GOOD MORNING,

Quiet markets are subject to quick bounces and breaks. Yesterday, what was a quiet atmosphere suddenly turned higher as trade war news headlines splashed again, this time not from the US, but from China. The South China Morning Post reported that China is expected to buy more US agricultural goods in hopes of delaying a series of tariffs that will take effect in October and December, as well as ease the supply ban against Chinese telecom giant Huawei Technologies. The fact that China made the statement they will purchase more US beans, betting that it’s a good faith statement to open doors on meat exports as well, got the attention of the algo traders who were quick to buy something.

Today, China announced it will exempt American industrial grease and some other products from tariff hikes, while keeping penalties on soybeans and other major US exports ahead of negotiations next month. A list of 16 items, including fish meal for animal feed and some chemicals, would be exempt from the penalties of up to 25% imposed in response to Trump's tariffs on Chinese products, the Ministry said.

Yesterday’s headlines sparked short-covering in all three classes of wheat, which closed the day into positive territory for a second day. Concerns over Australian and Argentine wheat was supportive. Dryness in Argentina's Cordoba, La Pampa, and BA regions helped to feed into the short-covering rally in wheat which honored its seasonal tendency to rally. Countering that, huge Black Sea harvest inventories may add to world wheat numbers on Thursday.

WEATHER

No freeze yet which is good for areas where crops are still maturing. This is particularly true for beans, where 6.136 mln acres have yet to set pods, including 1 mln acres in Illinois, 552,00 in Iowa, 864,000 in Ind., 816,000 in Mo., 506,000 in Kansas, and 315,000 in South Dakota. Temperatures remain above normal for now, with below normal rainfall, bearish.

ANNOUNCEMENTS

China's state planner is considering plans to release pork from the strategic reserves for the upcoming holiday including the Lunar New Year in order to control prices. China has banned the import of hogs, wild boar, and related products from the Philippines due to ASF controls.

China and Argentina have come to a bilateral trade deal where China will import Argentine bean meal. Argentina's Ag Ministry said they will sign an agreement with China in BA Wed.

Ukraine's Grain industry group announced it's 2019 corn production estimate to be 35.4 mmt, up 900,000 mmt from the prior outlook.

Brazil's Deral forecasting agency estimated summer corn planting progress at 9% complete, lagging the 13% pace yr ago.

STORIES

The White House invited biofuel company officials to meet with the administration Wed to discuss the direction of US biofuel policy.

DELIVERIES

- beans: 226

- soyoil: 60

- meal: 96

- cbot wheat: 23

- corn: 261

CALLS

Calls today are mostly lower across the board, congesting after yesterday's rally:

- beans: 1-2 lower

- meal: 30-50 lower

- soyoil: steady

- corn: 1/2-1 lower

- wheat: 1-2 lower

The markets closed slightly lower overnight but this is the kind of day where prices can open weaker and quickly turn two-sided. Expect that more to continue than not. Soyoil may turn higher vs. meal.

Outside markets feature firmer crude oil trading to new highs at $58.30/barrel and a stronger US dollar trading up to 98.66. The Dow is up 54 pts.

TECH TALK

The wheat market tends to be the leader on the way up and the leader on the way down. The corrective bounce in Dec wheat takes us into key resistance now at $4.83/$4.85, and as such would look for the market to perhaps stall at this level. However, any trade over $4.85 finds little back resistance to stop a larger rally which could take us back to $5.00. If short, have to have a very tight buy-stop in just above $4.86 in order to not get caught in a larger up-move.

Dec corn finally rallies to its first key resistance level of $3.63, and would look for trade over that level to take us towards $3.66 and double tops at $3.70 where sellers may be waiting to hop on board. Nov beans rally back towards $8.80 showing its sideways locked in range at $8.50-$8.85. The pattern in beans has been to post new lows without any downside follow-through, so if short have to keep that in mind.

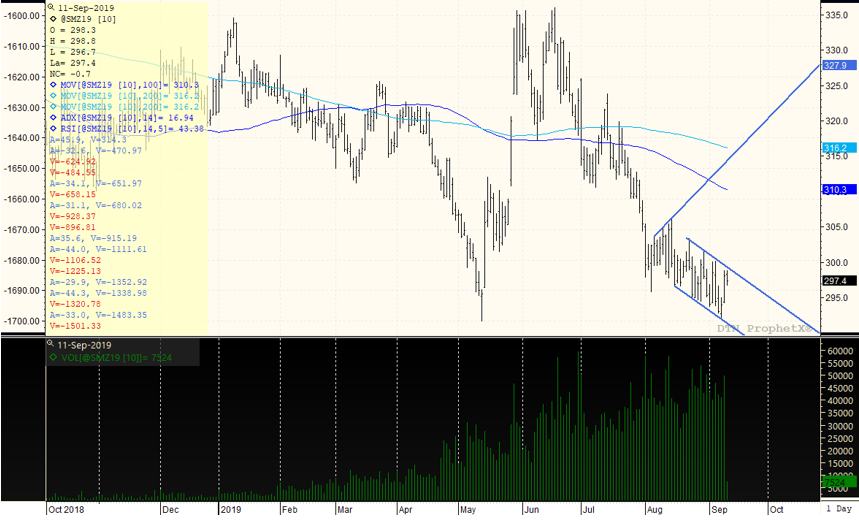

Dec meal bounces off $292.00 trendline support and moves close to trendline resistance at $300.00. The downtrend channel for Dec meal remains in place, and the PM session high at $298.80 is right up against the top of channel. Dec soyoil, on the other hand, is close to trading range lows and beginning to build in more support after testing 2820c this week. Would prefer to be a buyer of Dec soyoil today as the chart has turned sideways from lower, though has to clear 2875c in order to go to 29c again. However, charts are still suggestive that we re-visit this level at some point.

Here are the key resistance levels today, and most of the markets have traded close to them:

- Nov beans: $8.77/$8.80

- Dec corn: $3.63/$3.66

- Dec wheat: $4.85/$4.86

- Dec meal: $299.00

Any trade above these levels will trigger more fund buying.

DECEMBER MEAL: The major direction is sideways/lower, and the market was close to taking out its ctr low at $291.60 this week. The price pattern has been to break to new lows, but there is little follow-through to the downside when lows are hit, with reversal activity. The down-trend channel is directing the major direction, and the PM session high close to $299.00 is right at the top of channel. The trend is weak so would look for the chance that we hold resistance today for further retracement lower. Overall trading range is from $291.60 up to $300.00. At any point in time should we clear the top of the channel the $290.00-$300.00 would become a base of overall support and suggest a much higher move is on the way.

ON THE CALENDAR:

EIA production is expected to be up 1% while stocks are expected to be down 2%,.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America, China, South America

Russian Grain Markets: 15–19 April 2024 International sanctions and reverse measures Russia adopted towards “unfriendly” countries may leave Russia without proper genetics for this spring’s planting campaign. While small grains are available due to long term domestic see...

Russian Grain Markets: 15–19 April 2024 International sanctions and reverse measures Russia adopted towards “unfriendly” countries may leave Russia without proper genetics for this spring’s planting campaign. While small grains are available due to long term domestic see...

The spring 2024 wheat rally continues as weather threats linger for the U.S., Europe, and the Black Sea. Weather forecasts that offer a challenging outlook for the 2024/25 Northern Hemisphere crop are forcing funds to keep exiting short positions, with the resulting positive technical developme...

The spring 2024 wheat rally continues as weather threats linger for the U.S., Europe, and the Black Sea. Weather forecasts that offer a challenging outlook for the 2024/25 Northern Hemisphere crop are forcing funds to keep exiting short positions, with the resulting positive technical developme...

Hecho en Mexico While outgoing Mexican president and populist AMLO tries to shutdown American farmers, the U.S. government just keeps giving to Mexico. The de minimis duty is about to go away. The personal free import allowance is complex. Most American citizens reentering the country think of...

Hecho en Mexico While outgoing Mexican president and populist AMLO tries to shutdown American farmers, the U.S. government just keeps giving to Mexico. The de minimis duty is about to go away. The personal free import allowance is complex. Most American citizens reentering the country think of...

South Africa’s Crop Estimates Committee warns that instead of a previously expected 13.8 percent increase in maize production in 2024/25, output could fall to a five year low on account of El Nino. The shortfall is particularly acute for white corn, with the price rising 30 percent thus f...

South Africa’s Crop Estimates Committee warns that instead of a previously expected 13.8 percent increase in maize production in 2024/25, output could fall to a five year low on account of El Nino. The shortfall is particularly acute for white corn, with the price rising 30 percent thus f...