GOOD MORNING,

Price action remains extremely technical and on the defensive over disappointing ideas that the trade war may extend into 2020. The US Senate this week passed a bill supporting the Hong Kong protesters that infuriated China. According to a report from unnamed trade sources, the reason for the latest delay is that Beijing is pressing for more extensive tariff rollbacks, while Trump counters with threats of raising tariffs if a signed deal is delayed. The Wall Street Journal today reported that un-named Chinese officials have invited US trade negotiators to a new round of face-to-face discussions in Beijing, hopefully before the US Thanksgiving holiday. This has created a bit of morning short-covering for the start of today's session.

Yesterday, funds added to net short positions in corn and liquidated beans. However, bean prices seemed to be laboring to the upside, and the story finally produced a flush of length from the market. Question now is will funds go short everything but soyoil? They are even in wheat, while retaining a near record long in soyoil, which is piggy-backing off palm oil prices where production in the Far East is not expected to keep up with growing biodiesel demand in the coming year thus tightening stocks.

WEATHER

Temperatures are warming across the Midwest, with rain arriving this weekend. Light to moderate showers will impact the eastern Corn Belt, while the western Corn Belt should see drier weather through the weekend. The 6/10 day outlook features variable temperatures with above normal precipitation. In South America, mostly dry weather and above normal temperatures this week in Brazil's Parana and southern Mato Grosso will deplete moisture for developing beans. Scattered rainfall in northern Mato Grosso is beneficial. Weather for now is a neutral input, but a return to dryness in regions of Brazil and Argentina will require that some weather premium be added back for the possibility of lower production.

REPORTS

Export sales:

Beans: 2019/20 net 1.52 mmt (vs. an expected .800-1.4, better than expected with China taking the bulk of sales)

Meal: 2019/20 net 196,400 mt (vs. an expected 100-450 tmt low end and should remain competitive moving forward)

Soyoil: 2019/20 net 39,100 mt (vs. an expected 5-25 kmt - good sales, over the expected)

Corn: 2019/20 net 788,000 mt and 2020/21 net 45,900 mt (vs. an expected 400-900 kmt, higher end of estimates with SA offers very limited if any for Q1)

Wheat: 2019/20 net 437,700 mt (vs an expected 200-500 kmt, moderate to routine sales, but towards the higher end)

Sales were better than expected across the board, but did not at the end of the session bring additional strength to corn.

ANNOUNCEMENTS

Talks between Canada's CN railroad and the union members that are striking are reportedly making progress, according to Canada's transport minister.

Asian importers will likely be competing for Argentine wheat for Q1 2020, with 8 mmt of wheat forward sold for exports, as reported by traders.

CALLS

Calls today are as follows:

beans: 2 1/2-3 higher

meal: 1.50-1.80 higher

soyoil: 10-15 lower

corn: 1/2-1 higher

wheat: 2-2 1/2 higher

OUTSIDE MARKETS

Outside markets feature higher stocks, up 30 pts, and firmer crude at $57.47/barrel. The US dollar weakens to 97.27.

TECH TALK

- Charts were building in stiffer resistance levels in Jan beans that finally resulted in a break towards the $9.00 benchmark. Only question now is will $9.00 become a new low, or do prices slide to $8.80 to $8.90, which should prove to be a value level.

- March corn sets double lows at $3.76 3/4, with very big resistance levels intact from $3.83-$3.86. The chart will not find short-covering panic until we trade over $3.86. Trendline support for the day is still close by at $3.75, should we go there, and would expect a bounce if we do.

- March wheat continues to be a well bid market, now trading up and away from lower moving averages and a successful test of the $5.01 level. Best resistance is close by at $5.26.

- Dec soyoil futures break back below 31c as trades unwind buy soyoil/sell meal trade. Very good support is now located a bit higher than before, and would expect a pullback to 3080c to offer very good support. In the big picture, the movement is beginning to turn sideways from higher, from 3050c lows up to 3140c highs.

- Dec meal trends outside of its recent range to the downside of $300.00, but is back over this level after testing $299.00. Would still look for a sideways continuation pattern of trade from $300.00-$310.00 despite the outside movement below $300.00.

Would note that most of the markets begin near or on trendline support for the day, which could hold if tested again.

Jan beans: session lows right on support at $9.02

Dec soyoil: 3090c

Dec meal: $299.50

March corn: $3.76

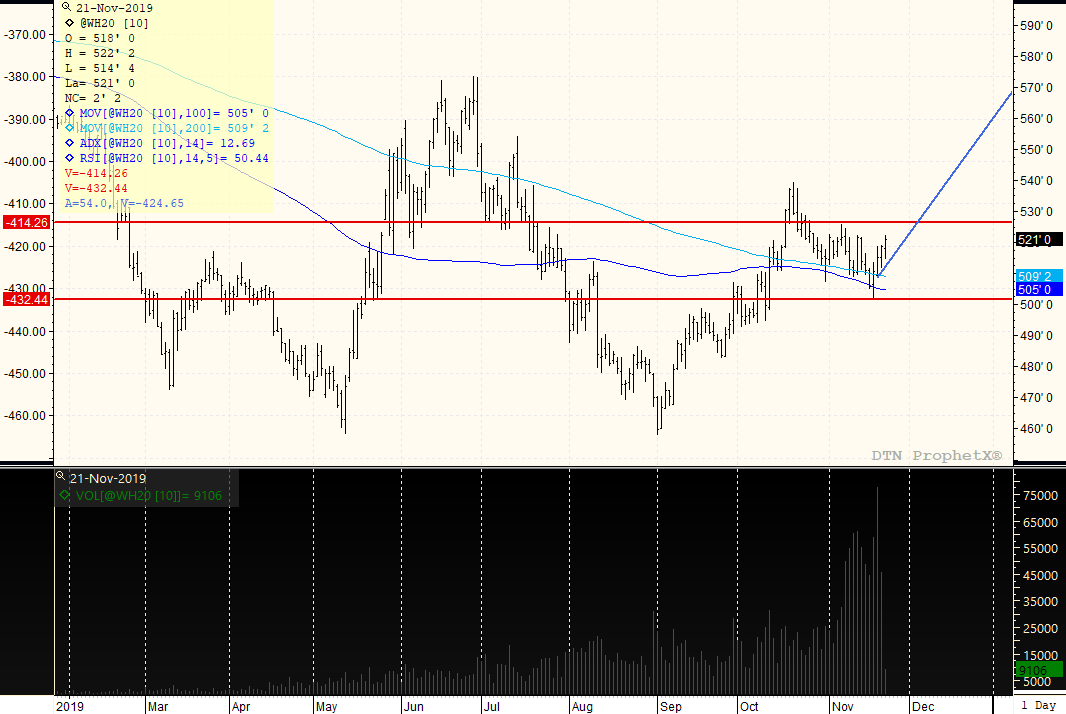

MARCH WHEAT

Prices continue to be well bid, having tested levels below moving averages this week with a test of $5.01 which held with a rejection low. Prices are moving up and away from moving averages which is a friendly technical input, and implies that setbacks should see support. Would look for price action to match the last peak high of $5.26 before resistance sets in for a $5.00-$5.25/$5.35 trading range. The trend remains weak with an ADX of 12 (anything under 25 is weak trend) so the market should stop at trading range highs if we move into $5.25 to $5.28 resistance. Could straddle/strangle the range as well.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Large supplies and a strong dollar took their toll this week on corn and soybeans, but they still managed to outperform. Weather worries pushed wheat higher for a seventh straight session, and pork finally took a fall. There was high volume trading in corn today but without any strong fee...

Large supplies and a strong dollar took their toll this week on corn and soybeans, but they still managed to outperform. Weather worries pushed wheat higher for a seventh straight session, and pork finally took a fall. There was high volume trading in corn today but without any strong fee...

The Market Brazil has been winning the soybean export war, and imported biodiesel feedstock threatens domestic crush margins, but Chicago trading this week appeared to shake off such concerns. July soybeans traded lower for the past three trading sessions but larger gains achieved at the beginn...

The Market Brazil has been winning the soybean export war, and imported biodiesel feedstock threatens domestic crush margins, but Chicago trading this week appeared to shake off such concerns. July soybeans traded lower for the past three trading sessions but larger gains achieved at the beginn...

The Q1 2024 GDP was 1.6 percent, well below the pre-report consensus expectation of 2.4 percent, and down from 3.1 percent in Q1 2023 and 3.4 percent in Q4 2023. That rate was the slowest in almost two years, dating back to Q2 2022. Recall that in the 2 February Ag Perspectives report on...

The Q1 2024 GDP was 1.6 percent, well below the pre-report consensus expectation of 2.4 percent, and down from 3.1 percent in Q1 2023 and 3.4 percent in Q4 2023. That rate was the slowest in almost two years, dating back to Q2 2022. Recall that in the 2 February Ag Perspectives report on...