GOOD MORNING,

Prices were mixed overnight but gradually turned higher led by wheat, as traders seem more pre-occupied by what is going on in outside markets such as energies and stocks than Ags. Funds hold a slight short in wheat but could be switching to long into the report tomorrow. Look for further position - evening, as funds may book profits while end-users may seek coverage on market breaks. Beans and soyoil struggle at the start of the PM session, while grains remain in the green. Thursday is a huge day with Sep. Quarterly Stocks report, export sales, first notice day for Oct. futures, and end-of month/quarter. Can you say "V" for volatility?

The demand front is quiet with rumors that China is around the markets before they go on holiday next week. There were no bean announcements so far this week, adding some weight to prices. Energy prices are struggling with weaker palm, adding to soyoil losses. Corn prices remain well bid as traders buy corn/sell beans based on current technical chart patterns. Wheat prices are firmer as prices continue to consolidate in recent ranges. Brazil banned GMO wheat imports, which could reduce anywhere from 6-7 mmt from Argentina. Matif continues to make new highs on possible lower acreage/production due to seed problems and higher input costs such as fertilizer. Wheat tenders remain active.

WEATHER

--Rains begin to move up from Texas moving through the central and western Midwest this week, which will create some minor harvest delays.

--Argentina is in a below normal trend but has time to catch some rainfall. Brazil sees good rains in the south with expanding moisture in the northwest, central and eastern areas over the next two weeks, favorable for planting.

ANNOUNCEMENTS

Brazil's Deral estimates Parana bean planting at 7% complete vs. 3% week ago. ANEC forecast that soy exports will reach 4.735 mmt in Sep. vs. 5.041 mmt prev, week. Corn exports would reach 2.525 mmt in Sep vs. 2.779 mmt prev. week.

Russia has harvested 105.4 mmt of gain before drying and cleaning, the Ag Ministry reported. Exports for 21/22 are down 22.4% and total 9.9 mmt as of Sep 23. Wheat exports were 8.4 mmt over the season, down 19% from year ago.

Argentina's farmers have sold 30.5 mmt of beans from the 20/21 crop, after registering sales over a seven-day period of 495,300 tons. This lags the 32.3 mmt prev. season. The exchange estimates that 50.5 mmt of corn was harvested for 20/21 and expects a record 55 mmt crop for 21/22. Farmers also sold a total of 7 mmt of wheat for 21/22, with the BA Exchange forecasting the new wheat crop at 19.2 mln.

CALLS

Calls are as follows:

beans: 1-3 higher

meal: .50-.80 higher

soyoil: 20-25 higher

corn: 3-4 higher

wheat: 7-9 higher

OUTSIDE MARKETS

A higher stock market, up 140 pts. Crude trades down to $74.23/barrel with the US dollar firmer to 93.77. There are concerns that the US shutdown, looming at week's end, could hurt economic growth.

TECH TALK

- November bean chart remains vulnerable to further downside but is once again above its 200-day moving average which crosses today at $12.70. The trend is an extremely weak one with an ADX of only 9, meaning that prices are likely to continue in a congestion trapped sideways pattern from $12.70-$13.00 into the report. Price pattern does suggest that the ultimate direction could be lower if prices attempt but cannot get over the $13.00 level.

- December meal prices trends sideways, building a base of congestion trade from $335.00-$345.00. Prices stay low at the bottom of recent price action, which is more inherent behavior of a market with another potential break than otherwise. Target low is $330.00.

- December soyoil prices remain sideways but at the upper portion of its range as oilshare remains well bid. Would look for a 57c to 59c trading range to develop, and a strong possibility that prices target the 100-day moving average of 60c.

- Corn price action remains strong and more well defined as a market that still has the potential to move upward. Prices placed a new high for the move up at $5.41 3/4 this week, and pullbacks back to test $5.33 which should hold for another attempt at a new high. Chart is leaning sideways to higher which is triggering more buying interest. Target high is $5.51, the 100-day moving average, though interim resistance may also stop a rally at $5.45. Would look for upside follow-through and a likely test of recent highs based on the successful pullback in Dec. corn to the $5.30/$5.33 level.

- December wheat is also firmer this morning. Strong support is at the $7.00 level via converging lines of support from the 100 day and trendline. Prices did not even move towards there, an indication of strong market action. Look for wheat to trend back towards $7.25/$7.33 based on behavior and chart price action.

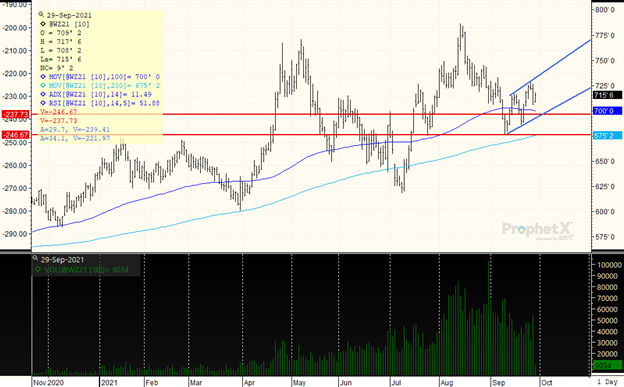

DECEMBER WHEAT

The market is in an uptrend channel from $6.88- $7.35. The 200-day moving and channel support nearly converge at $7.00, and while the price action approached it by testing $7.10-$7.12, the break now seems to be part of a continued $7.00-$7.35 trading range. The ADX remains trendless however at 11, meaning there is very little trend. Strong price action today moves prices up towards the recent highs, and would look for further advances. A wide uptrend channel has formed, as noted by the blue lines, and the low of $7.08 now looks to be a low for a market that could trend higher towards top of channel again, and towards the last peak high on the chart at $7.33.

TAGS – Feed Grains, North America

Most of the major agricultural commodity contracts opened today’s trading session in the red and stayed that way to the close. Only feeder cattle and lean hogs managed small gains on the day. New contract lows were hit for December soyoil, September SRW and September HRW. Volume was overa...

Most of the major agricultural commodity contracts opened today’s trading session in the red and stayed that way to the close. Only feeder cattle and lean hogs managed small gains on the day. New contract lows were hit for December soyoil, September SRW and September HRW. Volume was overa...

Non-Meat: In a first, a Europe-based company has sought EU approval to market lab-grown meat, in this case fake foie gras. Some member states have already banned such products. While lab-grown meat remains expensive, and plant-based meat substitutes have faced declining popularity, the increase...

Non-Meat: In a first, a Europe-based company has sought EU approval to market lab-grown meat, in this case fake foie gras. Some member states have already banned such products. While lab-grown meat remains expensive, and plant-based meat substitutes have faced declining popularity, the increase...

June 2024 total red meat and poultry stocks were up slightly from May but 5.4 percent below June 2023 levels due to sharp declines in poultry and pork stocks. Total poultry stocks were down 7.8 percent year-over-year (YoY) due to reductions in broiler slaughter for the month. Total pork stocks...

June 2024 total red meat and poultry stocks were up slightly from May but 5.4 percent below June 2023 levels due to sharp declines in poultry and pork stocks. Total poultry stocks were down 7.8 percent year-over-year (YoY) due to reductions in broiler slaughter for the month. Total pork stocks...