GOOD MORNING,

Prices opened close to home, higher for soy with some light profit-taking in wheat. All markets are higher heading into the close led by wheat. Minneapolis wheat trades into contract highs, and oats have traded into all-time record highs. Matif wheat made new contract highs yesterday, and corn posted further gains for the ninth day in a row which keeps current wheat up-trends intact.

The Goldman Roll begins today with rolling November to January contracts. China is back from holiday today, and traders will be looking for signs of demand. So far, it has been a quiet week. Egypt tendered for wheat and purchased a combination of Russian/Ukraine yesterday.

Basis is steady to mixed around the country. The chatter around the country is that corn and bean yields are coming in better than expected. The USDA October report will hone in on those yields. Trade expectations going into the report is for a bean yield that could be higher, corn yields slightly lower, and wheat numbers remaining friendly.

Brazil's CONAB forecast the following:

bean production: 21/22 at 140.75 mln mt vs 137.32 mln mt prev. 20/21 crop at 135.912 mln mt

total corn production: 21/22 at 116.31 mln mt, vs. prev. at 86.998 mln mt, 20/21 crop at 85.749 mln mt

wheat production: 2021 at 8.191 mln mt, prev. at 6.235 mln mt

WEATHER

--US weather remains dry in the west and plains but nuisance rains continue in the east. Plains do need rains which are forecasted to arrive in the next two weeks.

--Argentina is dry the next two weeks with more threats of frost. Brazil is seeing some beneficial rains for nearly all growing regions. Most other global regions see favorable or neutral forecasts. Brazil's weather remains beneficial for planting.

REPORTS

Export sales:

beans: 21/22 net 1.04 mt (vs. an expected 600-1.2 mt)

meal: 20/21 net minus 21,700 mt and 21/22 net 369,600 mt (vs. an expected 25-300 mt)

soyoil: 20/21 net minus 5,000 and 21/22 net 38,500 mt (vs. an expected minus 5 to 40 mt)

corn: 21/22 net 1.27 mt (vs. an expected 350-800 mt)

wheat: 21/22 net 333,200 mt (vs. an expected 200-500 mt)

Wheat: sales were neutral, up 15% vs. pre, wk, but down 19% from the 4-wk ave. Increases were primarily for Mexico and South Korea.

Corn: sales good, primarily to Mexico, with 100,000 mt switched from unknown destination. Exports of 974,600 mt were primarily due to Mexico and China (212,300 mt).

Beans: sales were good, with China in for 671,300, including 131,000 switched from unknown.

Meal: sales for 21/22 over the expected, primarily for the United Kingdom and Columbia, Philippines

Soyoil: 21/22 sales were good, primarily for Morocco and Canada.

ANNOUNCEMENTS

World food prices rose for a consecutive month in Sep. to reach a 10-yr peak driven by gains for cereals and veg oils, the UN agency announced. FAO also projected record global cereal production for 2021, but said it would be outpaced by global consumption.

India's cotton exports could fall by 36% for 21/22 as domestic demand has been rising amidst lower supplies. Sumeet Mittal, general manager for India cotton business, said that exports could down to 5 mln bales for the new season.

Ukraine's Ag Minister cut wheat production 500K to 31.5 mmt vs. USDA at 33 mmt, and corn down to 37.1 mmt vs. USDA at 39 mmt.

Brazil exported 4.8 mln mt of beans in Sep., up 13% on the year with volumes destined mostly for East Asia, with corn exports sharply lower.

CALLS

Calls are as follows:

beans: 3-5 higher

meal: .50-.80 higher

soyoil: 30-35 higher

corn: 1 1/2-2 higher

wheat: 3-5 higher

Outside markets feature a weaker US dollar at 94.08 and lower crude which trades down to $74.96/barrel. Stocks are 290 pts higher.

Tech talk:

Soy: November beans are trying to head into a trading range which could be from $12.35-$12.65 if prices can remain in the green today. Trendline support on a break is close to the low of $12.31, crossing at $12.25/$12.28. Looks like the chart is trying to make a case for the reversal this week to build on gains. December meal reverses out of double lows of $320.00, trying to correct its oversold status of an RSI at 28%. There is air over the market, so think we could build on gains and head into a $320.00-$340.00 trading range. The December soyoil chart remains bullish, peaking this week at 6190c before entering into a congestion trade. The 100 day moving average at 6020c was tested, but as in all good markets prices are back above this level. The 60c level now becomes a springboard to what could be an eventual 62c-64c trade.

Grains: December corn is locked in a sideways trade and establishing its highs and lows before the October report. The overall trading range is from $5.25-$5.45/$5.48. Would look for a continuation of this price pattern, as think the market is walking back and trying to see where the value low is located. Whether it's $5.15 or $5.25, would probably elect to price or cover a partial short as this market has had a healthy bid to it at market lows. December wheat also retains a good bid, with prices this morning bouncing back towards recent highs. The chart formation appears to resemble a bit of a bull flag, meaning price congestion is taking place from $7.40-$7.63 after a vertical rally. Prices over $7.63 targets $7.75/$7.80 without much resistance in place. If short, would elect to cover something given the fact that we remain very close to recent market highs. Strong markets offer pullbacks that hold, which is the case here.

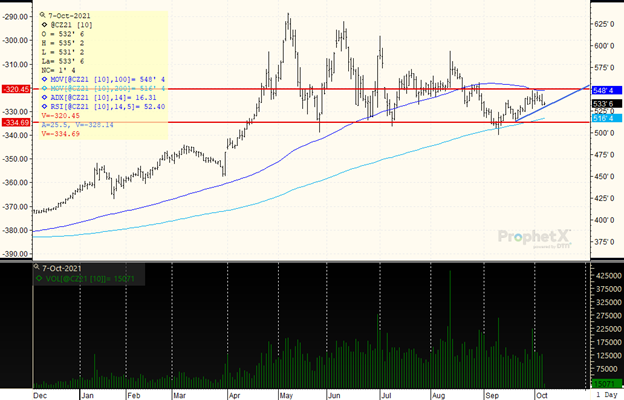

DECEMBER CORN: The market is in a sideways range, bounded by trendline support at $5.25 on the downside and $5.48 on the up. Visual horizontal resistance and the 100 day moving average crosses at $5.48, making it a tough go to move above. Crossing to the downside of $5.25 opens the door to the 200 day moving average of $5.15. Buyers will be patient, as the trend is sideways and the fact that the market is testing trendline support is not bullish.

TAGS – Feed Grains, Australia

Most of the major agricultural commodity contracts opened today’s trading session in the red and stayed that way to the close. Only feeder cattle and lean hogs managed small gains on the day. New contract lows were hit for December soyoil, September SRW and September HRW. Volume was overa...

Most of the major agricultural commodity contracts opened today’s trading session in the red and stayed that way to the close. Only feeder cattle and lean hogs managed small gains on the day. New contract lows were hit for December soyoil, September SRW and September HRW. Volume was overa...

The headline for the CBOT on Thursday was the unexpected surge in soymeal export sales that boosted that market and new crop soybeans to strong gains for the day. Soymeal exports have been a prominent support for the market this year and their recent uptick after December futures fell to near $...

The headline for the CBOT on Thursday was the unexpected surge in soymeal export sales that boosted that market and new crop soybeans to strong gains for the day. Soymeal exports have been a prominent support for the market this year and their recent uptick after December futures fell to near $...