and now hold a 100K short.

WEATHER

Large storm is crossing the Midwest bringing another round of ice and snow to the eastern/western Cornbelt. South American weather continues to have drying tendencies, but for now its on track to produce record large crops.

REPORTS

Export sales:

Beans: 2019/20 net 711,500 mt (vs. an expected 400-700 kmt)

Meal: 2019/20 net 375,200 mt (vs. an expected 75-250 kmt)

Soyoil: 2019/20 net 36,200 mt (vs. an expected 0-25 kmt)

Corn: 2019/20 net 784,800 mt and 20/21 net 207,000 mt (vs. an expected 500-700 kmt)

Wheat: 2019/20 net 650,000 mt and 20/21 59,700 mt (vs. an expected 300-500 kmt)

Export sales were generally better than expected and brought a bit of price stability as prices sit on their morning lows.

USDA broiler hatchery data showed 4% YOY growth in eggs set and broilers.

ANNOUNCEMENTS

Strategie Grains expected 19/20 MY EU soft wheat exports, excluding durum, at 30.5 mmt, up 1.8 mmt vs. Dec. They noted the EU is taking the slack of lower exports from Australia, the US, and Russian.

Capital Economics said that global wheat prices may fall by 20% in 2020 as stronger supply and weaker demand growth pushes the market into surplus. It is forecasting sluggish global demand growth of just 2.1% this season as African swine fever has reduced China's demand, and even if China buys more wheat from the US, total imports are unlikely to increase.

DELIVERIES

Soyoil: 15

CALLS

Calls today are as follows:

beans: 4-6 lower

meal: .40-.80 lower

soyoil: 20-25 lower

corn: 4 1/2-5 lower

wheat: 6-8 lower

OUTSIDE MARKETS

Outside markets features weaker crude, trading down to $57.56 /barrel, and a weaker US dollar at 97.08. The Dow is up 66 pts.

TECH TALK

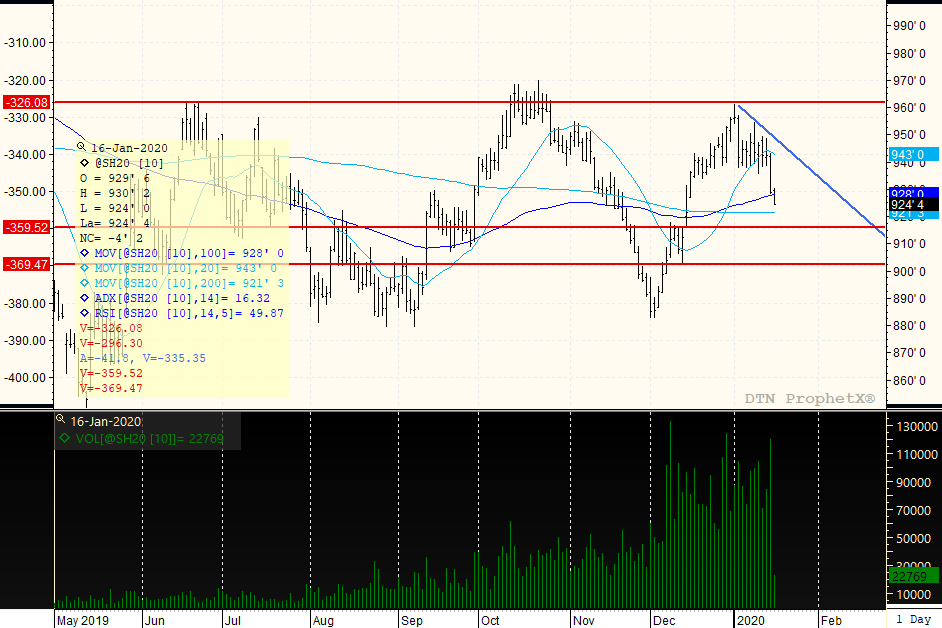

- March beans violated key swing support at $9.33 leading to a quick sell-off towards the next line of defense which is from $9.21 / $9.22.

- March soyoil now has a visual top in place (along with beans), and also continues to attempt to find its point of stability. For the day, 3290c-33c is a good place to start should we go there, with no guarantees that it can hold. Could maintain a short position in March soyoil, and if we close under 3290c then 3250c is doable.

- March meal prices are back under $300.00, but the $295.00-$297.00 level has been a good place to get coverage, and with soyoil/meal correcting should probably price in this vicinity.

- March corn cannot seem to leave its $3.71-$3.91 trading range, with funds short and prices trading back below resistance from $3.86 1/2 to $3.87. Trendline support now crosses at $3.78, just above the lows placed on the USDA report.

- March wheat trades to its key support level at $5.63, which is trendline support for this pullback, and a violation here would still find support even down to $5.55. Given the very strong performance, if short would be scale down covering from $5.55 to $5.63, perhaps trying the long side if prices seem to stick.

MARCH BEANS

The overall trading range is from $9.15-$9.61, but the top in place suggests that perhaps prices could also fall to the bottom red line at $9.00 for an extension trade lower for $9.00-$9.45 trading range. The break of the pivot point of $38% retracement level of $9.33 suggests that $9.21/$9.22 will come into play without much back support to stop the overall decline. The 200 -day moving average is located at $9.21, and the market turned higher to trade to $9.61 after stabilizing at $9.22. Therefore, would look for $9.21/$9.22 to offer support initially, and if short could scale down taking something off at this level, then wait to see if prices can work lower still. The trend is still weak at 16, but a visual top of resistance is now operating and may be hard to overcome at this point.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

The Q1 2024 GDP was 1.6 percent, well below the pre-report consensus expectation of 2.4 percent, and down from 3.1 percent in Q1 2023 and 3.4 percent in Q4 2023. That rate was the slowest in almost two years, dating back to Q2 2022. Recall that in the 2 February Ag Perspectives report on...

The Q1 2024 GDP was 1.6 percent, well below the pre-report consensus expectation of 2.4 percent, and down from 3.1 percent in Q1 2023 and 3.4 percent in Q4 2023. That rate was the slowest in almost two years, dating back to Q2 2022. Recall that in the 2 February Ag Perspectives report on...

As WPI readers likely well know by now, U.S. gross domestic product (GDP) grew at an inflation- and seasonally-adjusted 1.6 percent rate in Q1 2024, which missed economist’s 2.4 percent expectations. The data sent shockwaves through U.S. financial markets with U.S. stocks and bonds openin...

As WPI readers likely well know by now, U.S. gross domestic product (GDP) grew at an inflation- and seasonally-adjusted 1.6 percent rate in Q1 2024, which missed economist’s 2.4 percent expectations. The data sent shockwaves through U.S. financial markets with U.S. stocks and bonds openin...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...