GOOD MORNING,

Prices continue to remain well bid with no reversal signals in sight. China continues to be around the market, Black Sea vegoil values are rising, and dryness in various parts of the world continue to add to worries over production. Funds continue to own the market in lieu of these concerns while better producer engagement has been noted as beans traveled over $10.00 and corn $3.70. Rumors continue that China has purchased more US beans, but noted they could be buying Brazil as well for Feb. shipment.

WEATHER

--The US is drier over the next 10 days, with some rains in the Delta and the Southeast from tropical storm Sally, which is forecast to turn into a hurricane this week.

--Argentina dryness is expanding, which is stressing about 1/3 of the wheat belt. Brazil remains behind in planting with some showers but still needs more rainfall. Black Sea remains dry this week with showers limited.

REPORTS

Crop Progress

Corn: Down1% to 60% good/excellent, which was as expected. Small improvement was noted for Illinois, but Iowa was lower. North Dakota ratings were down 6% for G/E, which could have been frost damage. Dented: 80%. Mature: 41%. As expected, 5% of the crop was harvested, mostly outside of the Midwest states.

Beans: Down 2% to 63% G/E, with conditions dropping the most in the Dakotas, Minn, and Wisconsin. Illinois improved slightly, up 3%. Dropping leaves: 37% vs. 20% week ago, and 13% year ago.

Spring Wheat: 92% harvested vs. 75% year ago, and against the 92% average.

Winter Wheat: 10% planted vs. 6% year ago, and against 8% average.

ANNOUNCEMENTS

Brazil's SECEX estimated Sep 14 corn exports averaged 384,200 mt vs. 306,800 mt year ago. Bean export estimated through the first two weeks of Sep. averaged 197,000 mt vs. 219,200 mt year ago.

The Trump administration denied retroactive from 2011 to 2018 biofuel blending waivers that would have exempted oil refiners from requirements to blend biofuels into their fuel mix, according to the EPA.

Russian Ag consultancy reported that Sep Russian grain exports could set record volumes. At this point, 1.9 mmt of grain has been shipped, and the group is projecting that around 5.85 mmt could be sent in Sep, surpassing the 5.77 mmt in August.

The director for US Grains Council said that global ethanol production is expected to be 20% lower this year as the market moves through Covid, while recovery in output back to pre-pandemic levels will not be realized until 2022. About 23 bln liters of ethanol production has been lost in 2020, which has shuttered more than 250 ethanol plants across the globe, according to Brian D. Healy, speaking at the Platts APPEC 2020 virtual conference.

China's pig herd rose 31% in August vs. last year, while the sow herd was up 37%, said the Ministry of Agriculture and Rural Affairs. The announcement follows a major push to rebuild the herd after it was devastated by ASF.

DELIVERIES

Beans: 11

Soyoil: 33

Meal: 57

Corn: 276 Wells Fargo cust. puts out 276, JP Morgan stops 275

Wheat: 60

CALLS

Calls are as follows:

Beans: 3-5 higher

Meal: .30-.60 higher

Soyoil: 10-15 higher

Corn: 1-1 1/2 lower

Wheat: 3 1/2-4 lower

OUTSIDE MARKETS

The stock market is up 180 pts with crude oil firmer trading to $38.02/barrel. The US dollar trades down to 92.78.

TECH TALK

- November bean prices continue to rally, locking up with day before settlements to post new contract highs this morning. Charts are still positive, and the chance of moving towards $10.20 /$10.35 continues. Bulls will now use $9.95-$9.98 as a key support point in Nov beans for a market with a high that is yet to be determined.

- Dec meal now tests key support at $321.00 which holds for congestion trade. Target high is still from $330.00-$335.00, and the chance of testing previous highs at $328.00 remains a better chance than not.

- December soyoil continues its uptrend, which resumed out of a triangle pattern to the upside. Target high is 35c as the market tests its recent high trade at 3457c.

- December corn major support levels now move up to $3.55, and though prices have backed away slightly from $3.71 the uptrend has not been dented. Expect buying to continue on a pullback towards $3.63/$3.65, with possible new highs into the $3.75 level.

- December wheat price action continues to struggle the most, but still consolidates from $5.39-$5.42 where both the 200- and 20-day moving averages converge. Continuing to test key moving averages eventually suggests they are broken, and trendline support on a break under $5.40 is still visually present at $5.38.

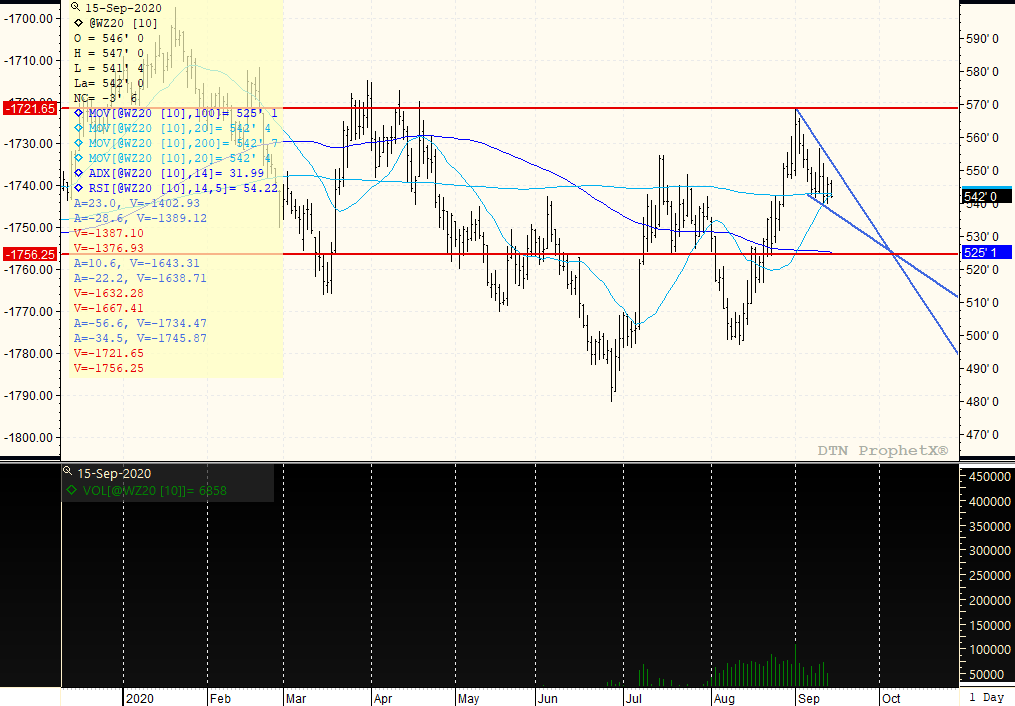

DECEMBER WHEAT

The overall direction has turned sideways from higher, with the ADX trend weakening a bit falling to 31. This chart is set up for strangling or straddling price direction between the red lines of $5.68 at the top, and $5.25 at the bottom. The descending triangle which has formed recently suggests that further weakness is ahead, and that prices may eventually break down to test $5.25. However, that level would find very good support as technically it is the bottom of the trading range.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

The CBOT was mixed on Wednesday with wheat futures dropping amid fund selling due to a stronger U.S. dollar and easing Russian FOB offers while corn drifted lower in lackluster, low-volume trade. While the grains were on the defensive, the soy complex found some support from technically related...

The CBOT was mixed on Wednesday with wheat futures dropping amid fund selling due to a stronger U.S. dollar and easing Russian FOB offers while corn drifted lower in lackluster, low-volume trade. While the grains were on the defensive, the soy complex found some support from technically related...

A Washington International Trade Association discussion on trade policy with former officials from both the Trump and Biden administrations reinforced the bipartisan agreement on some trade policies. A day after House GOP representatives slammed USTR Katherine Tai for the Biden Administration&r...

A Washington International Trade Association discussion on trade policy with former officials from both the Trump and Biden administrations reinforced the bipartisan agreement on some trade policies. A day after House GOP representatives slammed USTR Katherine Tai for the Biden Administration&r...

USDA reports that per capita flour consumption in 2023 fell to the lowest level in 37 years. Flour production and exports were lower, but so were flour imports. The question is why? It has been noted that consumers in developing countries with rising incomes tend to switch from rice consumption...

USDA reports that per capita flour consumption in 2023 fell to the lowest level in 37 years. Flour production and exports were lower, but so were flour imports. The question is why? It has been noted that consumers in developing countries with rising incomes tend to switch from rice consumption...