GOOD MORNING

Prices are mixed with new contract highs in corn, but everything lower this morning as head into first day and end-of-month profit-taking. Prices start out the PM session on a bullish note, but fund profit-taking seems to be the theme heading into the last day of November. Jan beans nearly hit $12.00, but will begin on its lows today. In terms of news, traders continue to analyze the slow-down and recent bean cancellations out of China. On the other hand, a vessel carrying 30,500 mt of beans from the US is due to arrive in Brazil, according to the Paranagua port authority, as supplies in this country are tight until new crops can be harvested. For corn, the International Grains Council lowered global production by 10 mmt to 1.146 bln while doubling its projection for China corn imports to 16 mmt.

The Chinese economy is improving, which could stimulate demand for most commodities. Funds remain long across the board, which is probably why the last day of the month is weighing on futures this AM, as weather patterns still remain dry, (for the most part) in SA.

WEATHER

The weather situation continues in a word to be bullish. There were some periods of showers over southern Brazil this weekend, but the pattern goes back to a classic La Nina this week. Rains were noted in Parana, with dryness still stressing beans in the central and south. Mato Grosso do Sul will see the least amount of moisture until the end of the week. Weekend weather offered scattered storms over Argentina with most rains significant in the northeast but not anywhere else. Bottom line remains one of concern for Argentina except for the northeast, while major growing areas need a substantial amount of rain. Through the next 5-7 days, rains in the northeast will remain status quo for Argentina, but rains in other areas will be needed. Areas that are too dry are around 35% for both areas.

ANNOUNCEMENTS

China's customs administration announced it had approved imports of sorghum from Mexico as the country looks to add new origins of grain to feed the increased size of its livestock.

Russia's IKAR reduced their grain crop to 78 mmt from 84 mmt last year. Russia may increase the size of its grain export quota planned for Feb. 15-June 30 to 17.5 mmt from 15 mmt, to stabilize its domestic market after recent price increases.

OPEC and its members have yet to find common ground regarding 2021 oil production policy and the first round of talks Sunday had not reached a compromise. The group is reportedly interested in rolling over 7.79 mln bpd of existing cuts, but parties to the policy meeting are at odds over the length of the rollover extension.

Argentina's bean planting advanced 10.6% last week to 39.3% or the projected planted areas of 17.2 mln ha, while wheat harvesting jumped 11.1% WOW to 30.9%, as reported by the BA Exchange

CALLS

Calls are as follows:

beans: 10-12 lower

meal: 1.80-2.20 lower

soyoil: 40-50 lower

corn: 1/2-1 lower

wheat: 5-6 lower

OUTSIDE MARKETS

Lower for equities, which are down 130 pts, and lower for the US dollar, which trades down to 91.55. Crude oil is slightly lower trading down to $44.42/barrel. Gold prices crack the $1800/oz mark, down $15.00/oz to 1762.30/oz.

TECH TALK

- Key levels of resistance are holding today, namely $12.00 Jan beans, 38c Jan soyoil, $4.40 March corn, with March wheat trading down to $6.00. These tops, followed by a lower start, are weaker technical signals than have been previously noted, implying that a larger correction into trading ranges from the top could be forming, and may become the major theme for the week.

- March wheat prices are sideways with the least amount of trend with an ADX of only 20, showing a sideways chop. Prices are locked from $5.90 to $6.30, with a target low on another break closer to $5.85. Resistance is stronger than support here, with rallies still for selling.

- March corn places a new contract high breaking out over $4.35 3/4 tops at $4.39 1/2. The uptrend is strong here, and pullbacks will be buying opportunities. The new trading range is from $4.20 up to $4.40 with a target at $4.50 or better.

- The Jan bean chart places multiple tops at $12.00 over the last week, and failure to move above this level will now find better resistance against these tops. Traders may now begin to sell the market and place close buy-stops over $12.00. The overall trade now defines a sideways pattern from $11.80-$12.00, so any trade under $11.80 becomes problematic for the bull, as there is plenty of back and fill down to $11.66/$11.70. The chart remains overbought, suggesting that a better break could be coming.

- Jan meal prices begin the evening with a gap -higher trade, which amounts to a rally towards the $400.00 level again. The gap was easily filled, with prices now starting the session on key support lows. A break of $393.00 would move through trendline support and open the door for a larger pullback towards $386.00, the bottom of the trading range.

- Jan soyoil charts now appear a bit more toppy as well, but still retains a 37c-39c trading range. Double highs are located at 3865c while prices start the day heading down towards trendline support at 3760c.

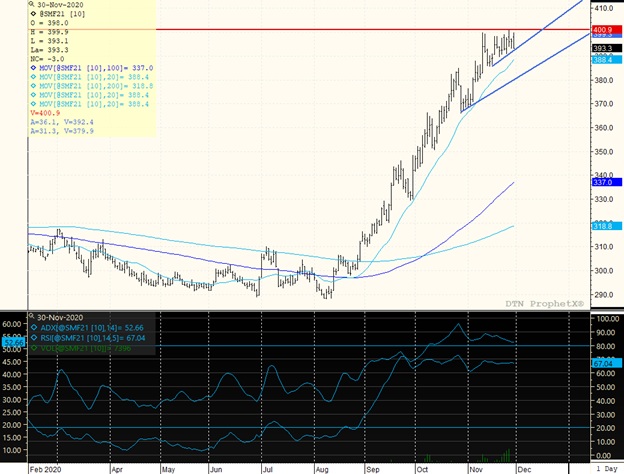

JANUARY MEAL

The major trend is higher, with major support now located at $386.00 and resistance at the contract high of $401.30. The ADX is extremely strong at 52, meaning the path of least resistance is still higher. So far, an ascending triangle is forming as prices continue to hold pullbacks at higher levels, and a breakout over $401.00 suggests that prices can accelerate towards $410.00. While the major trend is higher, the return to important lows makes the chart more vulnerable to a larger pullback, and the small gap left open to the upside was easily filled. If long, would perhaps want to take something off the table at this point, and keep the rest as long as major lines of support as shown in blue are not violated. We begin the morning right on trendline support at $393.00, which increases the chance that we break it and head lower. Think we know at the start of the session if trendline support at $392.50/$393.00 will hold.

ON THE CALENDAR

Export inspections are out at 10:00 central time.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...