THE OPEN

March beans: 19 higher

March meal: 5.90 higher

March soyoil: 120 higher

March corn: 11 higher

March wheat: 4 3/4 higher

The markets opened as called but swiftly traded both sides of unchanged with wheat futures leading the way lower. The business announcements could have been partly built into the rally, as prices traded both sides of unchanged for everything but soyoil futures. Oilshare strength continued as a major feature of trade.

SOY

- The soy complex opened higher but continued its choppy trade with profit-taking from the early morning strength leading to lower meal prices. Traders continue to buy soyoil against meal, sending March oilshare up to 33.91%. March crush trades to 75c/bu, holding steady.

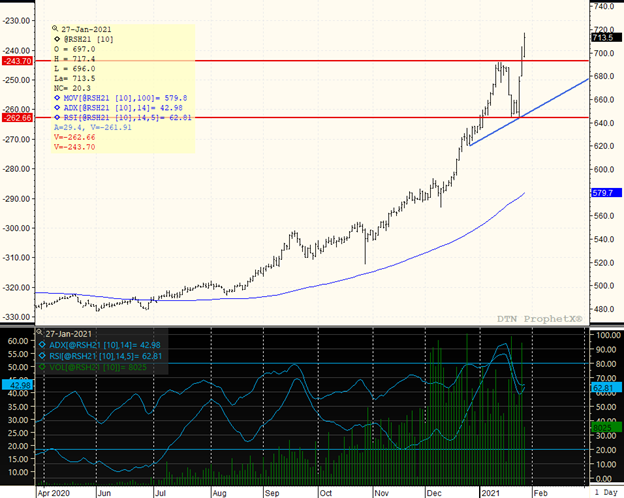

- An extremely strong canola market continued to fuel gains in soyoil. March canola now prints a new contract high at $717.40, providing a strong back-drop for soyoil prices and oilshare.

- Crude oil remains firm, and palm oil trades higher.

- March meal prices bounce around trading towards the lower end of recent prices on lower crush margins and in relation to soyoil futures.

- March beans traded through sell-stops down to major support at $13.65 which for the day held. Spreads were slightly lower with a round of profit-taking as well, with July/Nov trading down to 2.00c from 2.11c. March/May inverse for beans remains a firm 2 3/4c to 3/4c. March/May meal inverse trades down to $2.60 from $3.30.

- The choppy price action suggests that beans and meal are working into wide trading ranges, but soyoil charts remain extremely constructive with pullbacks viewed as buying opportunities.

GRAINS

- The corn and wheat market traded both sides but it was the latter that quickly broke down to trade both sides unchanged.

- Traders appear ready to once again buy beans and corn/sell wheat into the Feb. 9 report.

- March corn prices back away from new contract highs at $5.43 3/4, but good commercial pricing activity supports this market on the lows. Bull-spreads in corn remain solid, with July/Dec inverse trading to a new high of 87c, while May/July inverts to a new contract high of 8 1/2c.

- The EIA report was released today and showed production falling 1.3% to 933,000 bbl/day rate, which would consume 4.9 bln bu of corn. Ethanal stocks were steady dipping 0.1% to 991 mln glns.

- At midday, corn is holding above $5.30, while wheat prices fall back but could successfully test $6.50.

AT 12:00 THE MARKETS ARE AS FOLLOWS:

HI LO

March beans: 4 higher 13.94 3/4 13.64 1/2

March meal: .30 lower 443.20 434.10

March soyoil: 79 higher 4543 4406

March corn: 1 higher 5.43 3/4 5.29 1/2 **new ctr high

March wheat: 9 lower 6.72 3/4 6.52 1/2

March canola: 20.50 higher 717.40 696.00 **new ctr high

OUTSIDE MARKETS

Stocks were down over 300 pts during the first part of the session. Crude oil trades up to $53.30/barrel, with the US dollar trading to 90.15. At the midday hour, stocks are down 300 pts as the stimulus package seems to have been met with some resistance and a slower-than-expected time-frame.

CLOSING COMMENTS

The market is more volatile as prices trend higher, with the large wash-out breaks noted last week. However, technically speaking the funds remain long and the market behavior speaks more to bullish trend verification than a falling bear market. Corn prices place a new contract high, so pullbacks are for pricing or buying. Carry-outs are still tight, harvest is behind in SA, and logistics could get snarled again if the truckers strike persists. If wanting to day trade, look for pullbacks to own and cover shorts quickly until the tide has turned and falling prices find follow-through. Good bounces today off day session profit-taking implies that higher prices are ahead, as weaker markets do not and will not bounce.

Trading range potential:

March corn: $5.20-$5.50

March wheat: $6.50-$7.00

March beans: $13.60-$14..50

March meal: $420.00-$475.00-$480.00

March soyoil: 42c-46c/47c

MARCH CANOLA

The bull market continues with advances to new contract highs at $717.40, with few signs of a trend slow-down. Prices broke out to the upside over peaks at $692.00, and there is no sign of a slow-down for this advance. Canola prices continue to underpin soyoil, and both are seen as marching higher on the back of Chinese demand.

TAGS – Feed Grains, Soy & Oilseeds, Wheat, North America

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Wheat remains the star of the ag commodity space this week with the rally continuing on challenging weather prospects for the U.S. HRW region, Europe, and the Black Sea. Until a few weeks ago, there were few doubts about the 2024 crop being able to supply the expected demand, but now reduced yi...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Most Apparent Solution The EU’s organic sector wants the bloc’s officials to take more action to ensure they achieve the target of 25 percent of agricultural output being organic by 2030. Specifically, they want a campaign to increase consumer demand for organic food so that organic...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...

Yesterday, the Animal and Plant Health Inspection Service (APHIS) issued a federal order requiring testing and reporting of highly pathogenic avian influenza (HPAI) for the interstate movement of lactating dairy cattle. Specific guidance will be issued at some point today, and the order will go...