GOOD MORNING,

Prices are lower this AM as the Midwest saw a decent amount of rainfall over the weekend. Wheat prices trade near the lowest level since last Sep. 2019 as harvest continues across the US. So far, about 1/5 of the US HRW and SRW harvest has been completed. Russia's price for wheat was lower, which competes directly with US origin.

Crop conditions will be released today at 3:00 PM, and with scattered showers over the weekend ratings would be expected to be unchanged. One of the bigger upcoming reports involves corn and the 30 June Quarterly Stocks and Acreage Report, which is usually a market mover.

Soybeans are lower but may continue to see support on pullbacks as US beans remain at a deeper discount vs. Brazil origin. Talks remain constructive between the US/China.

WEATHER

West will see scattered showers through Tuesday, with temperatures near to above normal through Friday. The 6/10-day outlook calls for isolated showers continuing into midweek. There is now adequate moisture for much of the Midwest, which will foster growth. The Delta region remains drier through the weekend, imposing some stress though current moisture is adequate. Eastern Iowa is seeing rains this AM moving into northern Ill, and better rain chances today. Bottom line: rain moving through parts of the Midwest is bearish.

REPORTS

Commitment-of-trader's report as of June 16, disaggregated futures / options combined:

Beans: net long 21.183

Meal: net short 48,208

Soyoil: net short 4,786

Corn: net short 270,751

Wheat: net short 30,251

Funds pared back the corn short position, but the largest commitment is here to the short side, followed by meal. Overall, the corn short position makes the market vulnerable to short-covering activity.

Cattle-on-Feed:

"on feed" inventory as of June 1 was near unchanged, vs. an expected 1-2% deCline.

Placements: 99% vs. 96% expected

Marketings: 72% vs. 74% expected.

ANNOUNCEMENTS

Chinese authorities suspended imports of poultry products from a plant owned by US -based meat processor Tyson Inc that had been hit by coronavirus.

Russia's IKAR raised its estimate for Russia's 20/21 wheat exports by 2 mmt to 37 mmt. They raised wheat production to 79.5 mmt vs. 78 mmt.

Brazil's Arc Mercosul reported that the Safrinha corn harvest reached 7.9% of planted area vs. 17.2% year ago.

BUSINESS

Egypt purchased 59,000 mt of soyoil for their latest tender.

CALLS

The markets are called as follows:

beans: 1 1/2-2 lower

meal: .30-.80 lower

soyoil: 8-10 lower

corn: 1 1/2-2 lower

wheat: 1 1/2-2 lower

OUTSIDE MARKETS

Weaker crude, down to $39.12/barrel with the Dow up 200 pts. The US dollar trades down to 97.29.

TEACH TALK

- November beans retain a $8.65-$8.85 trading range, but continuing to operate at the highs of the range suggests that prices could exit to the upside for trade towards $8.92/$9.00. For the day the 100-day moving average is located at $8.75, and if we go there think it holds, and would cover a short.

- July soyoil prices remain well bid, with the 100- and 20-day moving average crossing under the market at 28c on a heavy break. Charts are more suggestive that there will be a run towards 29c. If short, would cover or try the long side on a break towards 28c.

- July meal has the opposite look trading into key lower support from $285.00/$286.00. However, if soyoil and beans recover at the open meal will follow.

- Sep. corn remains sideways with multiple tops at $3.39. However, the chart features higher lows which suggests that pullbacks are finding support. Could therefore try the long side of the market if opening weakness cannot break $3.33, as any trade over $3.39 will trigger more fund buying activity.

- Sep wheat prices attempt to stabilize near recent lows, and a trade back over $4.90 would set recovery in motion. Since prices begin close to trading range lows, think that down-side follow-through would have to come quickly or shorts may elect to cover something in for a $4.81 to $5.12/$5.15 range.

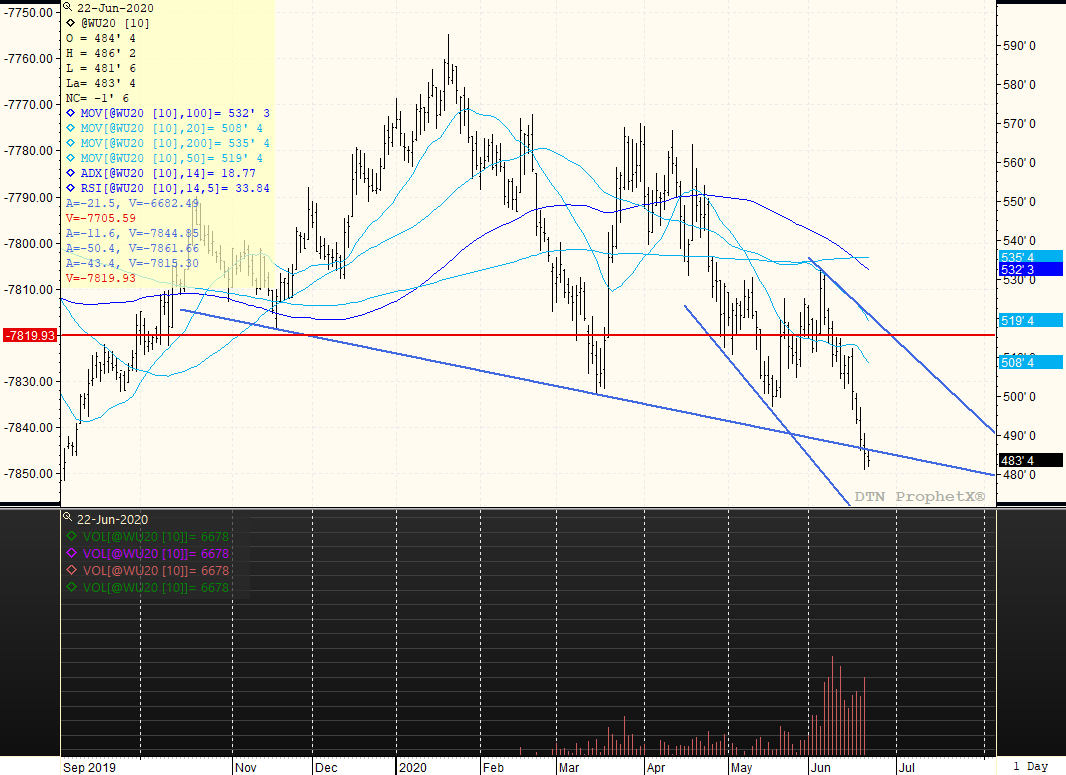

SEPTEMBER WHEAT

The overall trading range right now is from a $5.15 high down to current lows at $4.81. New lows beget new lows, and for now there is not a reversal signal at play to suggest that the downside is over. Key to recovery will be if the market can trade back over the violated down-trend line drawn back from Sep. lows and to the upside of $4.82. The market is slightly oversold at 33%, which does not call for corrective price action. A close over $4.90 would help to fuel a larger correction. A close below $4.80 opens the door for a slide towards $4.60/$4.70. Technically bears want to see a close under $4.80 to attain further downside, or the chart could morph into a $4.80-$5.15 trading range.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...