GOOD MORNING,

Prices took a turn lower as selling surfaced in Minneapolis wheat as rains crossed areas of Canada and the Great Lakes region. Minneapolis Sep. wheat travels 60c off the highs on Monday. Canola futures are lower as well, taking soyoil prices down with it. Profit-taking was noted as prices have rallied hard over the last several weeks to new contract highs. Corn prices could not move over the gap area, leaving it for now as technical resistance. The eastern Corn Belt old crop corn basis is fading. Calls today are lower across the board as trading ranges continue.

WEATHER

--Drier weather in the eastern Corn Belt is welcome as areas have been too wet. Farmers like and need the sunshine for the crops. For today, better organized rains surfaced in Canada which is promoting the profit-taking for Minneapolis wheat, which is extending into other exchanges. The western Corn Belt will continue to see above normal temperatures through next Sunday, creating stress on crops there. Favorable conditions remain in the Delta for beans which are in the reproductive stage.

--Flooding occurs in China's main corn producing states which is threatening crop potential.

REPORTS

Export sales:

beans: 20/21 net 62,000 mt and 21/22 net 176,300 mt (vs. an expected 50-650 kmt)

meal: 20/21 net 68,300 mt and 21/22 net 19,100 mt (vs. an expected 175-500 kmt)

soyoil: 20/21 net 700 mt (vs. an expected minus 20 to plus 20 kmt)

corn: 20/21 net minus 88,500 mt and 21/22 net 47,700 mt (vs. an expected 100-700 kmt)

wheat: 21/22 net 473,200 mt and 22/23 net 5,000 mt (vs. an expected 350-650 kmt)

Sales were not expected to be good, but certainly added morning weight to prices that were already lower.

Wheat: Sales were good, wheat is still in demand as feed. Concerns about crops remain, and chatter remains that China has been inquiring about wheat.

Corn: Sales were poor, reductions of 160K to China, and disappointing new crop sales. South America is cheaper but premiums have been rising.

Beans: Sales low end but expected. South America is less expensive but Argentina's logistical problems are noted. China purchased Argy beans, but asking about US

Meal: Sales low end following better demand as of late.

Soyoil: Poor on rising prices and cheaper offers elsewhere

ANNOUNCEMENTS

BA Exchange reports that Argentine farmers sold large volumes of corn as of July 14 amounting to 1.3 mmt, over 40% higher on the week and on the year, while new crop sales were also sharply higher to 240,100 mt. There were also 816,000 mt of fresh old crop export license applications, bringing the marketing year total up to 31.2 mmt, 15% higher for corn.

BA Exchange reports that farmers sold 85,100 mt of new crop beans as of July 14, 80% and 95% higher on the week and the year, respectively. Old crop forward sales were 20% lower to 660,400 mt, but significantly over volumes year ago. Total old crop sales reached 25.1 mmt, still 8% lower on the year, but marginally higher share of the estimated crop at 57.7%.

21/22 bean production is forecast at 144.7 mmt, with planted areas up 6.7% to 40.85 mln hectare according to Agronegocios vs. 144.0 mmt in 20/21.

CALLS

Calls are as follows:

beans: 25-28 lower

meal: 5.50 - 5.80 lower

soyoil: 140-150 pts lower

corn: 14-16 lower

wheat: 17-19 lower

OUTSIDE MARKETS

The Dow down 42 pts with crude oil trading up to $71.16/barrel, and the US dollar down to 92.63.

TECH TALK

- November bean prices remain sideways from $13.60 - $14.30, and now form new resistance turning lower from a congestion phase from $13.75 -$14.00. The exit to the downside of $13.75 suggests that prices could go back to $13.60, with the 100-day moving average crossing at $13.25. However, the lower end of the trading range is $13.45, and would cover a partial short should we go there. ADX is weak at 17, meaning follow-through at the top and lower end of ranges is not evident.

- December meal back-tracks today into the middle of its range from $355.00 to $385.00, and could continue to be patient. However, lines of support suggest that a pullback to $363.00 is a good place to price, and under that $357.00.

- December soyoil futures are pulling back and heading to trendline support which for the day is located at 5950c to 60c. IF wanting to own the market, this would be a good place to start with a tight sell-stop underneath. While prices are in corrective mode, the major direction is sideways from higher, but not lower. Still like Dec. soyoil from 59c to 66c.

- December corn nearly fills its gap with a trade to $5.73, (gap-fill at $5.73 1/2), and the inability to completely fill with trade over continues to show the inherently weak price movement of this market. Trading lower sets the tone for a continuation of a $5.35 to $5.75 trading range, and for the morning we are going to begin on trendline support at $5.50. If short, would think about covering something in, and keep the rest in case we break $5.50 at the open.

- The December wheat chart now turns sideways from higher, closing an open gap from $7.03 to $7.05, but also closing around the $7.00 benchmark. If short, would think about getting something covered, as the market has been strong and $6.95 - $7.00 is now key support for a market that did get up to $7.25. A close today under $7.00 would suggest that prices could target $6.70-$6.75 for a $6.75 - $7.25 trading range, but would not be surprised to rally back instead of moving downward.

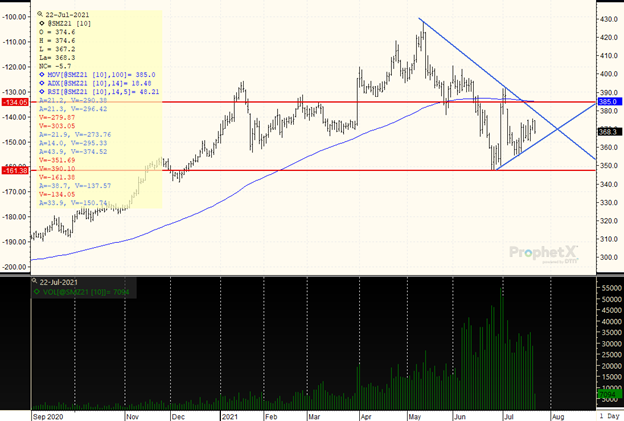

DECEMBER MEAL

Overall trading range is from $355.00 to $385.00. The market is building support levels which is driving prices higher. Trendline resistance and the 100-day moving average crosses at $385.00. The ADX is weak at 18, while the market is balanced. Continue to straddle/strangle, and if needing to price would do so along strong lines of support beginning with multiple lows of $363.00 to lower triangle support at $357.00.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...